2022年8月14日(日)

「本日2022年8月14日(日)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年8月14日)、EDINETに提出された法定開示書類は合計0冊でした。

「本日2022年8月14日(日)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年8月14日)、TDnetで開示された適時開示は合計0本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1338日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)~2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)~2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)~2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)~2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)~2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)~2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)~2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)~2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)~2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)~2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)~)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

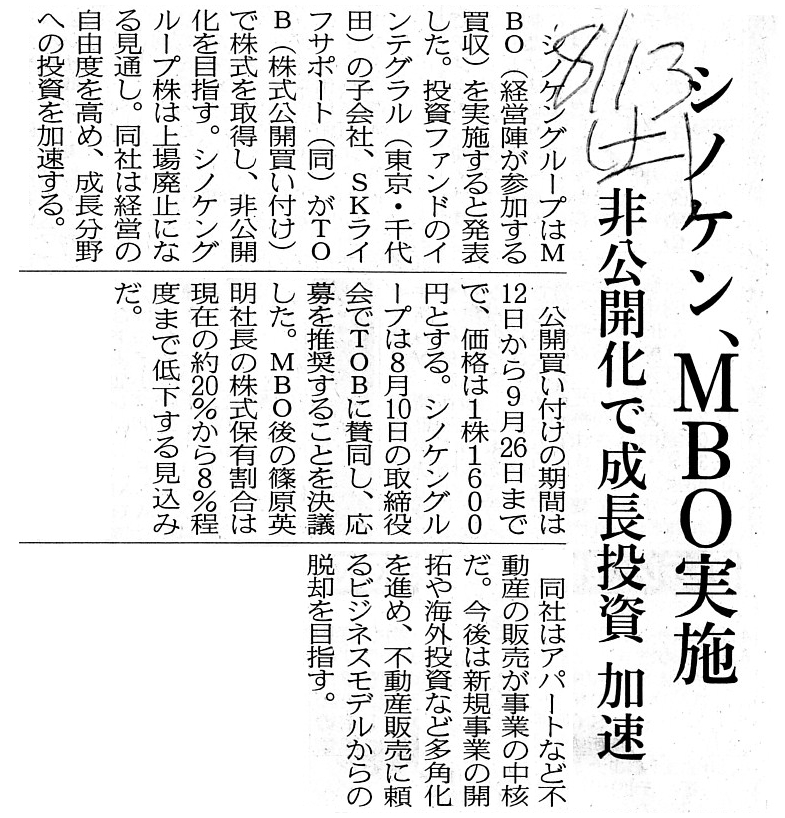

2022年8月13日(土)日本経済新聞

シノケン、MBO実施 非公開化で成長投資 加速

(記事)

シノケングループ<8909>、国内投資ファンドのインテグラルと組んでMBOで株式を非公開化

(M&A

Online 2022/08/10)

ttps://maonline.jp/news/20220810e

「PDF印刷・出力したファイル」

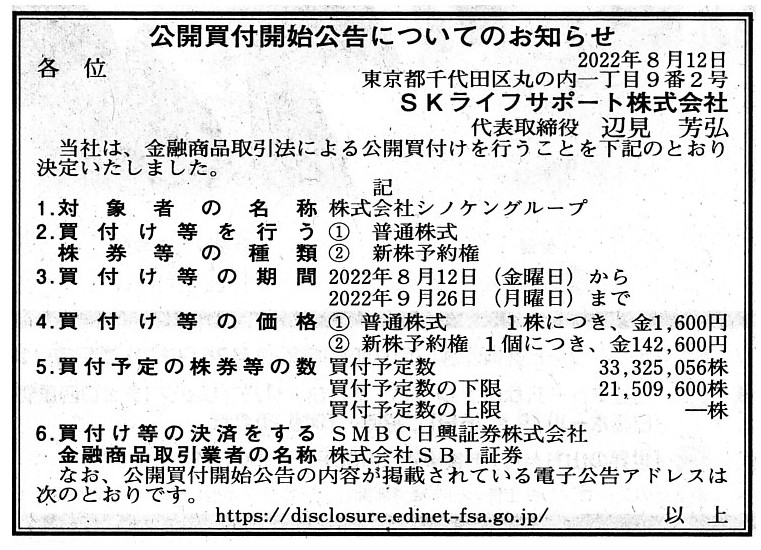

2022年8月12日(金)日本経済新聞 公告

公開買付開始公告についてのお知らせ

SKライフサポート株式会社

(記事)

R4.08.12

SKライフサポート株式会社

公開買付開始公告

(EDINET上と同じhtmlファイル)

R4.08.12 13:24

SKライフサポート株式会社

公開買付届出書 対象: 株式会社シノケングループ

(EDINET上と同じPDFファイル)

R4.08.12 15:57

株式会社シノケングループ

意見表明報告書 対象: SKライフサポート株式会社

(EDINET上と同じPDFファイル)

2022年8月10日

株式会社シノケングループ

MBOの実施及び応募の推奨に関するお知らせ

ttps://www.shinoken.co.jp/Presses/get_img/605/file1_path/20220810_605.pdf

(ウェブサイト上と同じPDFファイル)

2022年8月10日

株式会社シノケングループ

SKライフサポート株式会社による株式会社シノケングループ株券等(証券コード:8909)に対する公開買付けの開始に関するお知らせ

ttps://www.shinoken.co.jp/Presses/get_img/606/file1_path/20220810_606.pdf

(ウェブサイト上と同じPDFファイル)

2022年8月10日

株式会社シノケングループ

2022年12月期の中間配当(剰余金の配当)、期末配当予想の修正(無配)及び株主優待制度の廃止に関するお知らせ

ttps://www.shinoken.co.jp/Presses/get_img/607/file1_path/20220810_607.pdf

(ウェブサイト上と同じPDFファイル)

注:

これは"Management Buy-Out"(マネジメント・バイアウト)ではなく"Management Sell

Out"(経営陣による株式売却)だと思います。

マネジメント・バイアウトが行われるに際して経営陣が公開買付に応募をするということ自体がそもそもあり得ないと言わねばなりません。

提出されている公開買付届出書には、存続会社への出資割合が8%程度となるよう社長が会社側へ再出資することについて

投資ファンドと社長は合意をしていると書かれています(18/57ページ)が、株式を証券取引所へ再度上場することを目指す意向である

とも書かれてあり(18/57ページ)、結局のところ社長は再上場時に所有株式を全て売却する意向なのだろうと私は推測します。

英文会計用語辞典からのスキャン↓。

「"leveraged buyout"(レバレッジド・バイアウト/企業担保借入買収(LBO))」

【コメント】

この事例は、株式会社シノケングループのマネジメント・バイアウトではなく、株式会社シノケングループの経営陣による株式売却だ

と私は考えます(まず①このたびの公開買付で一部売却し、次に②会社の再上場時に「売出し」で残りの株式を売却する予定なのでしょう)。

This is anoter form of a leveraged buyout, or rather, a secondary

distribution by management.

In a series of acquistion procedures which are

scheduled, management of Shinoken Group. Co., Ltd. will

not buy shares of the

company but sell their own shares of the company.

As the 1st phase,

management of Shinoken Group. Co., Ltd. will partly sell their own shares of the

company to

a tender offerer namely substantially to an investment fund

superficially sponsoring a Management Buy-Out of this time,

and, as the 2nd

phase, management of Shinoken Group. Co., Ltd. will sell all of their own

residual shares of the company

to general investors in a stock market through

a secondary distribution when the company gets re-listed in the future.

This

is no form of a Managemet Buy-Out.

This is a combination of a company

acquisition by the investment fund and a potential secondary distribution by

management.

From a standpoint of management of Shinoken Group. Co., Ltd., the

company acquisition by the investment fund is just a cloak.

From a standpoint

of the investment fund, the fact that it has adpoted superficially a form of a

Management Buy-Out

is also a cloak for promoting the general shareholders'

acceptance of its tender offer by means of the company's consent.

And, what

is more, from a standpoint of the investment fund, fundamentally, acquiring a

Shinoken Group. Co., Ltd. Share

is literally a "purchase" as an investment

business.

The investment fund acquires a Shinoken Group. Co., Ltd. Share only

for a purpose of selling the share in the future.

A reason why management of

Shinoken Group. Co., Ltd. will continue to hold a part of their own shares after

the tender offer

is not that the management will continue to hold their own

residual shares of the company after the potential re-listing

but that such a

holding is contributory to pretending that the investment fund's "purchase" is a

Management Buy-Out.

I would like to term this kind of Management Buy-Out a

"Stepping-Stone Sell" (by Management).

これは別の形態のレバレッジド・バイアウト、もとい、経営陣による売出しです。

予定されている一連の買収手続きにおいて、株式会社シノケングループの経営陣は、会社の株式を買うのではなく、

自分達が所有している会社の株式を売却するのです。

第一段階目として、株式会社シノケングループの経営陣は自分達が所有している会社の株式の一部を公開買付者にすなわち

実質的には表面上はこのたびのマネジメント・バイアウトを後援している投資ファンドに売却します。

そして、第二段階目として、株式会社シノケングループの経営陣は会社が将来再上場する際に売出しを通じて

自分達が所有している会社の株式の残りの全てを株式市場の一般投資家に売却するのです。

これはいかなる形態のマネジメント・バイアウトでもありません。

これは投資ファンドによる企業買収と経営陣による将来の売出しの組み合わせです。

株式会社シノケングループの経営陣の立場からすると、投資ファンドによる企業買収はただの隠れ蓑です。

投資ファンドの立場からすると、表面上マネジメント・バイアウトの形を採ったのも会社からの賛同によって

自社が行う公開買付に一般株主が応募することを促進するための隠れ蓑です。

そして、さらに言えば、投資ファンドの立場からすると、そもそもの話、

株式会社シノケングループ株式を取得することは投資業としての文字通りの「仕入れ」なのです。

投資ファンドは、将来売却をすることのみを目的として、株式会社シノケングループ株式を取得するのです。

株式会社シノケングループの経営陣が公開買付後も所有株式の一部を保有し続ける理由は、

経営陣は将来の再上場後も自分達が所有している会社の株式の残りを保有し続けるからではなく、

そのような株式保有が投資ファンドの「仕入れ」はマネジメント・バイアウトであるというふりをするのに役立つからなのです。

私はこの種のマネジメント・バイアウトを(経営陣による)「踏み台売却」("Stepping-Stone

Sell")と名付けたいと思います。

{kind=link}

{kind=link}