2022�N7��28��(��)

�u�{��2022�N7��28��(��)��EDINET�ɒ�o���ꂽ�S�Ă̖@��J�����ށv

�{���i���Ȃ킿�A2022�N7��28���j�AEDINET�ɒ�o���ꂽ�@��J�����ނ͍��v220���ł����B

�u�{��2022�N7��28��(��)��TDnet�ŊJ�����ꂽ�S�Ă̓K���J���v

�{���i���Ȃ킿�A2022�N7��28���j�ATDnet�ŊJ�����ꂽ�K���J���͍��v445�{�ł����B

���j�]�z�[���f�B���O�X������Ђ̔�ٗp�҂��s���u�G���v���C�[�E�o�C�A�E�g�i"Employee Buyout"�j�v�Ɋ֘A����R�����g

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018�N12��18��(��)�̃R�����g�ŁA�\�t�g�o���N������Ђ̏��Ɋւ���L�����v26�{�Љ�A

�u�L���،��̏��ɂ�4�̃p�^�[��������B�v�Ƃ����������쐬���A�ȍ~�A�W���I�ɏ،����x�ɂ��čl�@���s���Ă���̂����A

2018�N12��18��(��)�������܂ł̊e�R�����g�̗v��t���̃����N���܂Ƃ߂��y�[�W�i������݁A���v1321���Ԃ̃R�����g�j�B��

�e�R�����g�̗v��t���̉ߋ��̃����N�i2018�N12��18��(��)�`2019�N4��30��(��)�j

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����2�i2019�N5��1��(��)�`2019�N8��31��(�y)�j

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����3�i2019�N9��1��(��)�`2019�N12��31��(��)�j

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����4�i2020�N1��1��(��)�`2020�N4��30��(��)�j

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����5�i2020�N5��1��(��)�`2020�N8��31��(��)�j

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����6�i2020�N9��1��(��)�`2020�N12��31��(��)�j

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����7�i2021�N1��1��(��)�`2021�N4��30��(��)�j

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����8�i2021�N5��1��(�y)�`2021�N12��31��(��)�j

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����9�i2022�N1��1��(�y)�`2022�N3��31��(��)�j

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����10�i2022�N4��1��(��)�`2022�N6��30��(��)�j

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

�e�R�����g�̗v��t���̉ߋ��̃����N�@����11�i2022�N7��1��(��)�`�j

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

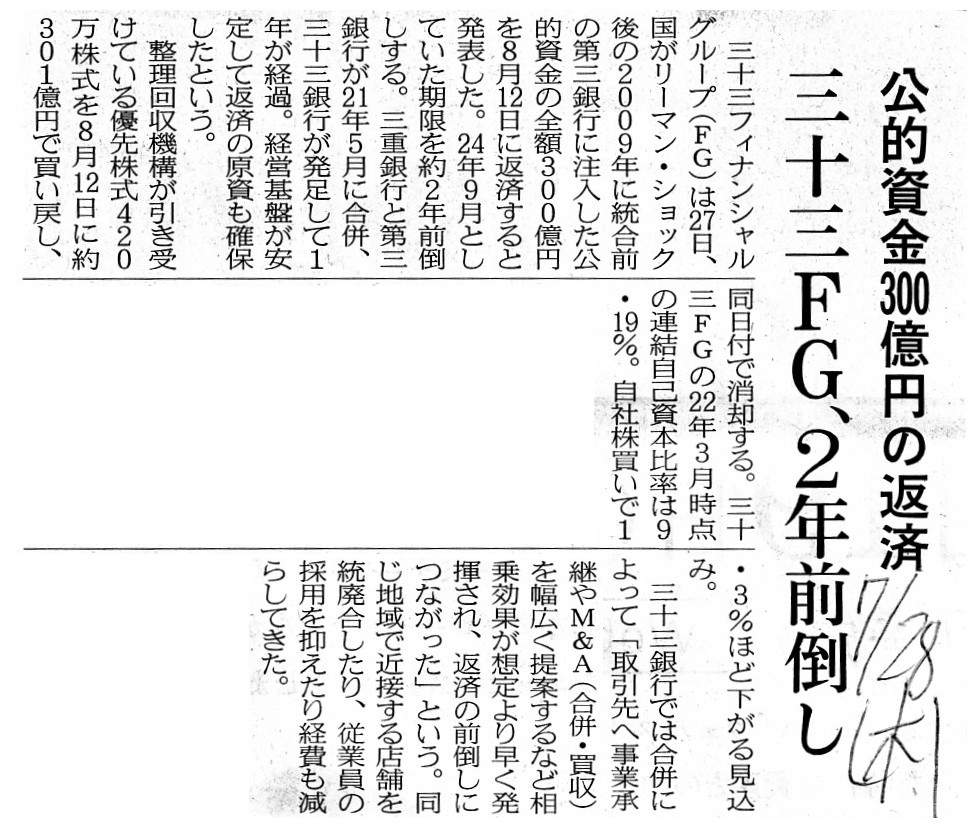

2022�N7��28��(��)���{�o�ϐV��

���I����300���~�̕ԍρ@�O�\�OFG�A2�N�O�|��

�i�L���j

2022�N07��27��

������ЎO�\�O�t�B�i���V�����O���[�v

����D�抔���̎擾����я��p�Ɋւ��邨�m�点

ttps://www.33fg.co.jp/news/pdf/20220727b.pdf

�i�E�F�u�T�C�g��Ɠ���PDF�t�@�C���j

�y�R�����g�z

An "obligee" in a context of a "mortgage" has no limited types in

it.

It is true the most typical type of an "obligee" in a context of a

"mortgage" in practice is a lender of cash, but,

any person who has a promise

to be kept is able to create a "mortgage" with respect to the counterparty's own

immovable property.

So, for example, a shareholder who has a preferred share

which will absolutely be repurchased by a company

within a definite period of

time by any means is able to create a "mortgage" with respect to the company's

own immovable property.

And, the betrothed is also able to create a

"mortgage" with respect to the counterparty's own immovable

property.

However, in a case of a breach of a promise of a marriage, the

betrothed is able to obtain the immovable property

by means of exercising

that "mortgage," but, nonetheless, what the betrothed truly wants remains a

marriage.

Once a couple get married, their relationship becomes immovable,

and a marriage itself is fundamentally a token of a promise.

�u����v�Ƃ��������ɂ�����u���ҁv�Ɍ��肳�ꂽ�T�^�I�l��������킯�ł͂���܂���B

�m���ɁA������u����v�Ƃ��������ɂ�����u���ҁv�̍ł��T�^�I�ȓT�^�I�l���͌����̑ݕt�l�ł���킯�ł����A

�ʂ����Ă��炤�������Ă���l�͒N�ł�����������L���Ă���s���Y�ɂ��āu����v��ݒ肷�邱�Ƃ��ł��܂��B

�ł��̂ŁA�Ⴆ�A�ǂ̂悤�Ȏ�i��p���Ă����̊������ɉ�Ђɐ�ɔ����߂��Ă��炤�\��ƂȂ��Ă���D�抔����

�����Ă��銔��́A��Ђ����L���Ă���s���Y�ɂ��āu����v��ݒ肷�邱�Ƃ��ł���̂ł��B

���ꂩ��A���Ă���l�����肪���L���Ă���s���Y�ɂ��āu����v��ݒ肷�邱�Ƃ��ł��܂��B

�����A����j���̏ꍇ�́A���Ă���l�͂��́u����v���s�g���邱�Ƃŕs���Y����ɓ���邱�Ƃ��ł���̂ł����A

����ł���͂�A���Ă���l���{���ɋ��߂Ă���̂͌����̂܂܂Ȃ̂ł��B

��U�j������������Γ�l�̊W�͕s���̂��̂ɂȂ�܂����A�܂��A���������������̂��̂��̏Ȃ̂ł��B

2022�N7��28��(��)���{�o�ϐV��

�D���Z�A�����u�~���{���v�@�t�@�X�g����L���m�����@�{�Ƃ̐����͂Ŗ���

�i�L���j

2022�N7��26��

�L���m���������

2022�N12�����i��122���j�̏�]���̔z��(���Ԕz��)�y�єN�Ԕz���\�z�̏C���Ɋւ��邨�m�点

ttps://global.canon/ja/ir/release/2022/p2022jul26j.pdf

�i�E�F�u�T�C�g��Ɠ���PDF�t�@�C���j

�i�E�F�u�T�C�g��Ɠ���PDF�t�@�C���j

�i�E�F�u�T�C�g��Ɠ���PDF�t�@�C���j

It is an "expected value on a basis of an actual value" that investors

calculate.

So, investors re-calculate an "intrinsic value of a share" every

time a company discloses the latest actual value.

Note that an "intrinsic

value of a share" is an expected value which is calculated by each

investor.

An "intrinsic value of a share" is the future liquidation

value.

That's why an "intrinsic value of a share" is an expected value.

Therefore, it is still an expected value that investors calculate and it is

still an actual value that a company discloses.

That a company discloses its

proper expected value is totally nonsense.

Even if a company discloses its

proper expected value, that expected value is based on a lot of

information

which investors don't know at all.

Perhaps, from a viewpoint

of the God, a company's proper expected value itself may be closer to

the

future (to-be-disclosed) actual value than each investor's expected value

is.

However, nonetheless, from a standpoint of investors, even if some value

is expected on a basis of

information which they will definitely not come to

know forever namely till a time of a liquidation,

after all,

investors are never able to understand "in what process that conclusion is

reached."

When a company discloses its proper expected value, it has

calculated the expected value on an Established Special Ground,

whereas, that

ground itself is an Empty Shielded Ground, at the least from a standpoint of

investors.

In a context of a disclosure, an Enterprise Screens a Ground

namely, for example, contents stated in an Annual Securities Report.

In

conclusion, a company must definitely not disclose its proper expected

value.

Investors are not the God.

Investors are beings who expect on a

basis of disclosures only.

Otherwise, now that you say in that way, all

disclosures including an Annual Securities Report will comprehensively

be

replaced for a routine and contingent publication of a company's proper various

expected values

including an intrinsic value of a share which the company

itself has properly expected and calculated.

In such a securities system,

needless to say, investors don't peruse an Annual Securities Report

nor

calculate an intrinsic value of a share, nearly like the traditional

securities system before September 30th, 1999.

However, investors trade a

share inside a stock market not nearly at an intrinsic value of the share which

they

have calculated for themselves but nearly at an intrinsic value of the

share which a company itself has properly calculated.

Roughly speaking, a

share price in a stock market fluctuates

every time and only when a company

publishes its proper expected intrinsic value of the share.

If this concept

should be materialized, that would be an birth of the Tertiary securities system

in Japan.

Though it may not be necessary, if the current securities system

should comprehensively transit to this new securities system,

some Certified

Public Accountants would change their profession from an audit to an agency of

tax payment affairs.

�����Ƃ��Z�肷��̂́u���ђl�Ɋ�Â����\�z�l�v�Ȃ̂ł��B

�ł��̂ŁA��Ђ��ŐV�̎��ђl���J�����邽�тɓ����Ƃ́u�����̖{���I���l�v���ĎZ�肷��̂ł��B

�u�����̖{���I���l�v�Ƃ����̂͊e�����Ƃ��Z�肷��\�z�l�ł��邱�Ƃɒ��ӂ��ĉ������B

�u�����̖{���I���l�v�Ƃ����̂͏����̐��Z���l�̂��ƂȂ̂ł��B

���������킯�ł��̂ŁA�u�����̖{���I���l�v�Ƃ����̂͗\�z�l�Ȃ̂ł��B�A

���������āA�����Ƃ��Z�肷��̂͂�͂�\�z�l�ł���A��Ђ��J������̂͂�͂���ђl�Ȃ̂ł��B

��Ђ����ЌŗL�̗\�z�l���J�����邱�Ƃ͑S���Ӗ����Ȃ����ƂȂ̂ł��B

���Ƃ���Ђ����ЌŗL�̗\�z�l���J�����Ă��A���̗\�z�l�͓����ƒB���S���m��Ȃ������̏��Ɋ�Â��Ă���̂ł��B

�Ђ���Ƃ���ƁA�_�l�̎��_���猩��ƁA��ЌŗL�̗\�z�l���ꎩ�̂͊e�����Ƃ̗\�z�l����

�����i�J�������j�̎��ђl�ɋ߂���������܂���B

�������Ȃ���A����ł���͂�A�����Ƃ̗��ꂩ�猩��ƁA�����i�����Ȃ킿���Z�̎��܂Ŏ����B���m��悤�ɂȂ邱�Ƃ�

��ɂȂ����Ɋ�Â��ĉ����̒l��\�z����Ă��A���ǂ̂Ƃ���A

�����Ƃ́u�ǂ̂悤�ȉߒ����o�Ă��̌��_�����̂��H�v�ɂ��Ă͌����ė������邱�Ƃ��ł��Ȃ��̂ł��B

��Ђ����ЌŗL�̗\�z�l���J������Ƃ������A��Ђ͂��̗\�z�l���m�̂�����ʂȗ��ꂩ��̍����Ɋ�Â��ĎZ�肵�Ă���̂ł����A

���̍������ꎩ�̂Ƃ����̂������Ă���Օ����ꂽ�����Ȃ̂ł��B���Ȃ��Ƃ������Ƃ̗��ꂩ��́A�ł��B

���J���Ƃ��������ɂ����ẮA��Ђ͍������A���Ȃ킿�A�Ⴆ�ΗL���،����̋L�ړ��e���A�ӂ邢�ɂ����đI�Ԃ̂ł��B

���_�Ƃ��ẮA��Ђ͎��ЌŗL�̗\�z�l���ɊJ�����Ă͂Ȃ�Ȃ��̂ł��B

�����Ƃ͐_�l�ł͂���܂���B

�����Ƃ͊J�����݂̂Ɋ�Â��ė\�z�����鑶�݂Ȃ̂ł��B

�����łȂ��Ȃ�A�����܂ł��������̂ł���A�L���،������܂ޑS�Ă̏��J������Ў��g���Ǝ��ɗ\�z���Z�肵��

�����̖{���I���l���܂މ�ЌŗL�̗l�X�ȏ��\�z�l�����I�ɂ����ɉ����Č��\���邱�ƂɑS�ʓI�ɒu�������邩�ł��傤�B

���̂悤�ȏ،����x�ł́A�����܂ł�����܂��A�����Ƃ͗L���،������{�����܂��܂������̖{���I���l���Z�肷��

���Ƃ����܂���B1999�N9��30���ȑO�̓`���I�ȏ،����x�ɊT�ˋ߂��킯�ł��B

�������Ȃ���A�����Ƃ́A�����ŎZ�肵�������̖{���I���l�̋ߖT�łł͂Ȃ��A��Ў��g���Ǝ��ɎZ�肵�������̖{���I���l�̋ߖT�ŁA

�����s����ɂ����Ċ������������̂ł��B

��܂��Ɍ����A�����s��̊����́A��Ђ��Ǝ��ɗ\�z���������̖{���I���l�\���邽�тɂ����\���鎞�ɂ̂݁A�ϓ����܂��B

�����ꂱ�̊T�O����������Ȃ�A����͓��{�ő�O�̏،����x�̒a���Ƃ������ƂɂȂ�܂��B

�V�k�S�Ȃ���A�����ꌻ�s�̏،����x���S�ʓI�ɂ��̐V�����،����x�Ɉڍs�����Ȃ�A

�����č�����[�Ŏ����̑�s�ւƓ]������F��v�m���o�Ă��邱�Ƃł��傤�B

{kind=link}

{kind=link}