2022年7月14日(木)

「本日2022年7月14日(木)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年7月14日)、EDINETに提出された法定開示書類は合計436冊でした。

「本日2022年7月14日(木)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年7月14日)、TDnetで開示された適時開示は合計345本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1307日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)〜)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

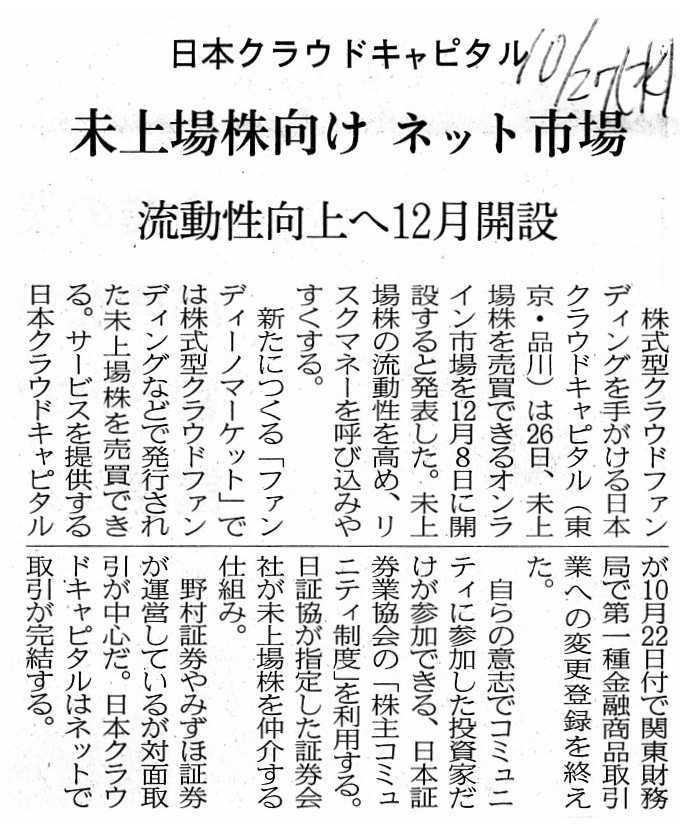

2021年10月27日(水)日本経済新聞

日本クラウドキャピタル 未上場株向け ネット市場 流動性向上へ12月開設

(記事)

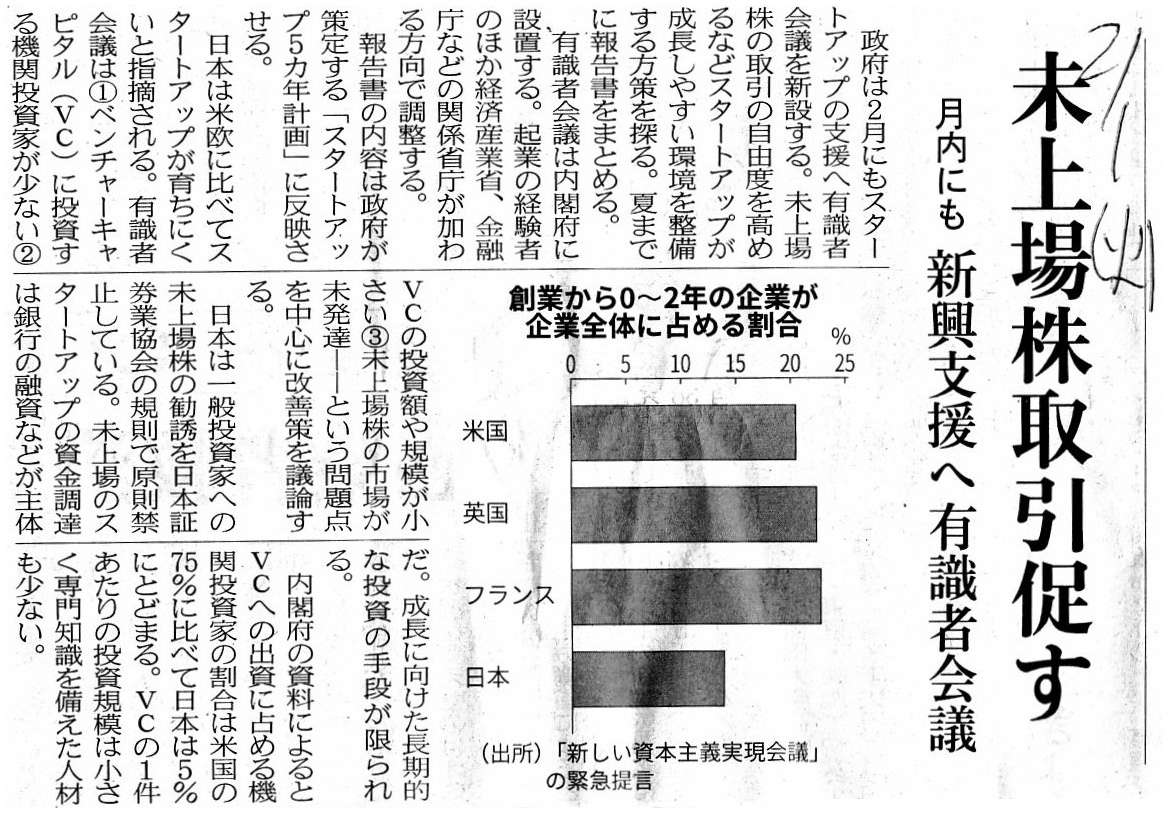

2022年2月1日(火)日本経済新聞

未上場株取引促す 月内にも 新興支援へ有識者会議

(記事)

未上場株、私設取引システムで売買可能に 金融庁方針

金融庁は20日、取引所を介さない私設取引システム(PTS)で未上場企業の株式の売買を可能にする方針を示した。

ただし、対象は機関投資家などのプロ投資家に限定する。経済成長の原動力となるスタートアップの育成に向け、

資金供給の円滑化を図る。PTS制度の見直しについて引き続き議論し、2022年内に詳細をとりまとめる。

同日開いた金融審議会の作業部会で示した。PTSは株式や債券などの有価証券を売買するプラ...

(日本経済新聞 2022年5月20日

20:32

[有料会員限定])

ttps://www.nikkei.com/article/DGXZQOUB203MT0Q2A520C2000000/

株主コミュニティ(日本証券業協会)

ttps://market.jsda.or.jp/shijyo/kabucommunity/

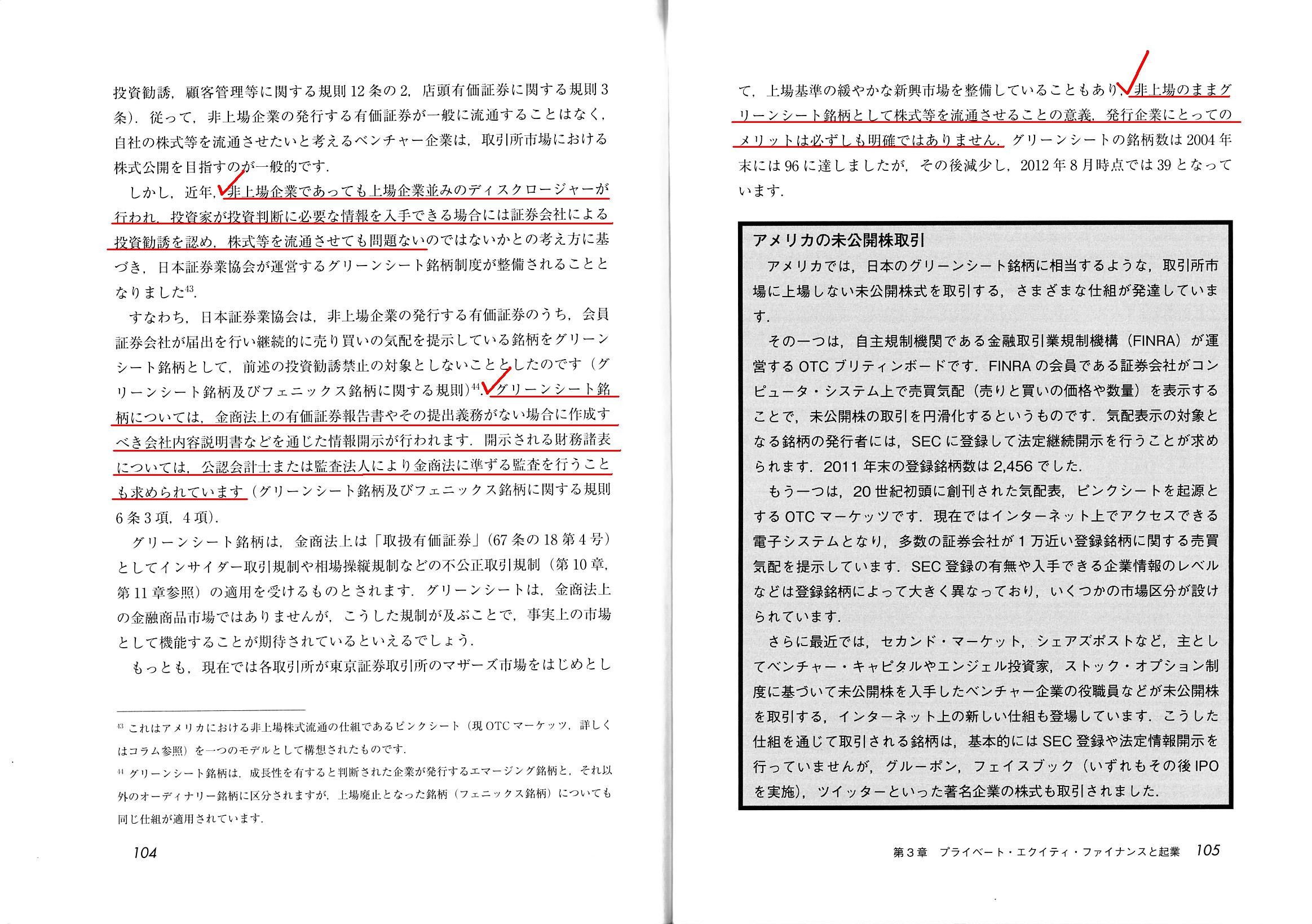

「ゼミナール 金融商品取引法」 大崎貞和 宍戸善一 著 (日本経済新聞出版社)

第3章 プライベート・エクイティ・ファイナンスと起業

3. 私募による資金調達

(2)私募に際しての情報提供

(3)グリーンシート

【コラム】アメリカの未公開株取引

「102〜103ページ」

「104〜105ページ」

【コメント】

Many and unspecified persons don't entrust their money to an

investee company.

That is to say, it is not many and unspecified persons but

a few and specified persons only that entrust their money.

In practice, a few

and specified persons mutually make an investment contract with an investee

company,

but, many and unspecified persons usually don't.

In practice,

disclosed information in a public placement is not always more detailed than

that in a private placement.

In comparison with disclosed information in a

private placement, disclosed items stated in disclosed information

in a

public placement have moderately been cut down in order for companies which have

made a public placement

to become able to actually make an information

disclosure continuously (namely every business year) afterward in

practice.

It may be too much to say that this is a legal information

disclosure system version of that "convoy method," though.

By the way, in a

proprietary trading system, it is true that a trading of a share is not made

through a stock exchange,

but, after all, a share traded there is the one

listed in exactly a stock exchange.

A proprietary trading system has another

order board (market) itself in it but doesn't have any proper tradable brands in

it.

An expression "trading in a market of an unlisted share" is

self-contradictory, I suppose.

Quite contrary to a stock exchang, a

proprietary trading system has never originally borne an information disclosure

function,

which is the very center of an investor protection, and, it must

get equipped with the function if it wants to become

a true stock market, in

which an orderers guard by means of disclosures is the top priority.

In

future, a proprietary trading system must follow the example of a stock

exchange, or it will stay a hollowed-out market.

And, the current

"Shareholders Community" system is a deteriorated version of the former "Green

Sheet" system.

Unlike common listed companies, no Annual Securities Report is

submitted and no legal accounting audit is made there.

One idea is that, in

consideration of a lack of sufficient disclosures, the maximum number of

investors who are able to

participate in a single Shareholders Community at

one time is less than 50.

不特定多数の人が自分のお金を出資先企業に信託するということはありません。

すなわち、自分のお金を信託するのは不特定多数の人ではなく特定かつ少数の人だけなのです。

実務上、特定かつ少数の人は出資先企業と出資契約を取り交わしますが、不特定多数の人は通常出資契約を取り交わしたりはしません。

実務上は、公募の際の開示情報は私募の際の開示情報よりも詳細であるとは限りません。

私募の際の開示情報と比較すると、公募の際の開示情報に記載される開示項目は、実務上公募を行った会社が

その後現実に継続して(すなわち、毎事業年度)情報開示を行うことができるように、適度に削減されているのです。

これはあの「護送船団方式」の法定情報開示制度版だと言うのは言い過ぎかもしれませんが。

ところで、私設電子取引システムでは、確かに株式の取引は取引所を介さずに行われるわけですが、

結局のところ、そこで取引される株式は他ならぬ取引所に上場されている株式なのです。

私設電子取引システムには板(市場)自体は別の板(市場)があるのですが取引可能な固有の銘柄は一切ないのです。

「未上場株式の市場での取引」という表現は自己矛盾であると私は思います。

取引所とは正反対に、私設電子取引システムは、情報開示機能―投資家保護のまさに中心にあるもの―を独自に担うということを

これまで一度もしていませんので、真の株式市場―そこでは情報開示を用いた注文者保護が最優先事項となるのですが―

になりたいのであれば、情報開示機能を備えるようにならなければなりません。

今後は、私設電子取引システムは取引所を見習わねばなりません。さもないと、中心が抜け落ちた市場のままになってしまうでしょう。

それから、現在の「株主コミュニティ」制度はかつての「グリーンシート」制度の劣化版です。

一般的な上場会社とは異なり、「株主コミュニティ」では有価証券報告書は提出されませんし法定の会計監査も行われません。

十分な情報開示がなされないことを鑑みれば、一つの案は、一つの株主コミュニティに一度に参加することができる投資家の人数は

最大で50人未満である、というものです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}