2022年8月23日(火)

「本日2022年8月23日(火)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年8月23日)、EDINETに提出された法定開示書類は合計109冊でした。

「本日2022年8月23日(火)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年8月23日)、TDnetで開示された適時開示は合計112本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)〜)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

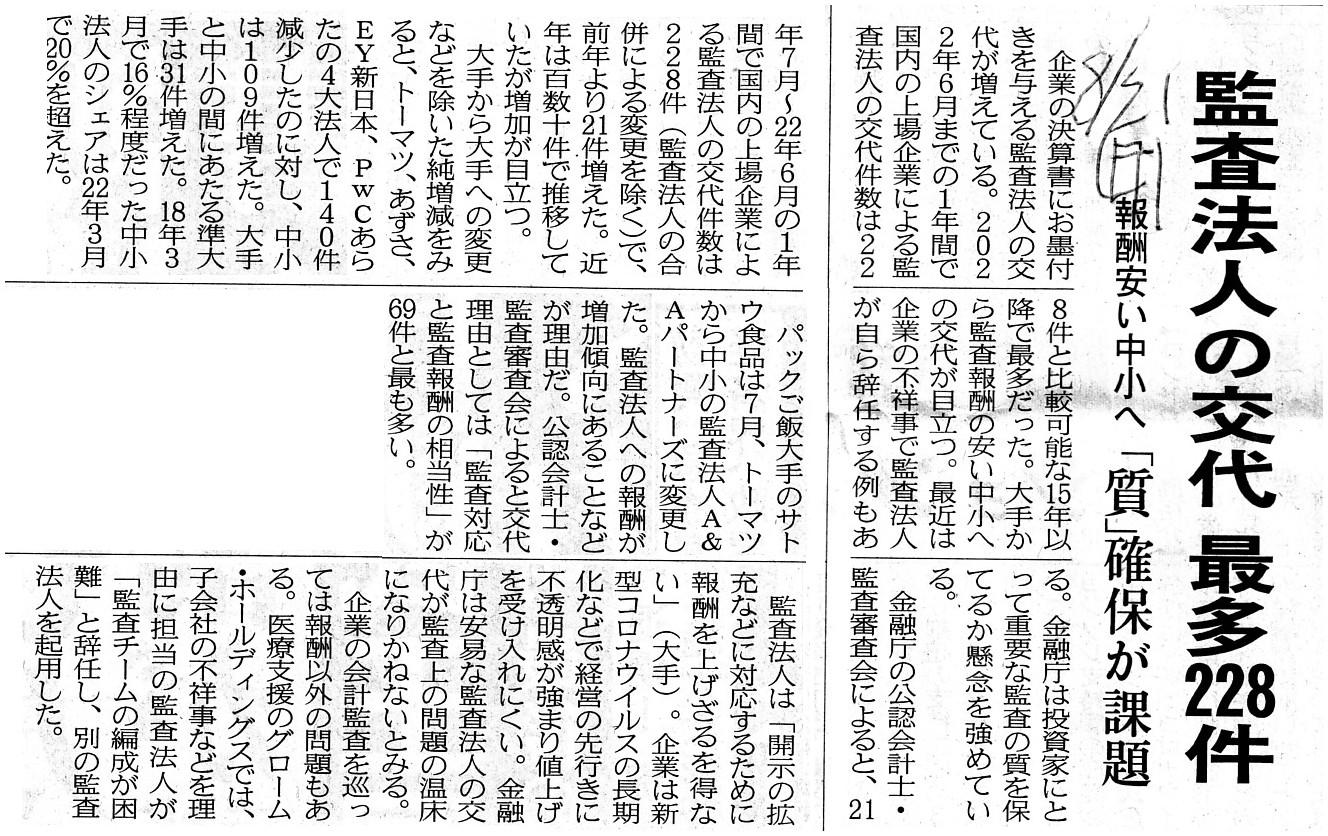

2022年8月21日(日)日本経済新聞

監査法人の交代 最多228件 報酬安い中小へ 「質」確保が課題

(記事)

英文会計用語辞典からのスキャン↓。

「"auditability"(監査可能性)」

「"audit risk"(監査リスク)」(ウェブサイト上と同じPDFファイル)

「PDF印刷・出力したファイル」

A graveness of a hiding risk is much greater than that of an audit

risk.

In consideration of the fact that it is exclusively a director of a

company that executes operations of the company,

the company's having a

Certified Public Accountant audit the company's own financial statements is,

after all, similar to

an "opinion shopping" in another sense than electing a

convenient auditor to the company, I suppose.

It means that an audit report

is just "necessaries" on the securities system, just as a postage stamp put on

an envelope.

隠蔽リスクの深刻さは監査リスクの深刻さよりもはるかに大きいのです。

会社の業務を執行しているのは専ら会社の取締役であるということを鑑みますと、会社が公認会計士に自社の財務諸表を監査してもらう

ことは結局、自社に都合のいい監査人を選任するということとまた別の意味の「オピニオン・ショッピング」に近いのだと私は思います。

つまり、まさに封筒に貼る郵便切手のように、単に証券制度上監査報告書が必要なものだからだ、という意味です。

{kind=link}