2022年8月16日(火)

「本日2022年8月16日(火)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年8月16日)、EDINETに提出された法定開示書類は合計159冊でした。

「本日2022年8月16日(火)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年8月16日)、TDnetで開示された適時開示は合計100本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)〜)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

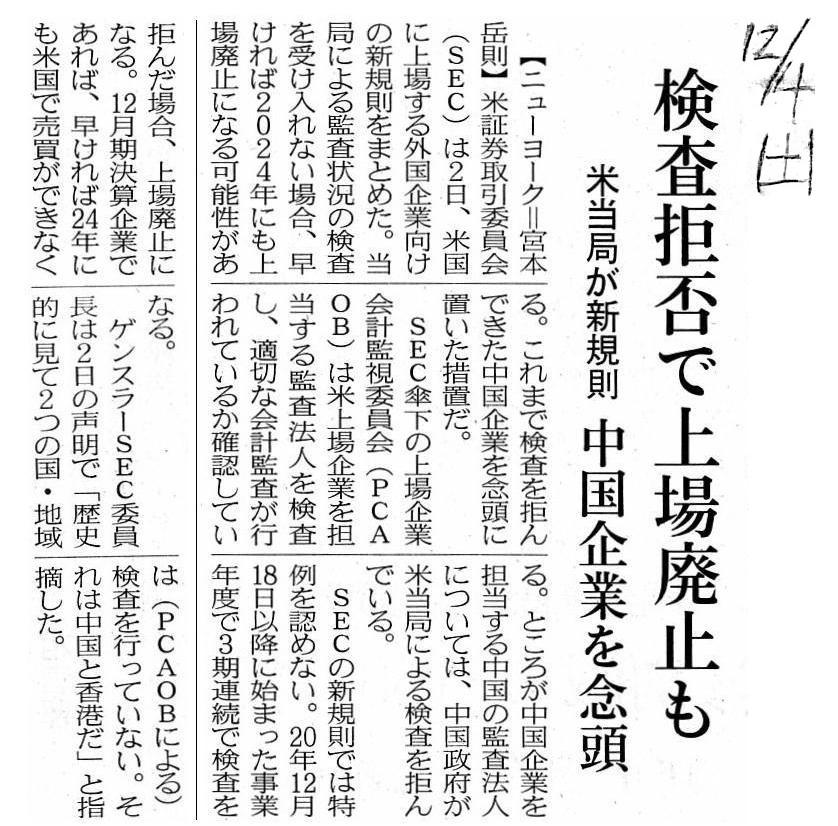

2021年12月4日(土)日本経済新聞

検査拒否で上場廃止も 米当局が新規制 中国企業を念頭

(記事)

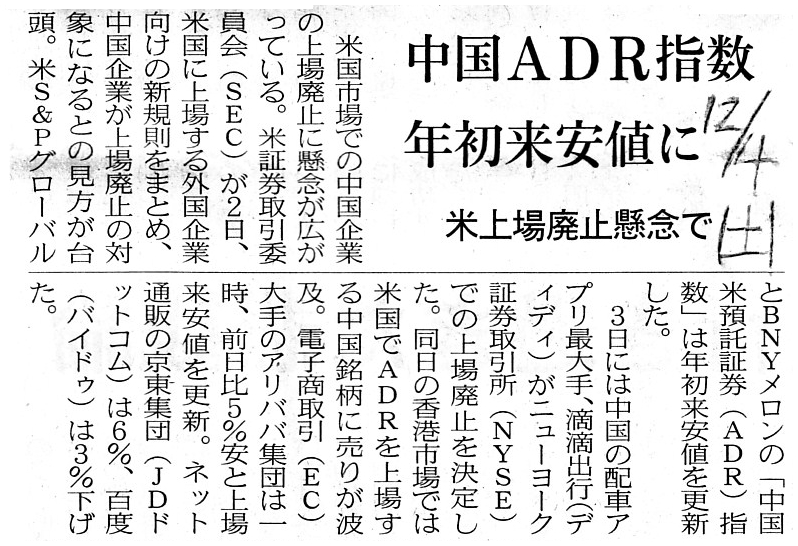

2021年12月4日(土)日本経済新聞

中国ADR指数

年初来安値に 米上場廃止懸念で

(記事)

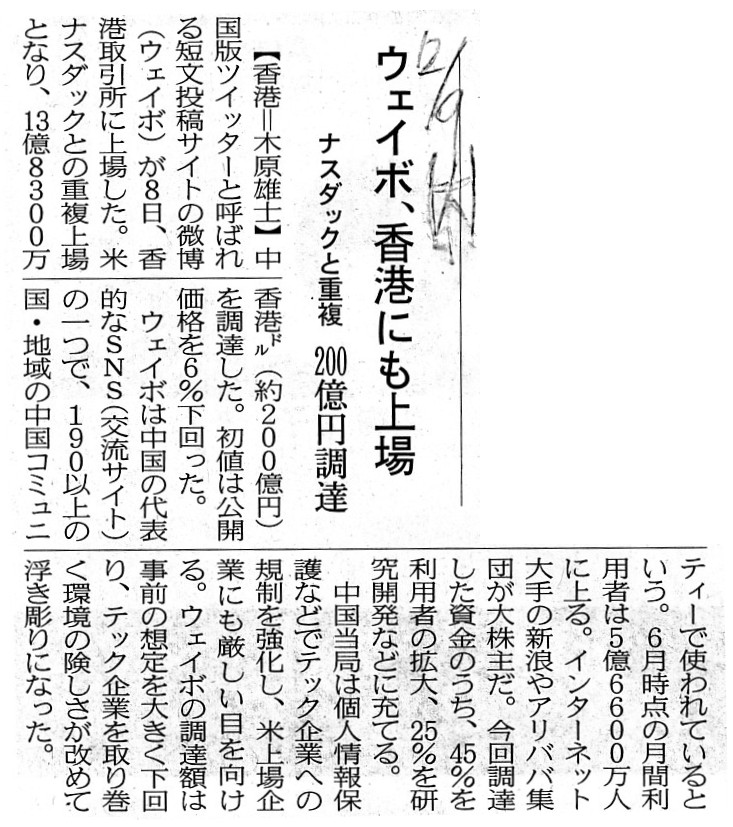

2021年12月9日(木)日本経済新聞

ウェイボ、香港にも上場 ナスダックと重複 200億円調達

(記事)

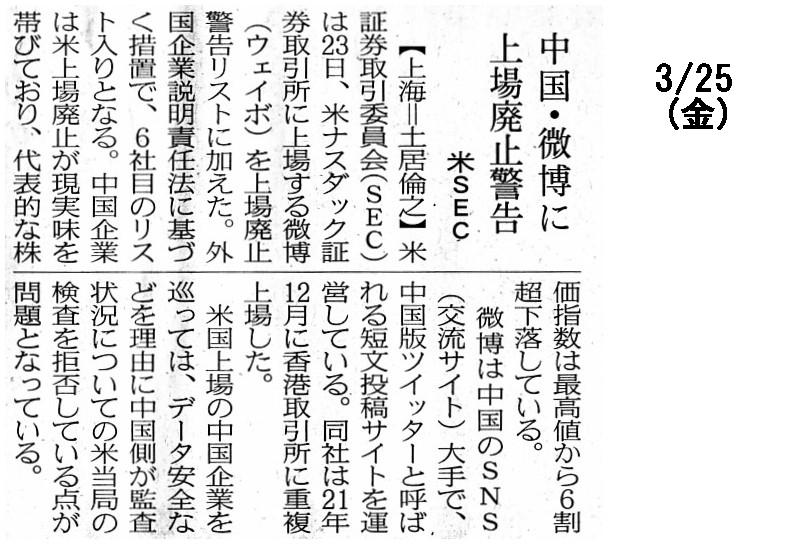

2022年3月25日(金)日本経済新聞

中国・微博に上場廃止警告 米SEC

(記事)

2022年4月1日(金)日本経済新聞

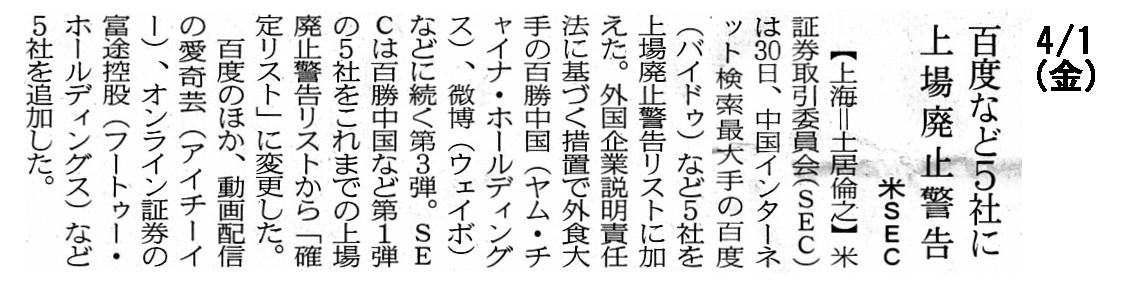

米SEC 百度など5社に上場廃止警告

(記事)

2022年4月3日(日)日本経済新聞

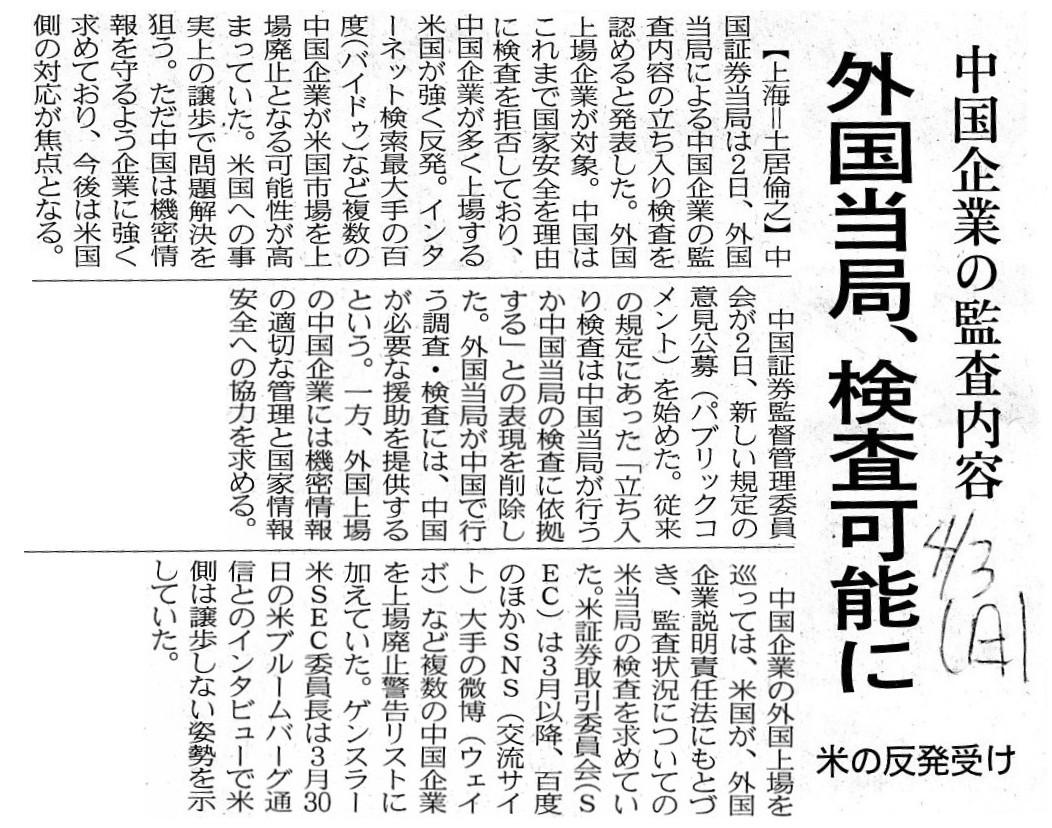

中国企業の監査内容 外国当局、検査可能に 米の反発受け

(記事)

2022年6月9日(木)日本経済新聞

中国テック株

急反発 3月安値から45%高 滴滴など統制懸念後退 米上場廃止リスクは残る

(記事)

2022年6月14日(火)日本経済新聞

中国企業に上場廃止警告 150社対象 米、時期早める構え

(記事)

2022年8月13日(土)日本経済新聞

中国ペトロチャイナなど 国有5社、米上場廃止へ 監査で対立

(記事)

英文会計用語辞典からのスキャン↓。

「"peer review"(ピア・レビュー/公認会計士事務所間の相互審査)」

(ウェブサイト上と同じPDFファイル)

(ウェブサイト上と同じPDFファイル)

米国における米国預託証券制度の最初期には、米国預託証券の発行者の財務諸表に関する会計監査の品質管理はかつて、

「米国公認会計士協会」(AICPA)の品質管理基準の示すところに従って「排他的に」なされていました。

私が知る限り、米国の米国預託証券制度の始めから、世界の全ての国・全ての地域はかつて、要求される「監査そのもの」が

実施可能になるように米国証券取引委員会と共に事を成していました。すなわち、米国の当局に登録されている米国公認会計士自身が

かつてはまさに現地国・現地地域で自分で会計監査を行っていたのです。

あいにくなことに、歴史的に見て、米国預託証券の会計監査制度は最初期の品質保証制度と同じなままではなくなったのです。

すなわち、現地国・現地地域の公認会計士が米国の同等の者達に代わって会計監査をし始めたのですが、

外国の公認会計士は昔も今も将来も少なくとも米国の投資家から見ると会計の専門家ではないのです。

それは米国預託証券の発行者は証券制度上は純粋な「米国企業」であるということなのです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}