2022年7月13日(水)

「本日2022年7月13日(水)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年7月13日)、EDINETに提出された法定開示書類は合計203冊でした。

「本日2022年7月13日(水)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年7月13日)、TDnetで開示された適時開示は合計242本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1306日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)〜)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

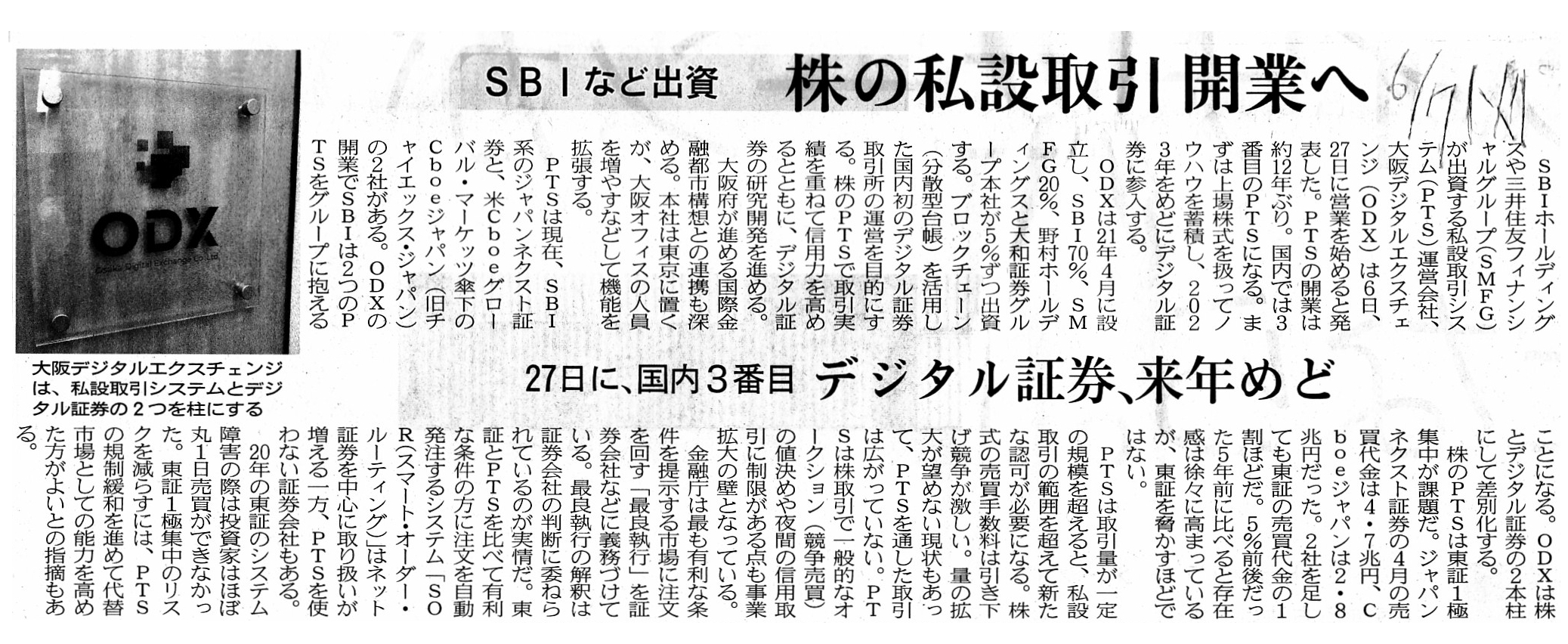

2022年6月7日(火)日本経済新聞

株の私設取引 開業へ SBIなど出資 27日に、国内3番目 デジタル証券、来年めど

(記事)

2022年7月5日(火)日本経済新聞

株の私設取引、規制緩和へ 東証一極集中を改善 年内にも結論 売買高や認可など 金融庁

12年ぶり参入

契機 ODX、先月末に取引開始

(記事)

大阪デジタルエクスチェンジ株式会社 - ODX

ttps://www.odx.co.jp/

>当社は株式PTS(私設取引システム)を運営しており、

>日本で登録された証券会社を参加者として株式取引等の付け合せを行っております。

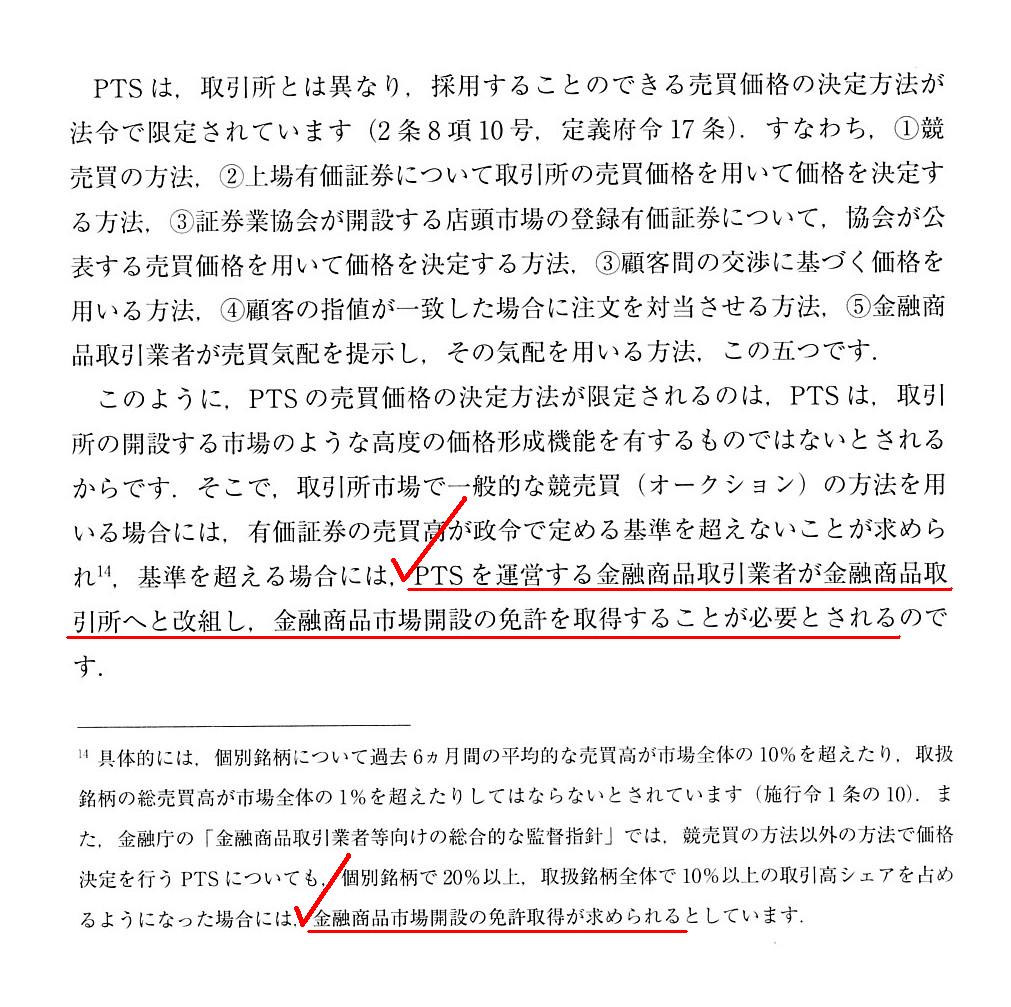

金融商品取引業者等向けの総合的な監督指針

令和4年6月(金融庁)

ttps://www.fsa.go.jp/common/law/guide/kinyushohin/

「キャプチャー画像」

「ゼミナール 金融商品取引法」 大崎貞和 宍戸善一 著 (日本経済新聞出版社)

第13章 証券市場のインフラストラクチャー

1. 金融商品取引所

(3)金融商品取引所市場における取引と取引所外取引

私設電子取引システム(PTS)

「342ページ」

Members Exchange

ttps://memx.com/

有識者に聞く「米国に証券取引所が多い」理由|LINE法務室長・山本雅道氏

(M&A

Online 2019/08/20)

ttps://maonline.jp/articles/ltse_memx20190820

「PDF印刷・出力したファイル(1ページ目)」

「PDF印刷・出力したファイル(2ページ目)」 「PDF印刷・出力したファイル(3ページ目)」

注:

欧州では私設電子取引システムのことを"multilateral trading

facility"(MTF)と表現するようです。

日本語では「多角的取引システム」と訳されるようです(同時に多数の市場参加者を相手とする取引システムという意味合いでしょう)。

この文脈で"multi-"という言葉を用いるのならば、私案になりますが"multi-landing"という言葉で表現するのはどうでしょうか。

「同一の上場株式を取引する場("land")が複数ある。」という意味と「飛び交う(出されている)売買注文を取引所市場に加え

ここでも着地(成約)させる("land")ことができる。」という意味の両方を"multi-landing"に込めてみました。

"multi-places"(複数の取引場所)と"multi-matching"(成約が複数だ)の両方の意味合いを"land"で表現できないだろうかと思いました。

The Osaka Digital Exchange of this time is fundamentally different from, for

example, the Members Exchange in U.S.

Generally speaking, what you call a

"stock exchange market" has its own proper listed share in it,

whereas a

proprietary trading system doesn't.

You are able to commence a proprietary

trading system comparatively easiy and within a short period,

whereas

commencing a "stock exchange market" takes really a long long time.

A reason

for it is that commencing a "stock exchange market" must begin with collecting

listed shares from scratch.

このたびの大阪デジタルエクスチェンジは例えば米国のメンバーズエクスチェンジとは本質的に異なります。

一般的なことを言えば、いわゆる「取引所市場」には固有の上場株式がありますが、

私設電子取引システムには固有の上場株式はないのです。

私設電子取引システムは比較的容易にそして短期間の内に開始することができますが、

「取引所市場」を開始することは本当に長い長い時間がかかります。

その理由は、「取引所市場」を開始するためにはゼロから上場株式を募ることから始めなければならないからです。

【コメント】

いくら私設電子取引システムを開設しても、東京証券取引所への一極集中の状態が変動するわけではありません。

その理由は、東京証券取引所は「取引所市場」であるのに対し、私設電子取引システムは東京証券取引所で取引されている上場株式を

追加的に取引するために別途設けられた取引場所であるというに過ぎないからです(そこでは東証上場銘柄を取引するだけなのです)。

取引システムの運営者こそ異なるものの、「上場銘柄」という観点から見れば、私設電子取引システムは東京証券取引所の

「マーケット・イン・マーケット」("market

in

market")に過ぎないのです(異なる株式市場や上場銘柄があるわけでは決してない)。

率直に言えば、このたびの大阪デジタルエクスチェンジは「証券取引所」では全くないのです(取引シェアとは全く無関係なのです)。

In a proprietary trading system, a share listed in a stock exchange is

traded.

In other words, a proprietary trading system functions as an

alternative trading market.

In other words, a proprietary trading system

presupposes a stock exchange and a share listed in a stock exchange.

This is

of my own coining, but, a proprietary trading system may be colloquially termed

a "sub-market."

On the other hand, what you call a "stock exchange market" is

a "native stock market."

A "stock exchange market" is essential to a trading

of a share, whereas a proprietary trading system offers one only partially.

A

proprietary trading system has merely taken advantage of the existing "stock

exchange market" since its birth

and is never able to stand on its own feet,

and, a share traded in a proprietary trading system is, as it were, a

"sub-listed share."

It's truly an "SL." (It's a joke though.)

Exactly, a

proprietary trading system has profited at someone else's expense.

Quite

contrary to a proprietary trading system, a "stock exchange market" has

completed

(namely has completely been equipped with) all the functions

necesssary for a trading of a listed share inside it by itself.

On the

traditional securities system before September 30th, 1999, securities companies

used to be at once an intermediary of

a market and an operator of a market,

but, they have never been interdependent on a proprietary trading

system,

and, an "over-the-counter market" has substantially been equal to the

originator in terms of a complete equipment of functions.

Today, please learn

only this and go home.

A "stock exchange market" is a "native market,"

whereas a proprietary trading system is an "alternative market."

私設電子取引システムでは、証券取引所に上場している株式が取引されるのです。

他の言い方をすれば、私設電子取引システムは代替的な取引市場として機能しているのです。

他の言い方をすれば、私設電子取引システムは証券取引所と証券取引所に上場している株式を前提としているのです。

これは私の造語ですが、私設電子取引システムは口語表現を使えば「下位市場」と呼んでよいのです。

これに対し、いわゆる「取引所市場」は「生来の株式市場」なのです。

「取引所市場」は株式の取引に必要不可欠ですが、私設電子取引システムは株式の取引を部分的にしか提供していません。

私設電子取引システムはただ単にその誕生の時から既存の「取引所市場」を利用しているだけであり、独り立ちすることは決してできず、

また、私設電子取引システムで取引される株式は言わば「サブリスティッド株式」(「又上場株式」)なのです。

これがほんとの「SL」です(冗談ですが)。

まさしく、私設電子取引ステムは人のふんどしで相撲を取っているのです。

私設電子取引システムとは正反対に、「取引所市場」は上場株式の取引のために必要な全ての機能を

独力で自取引所内に完結させている(すなわち、完備している)のです。

1999年9月30日以前の伝統的な証券制度では証券会社は市場仲介者であるのと同時に市場運営者であったわけですが、

証券会社が私設電子取引システムと相互依存になったことは今までに一度もなく、

また、「店頭市場」は諸機能の完備性という点において本家と実質的に同等であるのです。

今日はこれだけ覚えて帰って下さい。

「取引所市場」は"native

market"(「生来市場」)であり、私設電子取引システムは"alternative

market"(「代替市場」)なのです。

{kind=link}

{kind=link}

{kind=link}