2019年12月1日(日)

「本日2019年12月1日(日)にEDINETに提出された全ての法定開示書類」

Today (i.e. December 1st, 2019), 0 legal disclosure document has been submitted to EDINET in total.

本日(すなわち、2019年12月1日)、EDINETに提出された法定開示書類は合計0冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計348日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)~2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)~2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)~)

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

R1.11.29

サッポロ合同会社

公開買付条件等の変更の公告

(EDINET上と同じhtmlファイル)

R1.11.29 12:40

サッポロ合同会社

訂正公開買付届出書 対象: ユニゾホールディングス株式会社

(EDINET上と同じPDFファイル)

注:

2019年11月12日(火)のコメントで紹介した訂正公開買付届出書を改めて読んだのですが、重要な部分をスキャンして紹介します↓。

R1.11.11 16:16

サッポロ合同会社

訂正公開買付届出書 対象:

ユニゾホールディングス株式会社

Ⅰ 公開買付届出書

第1 【公開買付要項】

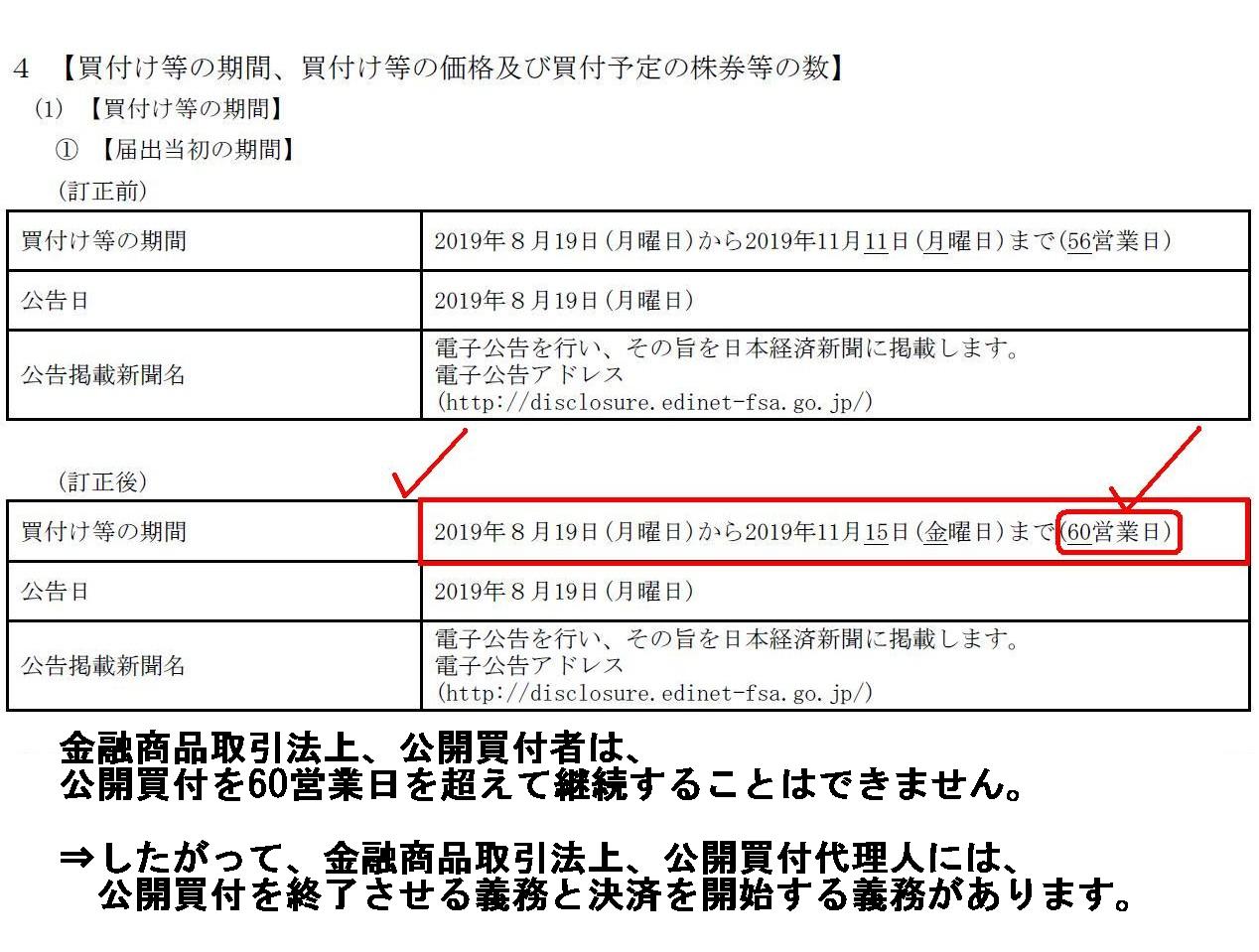

4 【買付け等の期間、買付け等の価格及び買付予定の株券等の数】

(1)【買付け等の期間】

①【届出当初の期間】

(5/6ページ)

公開買付者は、60営業日を超えて公開買付を継続することは金融商品取引法上できません。

したがって、公開買付代理人は、その後さらなる訂正公開買付届出書が提出されようとも、2019年11月15日(金曜日)をもって

公開買付への応募を締め切り(応募の解除の請求にも応じてはなりません)、すみやかに応募株式数の集計を行い、

公開買付が成立していた場合は、訂正後の決済の開始日である2019年11月22日(金曜日)に決済を開始しなければならなかったのです。

公開買付代理人が60営業日を超えて公開買付が継続することを容認すること(公開買付代理人が応募や応募の解除に応じること)は、

率直に言えば、公開買付代理人の法令違反でもあります(公開買付代理人は2019年11月22日(金曜日)に決済を行う義務があります)。

PR TIMES

ttps://prtimes.jp/

2019年11月28日

00時31分

ブラックストーン・グループ・ジャパン株式会社

ブラックストーンによるユニゾホールディングス株式会社(証券コード:3258)との協議の状況に関するお知らせ

Blackstone

Announces Update on Discussions with UNIZO Holdings (Securities Code:

3258)

ttps://prtimes.jp/main/html/rd/p/000000008.000049930.html

「キャプチャー画像」

2019年11月28日

ユニゾホールディングス株式会社

ブラックストーンによる当社買収提案に係る協議継続のお知らせ

ttps://www.unizo-hd.co.jp/news/file/20191128.pdf

(ウェブサイト上と同じPDFファイル)

2019年11月29日

ユニゾホールディングス株式会社

サッポロ合同会社による当社株券に対する公開買付けの買付条件等の変更に関するお知らせ

ttps://www.unizo-hd.co.jp/news/file/20191129.pdf

(ウェブサイト上と同じPDFファイル)

ユニゾホールディングス株式会社に対する公開買付に関する最近のコメント①↓

2019年9月29日(日)

http://citizen2.nobody.jp/html/201909/20190929.html

2019年10月3日(木)

http://citizen2.nobody.jp/html/201910/20191003.html

2019年10月7日(月)

http://citizen2.nobody.jp/html/201910/20191007.html

2019年10月16日(水)

http://citizen2.nobody.jp/html/201910/20191016.html

2019年10月18日(金)

http://citizen2.nobody.jp/html/201910/20191018.html

2019年10月22日(火)

http://citizen2.nobody.jp/html/201910/20191022.html

2019年10月25日(金)

http://citizen2.nobody.jp/html/201910/20191025.html

2019年10月26日(土)

http://citizen2.nobody.jp/html/201910/20191026.html

2019年10月29日(火)

http://citizen2.nobody.jp/html/201910/20191029.html

2019年10月30日(水)

http://citizen2.nobody.jp/html/201910/20191030.html

2019年11月12日(火)

http://citizen2.nobody.jp/html/201911/20191112.html

2019年11月16日(土)

http://citizen2.nobody.jp/html/201911/20191116.html

2019年11月19日(火)

http://citizen2.nobody.jp/html/201911/20191119.html

2019年11月23日(土)

http://citizen2.nobody.jp/html/201911/20191123.html

2019年11月26日(火)

http://citizen2.nobody.jp/html/201911/20191126.html

マネジメント・バイアウト(MBO)や発行者による公開買付に関する過去のコメント↓

2019年9月11日(水)

http://citizen2.nobody.jp/html/201909/20190911.html

真の意味で周知されたウェブサイト上での情報開示は、他のウェブサイト上での情報開示を排除するのです。

すなわち、「PR

TIMES」のウェブサイトが市場の投資家にとって真に周知されたウェブサイトであるのならば、

対象会社は市場の投資家に同じプレスリリースをもう一度お知らせする必要はないのです。

ユニゾホールディングス株式会社によるこの二重の情報開示は、

ユニゾホールディングス株式会社は問題のウェブサイトを周知されてはないと認識している、ということを暗に意味しているのです。

The term "well-known" in this context means, to put it simply, "official on

the securities system."

The most typical example is the "EDINET" and the

"TDnet."

Press release distribution web sites operated by news media or IT

companies specializing in the related distibution

are generally not

recognized as "well-known."

In practice, ultimately speaking, a web site's

being "well-known" requires the fact that the related laws and

ordinances

prescribe that information on the securities system must be

disclosed on the web site.

And, the critical concept with relation to the

concept "well-known" in this context is "exclusive," I suppose.

Even if there

are not any problems at all concerning the Information Security from the

well-known "CIA" down,

in practice, retrieving one disclosure document on

several web sites imposes too many loads on investors in the

market.

Actually, multiplexly-uploaded documents (one document uploaded upto

plural web sites) have already exhausted me myself.

この文脈における「周知された」という用語は、簡単に言えば、「証券制度上公式の」という意味です。

最も典型的な実例は、「EDINET」と「TDnet」です。

報道機関や関連するプレスリリースの配信に特化したIT企業が運営するプレスリリース配信ウェブサイトは、

通常は「周知された」とは認められません。

実務上は、究極的なことを言えば、あるウェブサイトが「周知される」ためには、

関連する法令で証券制度上の情報はそのウェブサイトで開示しなければならないと定めることが必要なのです。

そして、この文脈における「周知された」という概念に関連する重要な概念は、「独占的な」であると私は思います。

たとえあの有名な情報の「CIA」を始めとする情報セキュリティに関しては一切何の問題もないとしても、

実務上は、複数のウェブサイトで同一の開示文書を検索・取得することは市場の投資家に過剰な負担を負わせるのです。

現に、私自身、多重にアップロードされた文書(複数のウェブサイトにアップロードされた同一の文書)にはもう飽きています。

同一の開示文書を複数のウェブサイトにアップロードすることは、市場の投資家に貢献するものではありません。

それどころか、多重アップロードは市場の投資家にとって害になることなのです。

というのは、市場の投資家は、

それら複数のウェブサイトにアップロードされた開示文書1つ1つの全てをわざわざ精読しなければならないからです。

市場の投資家は、それら複数のウェブサイトにアップロードされた開示文書の全てをそれぞれの最後のページまで

読み通して始めて、それら複数の開示文書は皆同じ文書であったということが分かるのです。

Even 2 disclosure documents with the same title do not always have the same contents in them.

開示文書の表題が同じだからと言って内容まで同じとは限らないのです。

Abstractly speaking, a dislosure on the superordinate web site excludes a

disclosure on the subordinate web site.

That is to say, on the principle of

law,

Unizo Holdings Company Limited needn't and mustn't disclose this press

release on its web site

because the "EDINET" is an absolutely well-known web

site for investors in the market.

抽象的に言えば、上位のウェブサイトでの情報開示は下位のウェブサイトでの情報開示を排除するのです。

すなわち、法理的には、ユニゾホールディングス株式会社は、

このプレスリリースを自社ウェブサイト上で開示する必要はありませんしさらに自社ウェブサイト上で開示してはならないのです。

なぜならば、「EDINET」は市場の投資家にとって絶対的に周知されたウェブサイトだからです。

A Tender Offer Agent is at once a person who undertakes the clerical work on

a tender offer

and a person who keeps a tender offer under guard.

公開買付代理人というのは、公開買付に関する事務の引受人であると同時に、公開買付の番人でもあるのです。

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}