2022年7月8日(金)

「本日2022年7月8日(金)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年7月8日)、EDINETに提出された法定開示書類は合計342冊でした。

「本日2022年7月8日(金)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年7月8日)、TDnetで開示された適時開示は合計237本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1301日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜2022年6月30日(木))

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

各コメントの要約付きの過去のリンク その11(2022年7月1日(金)〜)

http://citizen2.nobody.jp/html/202207/PastLinksWithASummaryOfEachComment11.html

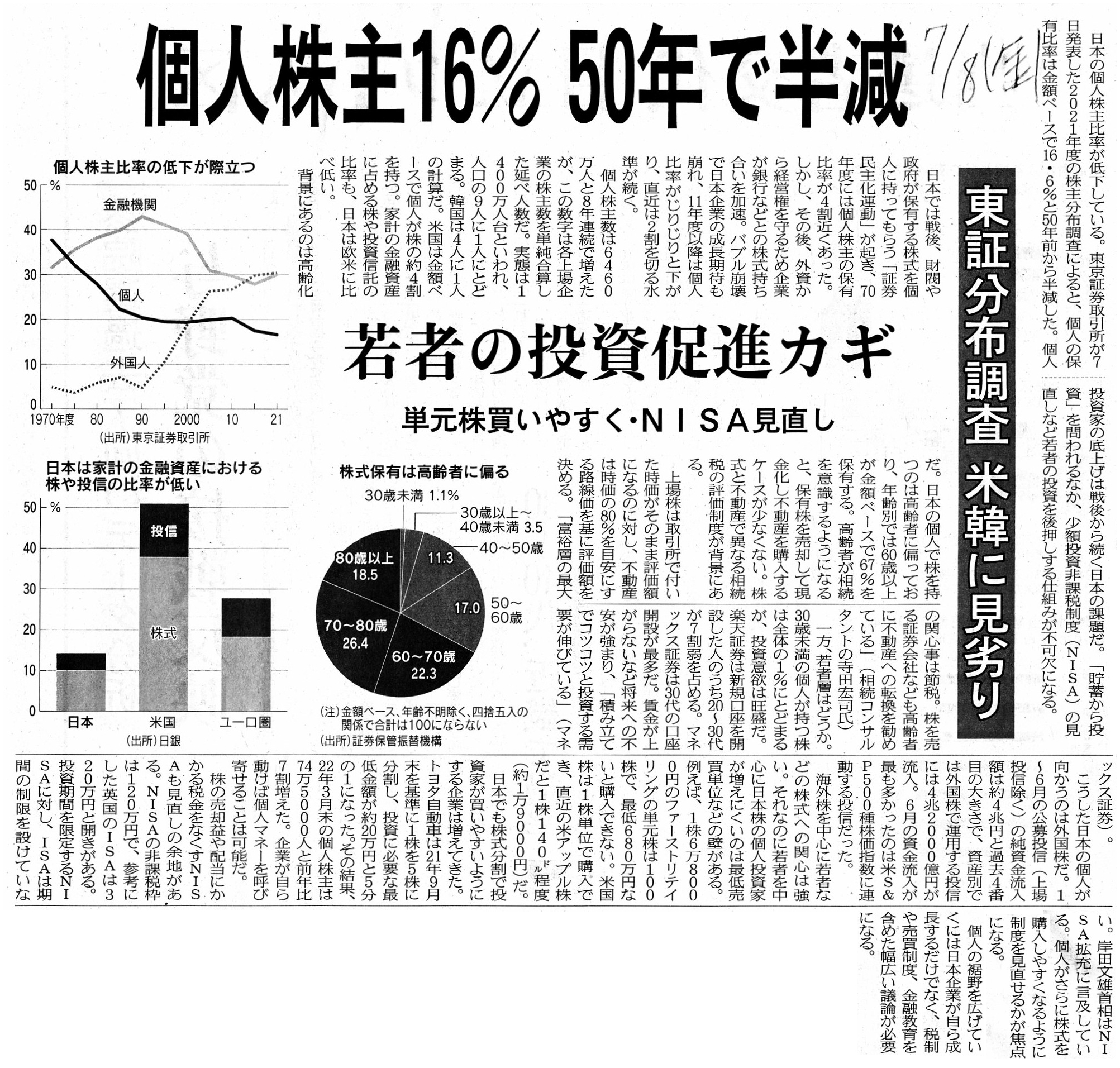

2022年7月8日(金)日本経済新聞

個人株主16% 50年で半減 東証分布調査

米韓に見劣り 若者の投資促進カギ 単元株買いやすく・NISA見直し

(記事)

2022年7月7日

株式会社東京証券取引所

2021年度株式分布状況調査の調査結果について<要約版>

ttps://www.jpx.co.jp/markets/statistics-equities/examination/nlsgeu000006i70f-att/j-bunpu2021.pdf

(ウェブサイト上と同じPDFファイル)

【コメント】

For individual investors, an amount itself of an investment unit is

not a moment.

In other words, for them, a minimum amount itself invested in

one listed brand is neither a motivation nor a discourgement.

Just as no

individual investors care about a market capitalization of one listed brand in

considering a securities investment,

no individual investors care about a

mark capitalized into the listed brand at the least.

A proverb "Least said,

soonest mended." goes in the real life world, but,

in the securities

investment world, a maxim "Least invested, soonest mended." doesn't go.

I

would like to say, "Least read, deepest remembered." or "Least read, so long

minded."

concerning timely disclosures and legal disclosure documents such as

an Annual Securities Report, etc.

Roughly speaking, individual investors buy

their respective favorites without minding the minimum investment amount, that's

all.

So, as a result of a share split, a cumulative total of individual

investors increases but a net total of them doesn't vary.

For a favorite

doesn't increase in a stock market for individual investors, though a liquidity

itself of that brand increases.

However, as a result of a new listing, a

cumulative total of individual investors increases

and a net total of them

also increases.

For a favorite itself increases in a stock market for

individual investors.

個人投資家にとって、投資単位の金額それ自体は変化を生みだす本質的要素ではありません。

他の言い方をすれば、個人投資家にとって、一つの上場銘柄に投じる最低金額それ自体は動機でもありませんし抑制でもありません。

証券投資を検討する際に上場銘柄の時価総額を気にする個人投資家は一人もいないように、

その上場銘柄に投資をする最低限度の金額水準を気にする個人投資家は一人もいないのです。

「言葉少なければ災い少なし。」という諺が実生活の世界にはありますが、

証券投資の世界には「投資額少なければ災い少なし。」という処世訓があるわけではありません。

私は適時開示と有価証券報告書等のような法定開示書類に関して、「閲覧少なければ心に深く忘れずに覚えているものだ。」

もしくは「閲覧少なければ非常に長い間気にしてしまうものだ。」と言いたいと思います。

乱暴に言えば、個人投資家はそれぞれ自分が好きな銘柄を最低投資金額は気にすることなく買う、ただそれだけなのです。

それで、株式分割が行われますと、個人投資家の延べ人数は増加しますが個人投資家の実人数は変動しません。

というのは、その銘柄の流動性自体は増加しているものの、個人投資家にとって自分が好きな銘柄は株式市場で増加していないからです。

しかしながら、新規上場が行われますと、個人投資家の延べ人数は増加しますし個人投資家の実人数も増加します。

というのは、個人投資家にとって自分が好きな銘柄そのものが株式市場で増加するからです。

{kind=link}