2019年10月29日(火)

「本日2019年10月29日(火)にEDINETに提出された全ての法定開示書類」

Today (i.e. October 29th, 2019), 139 legal disclosure documents have been submitted to EDINET in total.

本日(すなわち、2019年10月29日)、EDINETに提出された法定開示書類は合計139冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計315日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜)

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

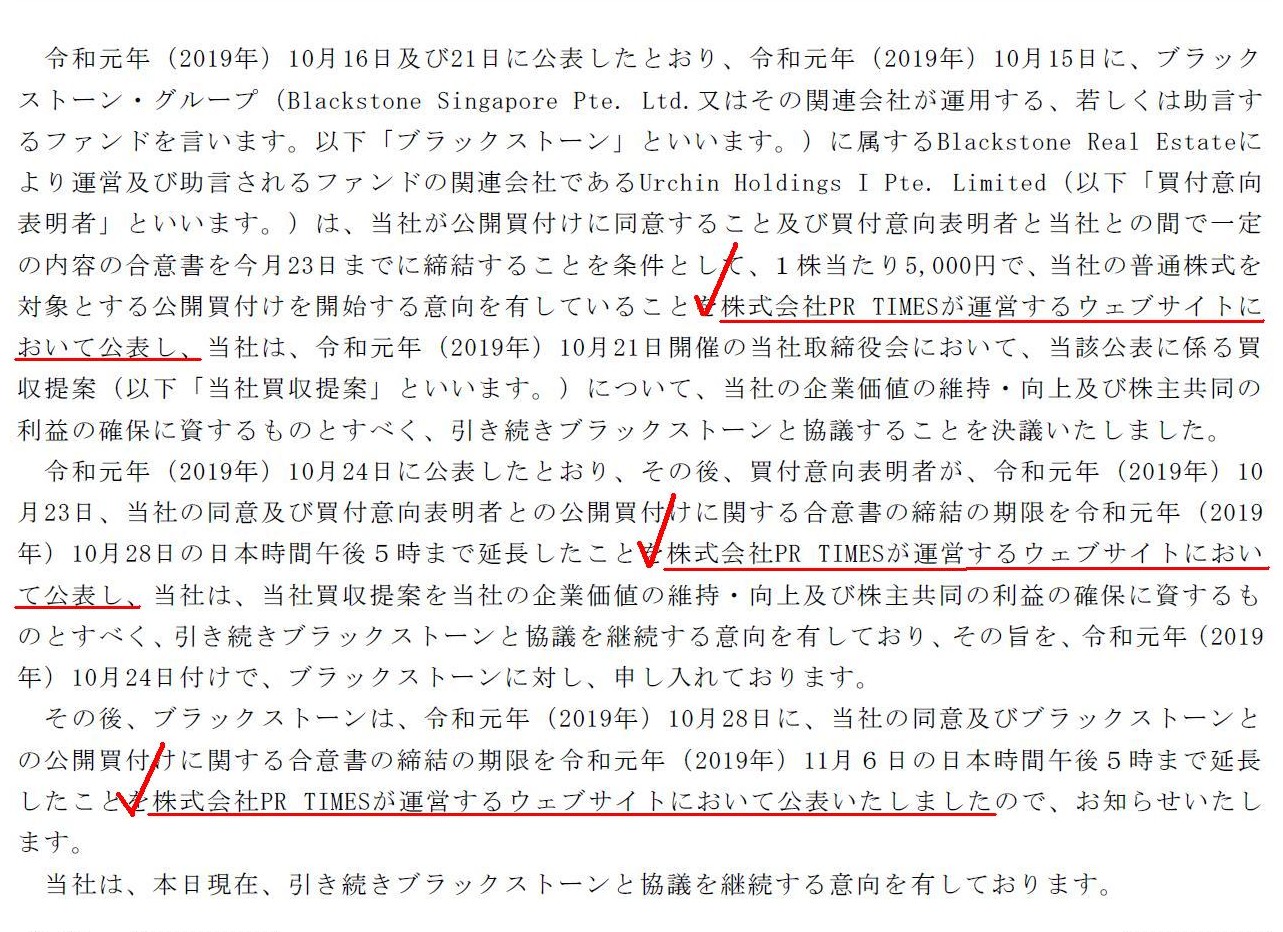

ユニゾHD、米ブラックストーンと「協議継続の意向」

ユニゾホールディングス(3258)は29日、TOB(株式公開買い付け)を巡り米投資ファンドのブラックストーン・グループと

「引き続き協議を継続する意向がある」とのコメントを発表した。

ブラックストーンはユニゾHD側の合意を条件に、TOBによりユニゾHD株の全株取得を目指すとしている。

ブラックストーンは28日、ユニゾHDに提示している買収提案への合意締結期限を11月6日の17時に再度延期していた。

〔日経QUICKニュース(NQN)〕

(日本経済新聞 2019/10/29

11:40)

ttps://www.nikkei.com/article/DGXLASFL29HJ9_Z21C19A0000000/

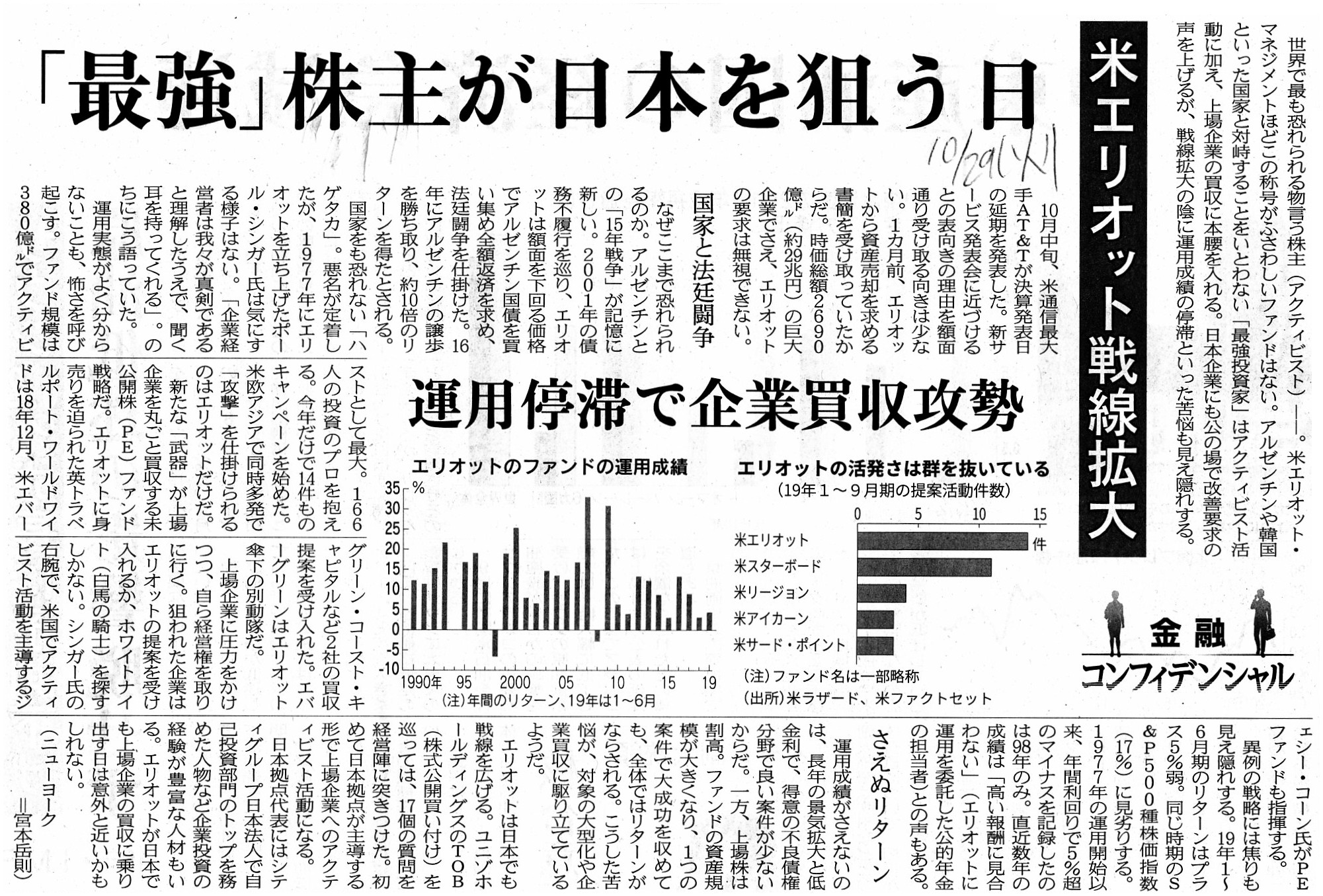

2019年10月29日(火)日本経済新聞

ブラックストーンへの回答延期 ユニゾTOB 混迷増す 不動産価格の上昇 背景に

(記事)

2019年10月29日(火)日本経済新聞

「最強」株主が日本を狙う日 米エリオット戦線拡大 運用停滞で企業買収攻勢

(記事)

(ウェブサイト上と同じPDFファイル)

「本文のキャプチャー画像」

>株式会社PR TIMESが運営するウェブサイトにおいて公表

PR TIMES

ttps://prtimes.jp/

2019年10月29日

ユニゾホールディングス株式会社

令和2年(2020年)3月期第2四半期連結決算の概要

ttps://www.unizo-hd.co.jp/ir/file/gaiyou_20191029.pdf

(ウェブサイト上と同じPDFファイル)

「令和2年(2020年)3月期上期連結業績(平成31(2019)/4〜令和元(2019)/9)」

R1.10.28 11:40

ユニゾホールディングス株式会社

訂正意見表明報告書 対象: サッポロ合同会社

(EDIENT上と同じPDFファイル)

2019年9月29日(日)

http://citizen2.nobody.jp/html/201909/20190929.html

2019年10月3日(木)

http://citizen2.nobody.jp/html/201910/20191003.html

2019年10月7日(月)

http://citizen2.nobody.jp/html/201910/20191007.html

2019年10月16日(水)

http://citizen2.nobody.jp/html/201910/20191016.html

2019年10月18日(金)

http://citizen2.nobody.jp/html/201910/20191018.html

2019年10月22日(火)

http://citizen2.nobody.jp/html/201910/20191022.html

2019年10月25日(金)

http://citizen2.nobody.jp/html/201910/20191025.html

2019年10月26日(土)

http://citizen2.nobody.jp/html/201910/20191026.html

マネジメント・バイアウト(MBO)や発行者による公開買付に関する過去のコメント↓

2019年9月11日(水)

http://citizen2.nobody.jp/html/201909/20190911.html

一つの案は、買収希望者が「正式に」公開買付を提案したい場合は、

関連する提案書を法定開示書類として提出しなければならない、というものです。

この文脈における「正式に」という用語は、

有事の際には刑罰を受けることを条件としてすなわち有事の際には処罰される、という意味です。

One idea is that a listed company should not disclose its "Earnings Report"

(Kessan Tanshin) (Summary)

on the Securities Listing Regulations in a process

of its negotiated M&A.

The reason for it is that grounds of a legal

procedure should be a legal disclosure document.

一つの案は、自社のM&Aについて目下交渉中である時は、上場企業は有価証券上場規程上の「決算短信」を開示するべきではない、

というものです。

その理由は、法手続きの根拠は法定開示書類であるべきだからです。

In theory, coping with a tender offer by an acquirer is

one of the

elements of an execution of operarions of a company as a fiduciary.

In my

personal opinion, a fee which a company pays to a legal advisor and a financial

advisor

concerning its M&A is what you call an "entertainment expense"

(i.e. a non-deductible expense), I suppose.

The reason for it is that a

company in question doesn't gain any earnings with relation to a M&A in

question.

Fees in question have nothing to do with earning its

revenues.

In case a company is an acquirer, the related fees paid to the

related advisors can sometimes be

an acuisition cost (i.e. a deductible

expense),

whereas, in case a company is an acquiree, the related fees paid to

the related advisors will never be

a deductible expense (i.e. the defense

cost will never generate any revenues inside the acquiree company).

Directors

of a company should defend their company against its acquirer through their own

resources.

理論的には、買収者からの公開買付に対処することは、受託者としての会社の業務執行の構成要素の1つなのです。

私個人の考えになりますが、自社のM&Aについて会社が法務アドバイザーと財務アドバイザーに支払ったフィーは

いわゆる「交際費」(すなわち、損金とならない費用)である、と私は思います。

その理由は、当該会社は件のM&Aに関連して何らの収益も獲得はしないからです。

問題のフィーは会社の収益の獲得とは全く関係がないのです。

会社が取得企業である場合は、関連するアドバイザーに支払った関連するフィーは取得原価(すなわち、損金となる費用)

となり得るのですが、会社が被取得企業である場合は、関連するアドバイザーに支払った関連するフィーは

決して損金となる費用とはなりません(すなわち、防衛費用は被取得企業において何らの収益も生み出さないのです)。

会社の取締役は、独力で買収者から会社を防衛するべきなのです。

,139LegalDisclosureDocumentsHaveBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}

{kind=link}