2022年8月24日(水)

「本日2022年8月24日(水)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年8月24日)、EDINETに提出された法定開示書類は合計204冊でした。

「本日2022年8月24日(水)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年8月24日)、TDnetで開示された適時開示は合計175本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)〜)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

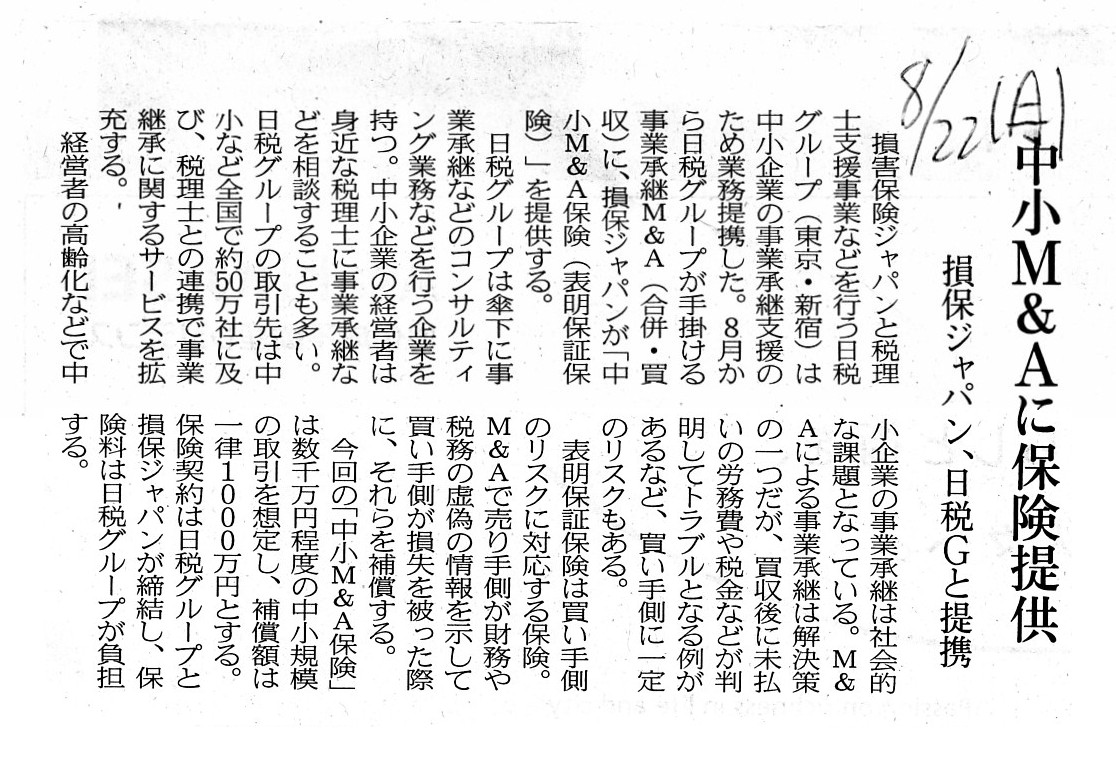

2022年8月22日(月)日本経済新聞

中小M&Aに保険提供 損保ジャパン、日税Gと提携

(記事)

2022年8月22日

日税グループ

損害保険ジャパン株式会社

日税グループと損保ジャパンが中小M&A推進に向けて業務提携中小M&A仲介サービスに表明保証保険を自動付帯

ttps://www.sompo-japan.co.jp/-/media/SJNK/files/news/2022/20220822_1.pdf

(ウェブサイト上と同じPDFファイル)

「"quality"(品質)、"quality assurance"(品質保証)、

"quality at the

source"(供給元における品質)、"quality control"(品質管理(QC))」

【コメント】

In a scene of an M&A, a source itself of information namely a

seller itself of a business ought to become unlimitedly liable.

For example,

in a case that a Certified Public Tax Accountant serves as an agent, or deputy,

for a taxpayer in a filing of

the paxpayer's return to the tax authorities,

the Accountant is able to assure contents stated of the return filed

only

when the taxpayer is unlimitedly liable for contents of a self-declation in

relation to the paxpayer's own income.

Even if a Certified Public Tax

Accountant lives together with a taxpayer like a family, contents of a

declation

to the Accountant in relation to the paxpayer's own income are no

more than a "self-declaraion" at the end of the end.

Even if a patient's own

declaration to a medical doctor is a lie, that misstatement is merely

self-responsible,

but, "self-declations" in the other fields are likely to

damage interests of a person who takes the word.

Ultimately speaking, a

person who assures some state must be exactly a source itself of the

state.

Whoever is at the source should start an assurance and whoever is

other than the source itself can offer a supplement only.

M&Aの場面では、情報の供給元自身がすなわち事業の売り手自身が無限責任を負うべきなのです。

例えば、税理士が納税者の代理人としてすなわち代行者として納税者の確定申告書を税務当局に提出するという場合には、

税理士は納税者自身の所得に関連して自己申告された内容に納税者が無限責任を負う場合のみ、

提出する確定申告書の記載内容を保証することができるのです。

たとえ税理士が納税者と家族のように同居していても、

納税者自身の所得に関連して自分に申告された内容というのは最後の最後は「自己申告」に過ぎないのです。

たとえ患者自身による医者への申告が嘘であってもその虚偽の申し述べは単なる自己責任ですが、

他の分野における「自己申告」はその言葉を信じた人の利益を害しがちです。

究極的なことを言えば、ある事柄を保証する人というのはまさしくその事柄の供給元自身でなければならないのです。

誰であろうとも供給元から保証を始めるべきであり供給元本人以外の人は誰であろうとも補足をすることしかできないのです。

{kind=link}