2022年5月5日(木)

「本日2022年5月5日(木)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年5月5日)、EDINETに提出された法定開示書類は合計0冊でした。

「本日2022年5月5日(木)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年5月5日)、TDnetで開示された適時開示は合計0本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1237日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜)

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

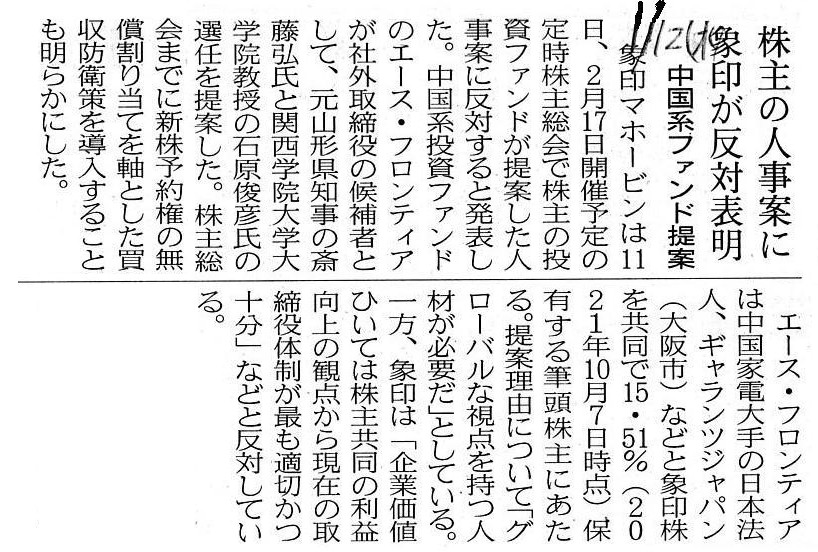

2022年1月12日(水)日本経済新聞

株主の人事案に象印が反対表明 中国系ファンド提案

(記事)

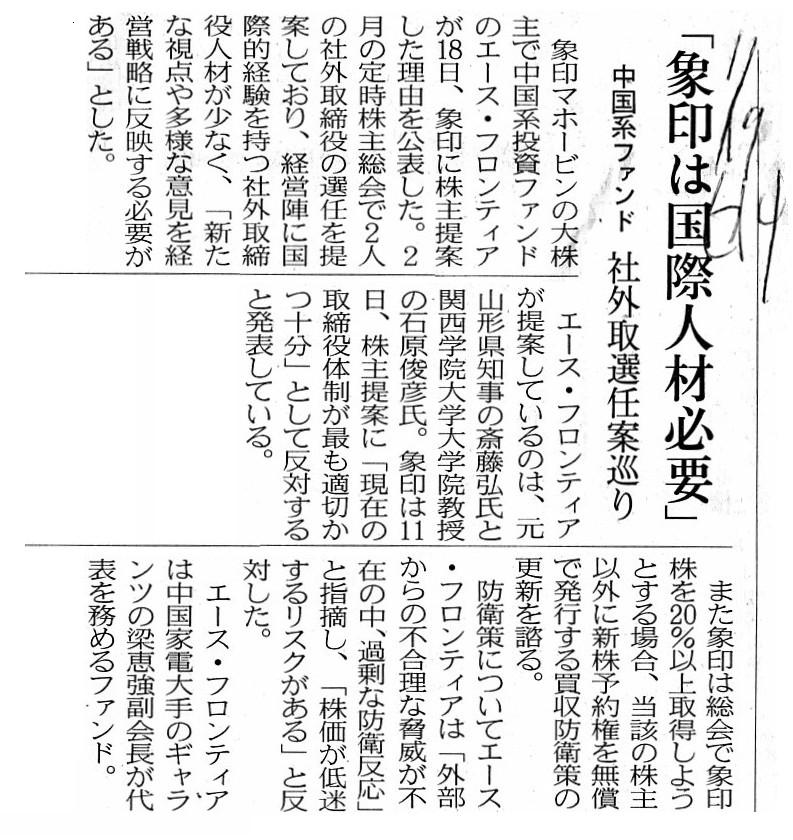

2022年1月19日(水)日本経済新聞

「象印は国際人材必要」 中国系ファンド 社外取選任案巡り

(記事)

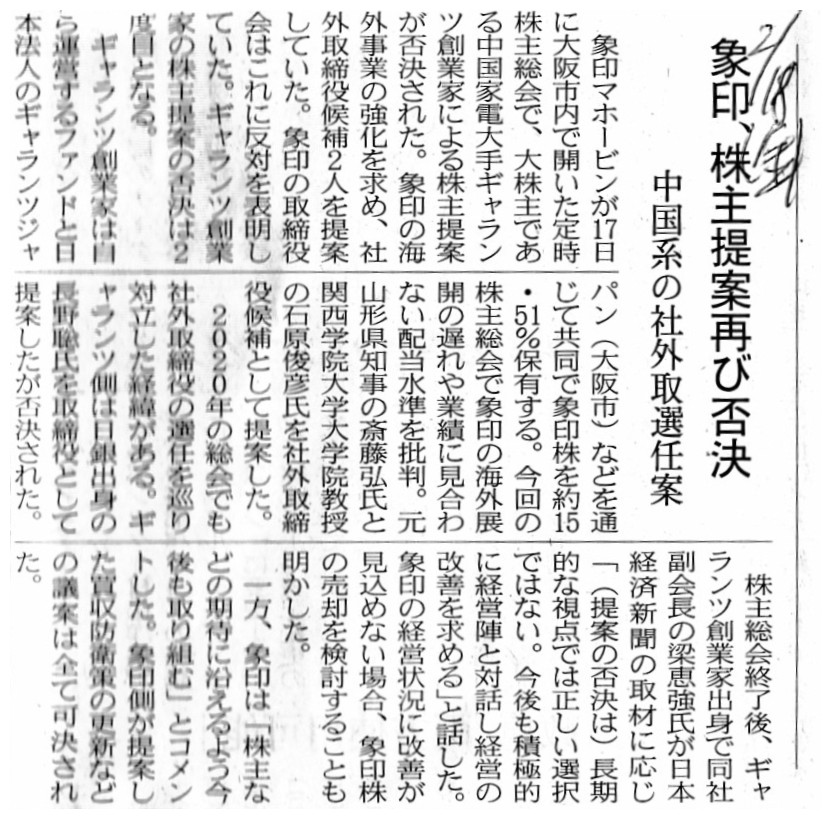

2022年2月18日(金)日本経済新聞

象印、株主提案再び否決 中国系の社外取選任案

(記事)

2021年12月3日

象印マホービン株式会社

新市場区分における「プライム市場」選択申請に関するお知らせ

ttps://www.zojirushi.co.jp/corp/ir/library/pdf/disclose/20211203.pdf

(ウェブサイト上と同じPDFファイル)

2022年1月11日

象印マホービン株式会社

当社株式の大量取得行為に関する対応策(買収防衛策)の導入について

ttps://www.zojirushi.co.jp/corp/ir/library/pdf/disclose/20220111_2.pdf

(ウェブサイト上と同じPDFファイル)

2022年1月11日

象印マホービン株式会社

株主提案に対する当社取締役会意見に関するお知らせ

ttps://www.zojirushi.co.jp/corp/ir/library/pdf/disclose/20220111_3.pdf

(ウェブサイト上と同じPDFファイル)

2022年3月24日

象印マホービン株式会社

主要株主の異動に関するお知らせ

ttps://www.zojirushi.co.jp/corp/ir/library/pdf/disclose/20220324.pdf

(ウェブサイト上と同じPDFファイル)

象印ってどんな会社 /

象印の事業領域(象印マホービン株式会社)

ttps://www.zojirushi.co.jp/corp/ir/individual/area.html

「PDF印刷・出力したファイル」

注:1

東京証券取引所で株式市場の再編が実施された2022年4月4日(と直近の決算が発表された2022年4月1日)付けの記事を紹介します↓。

旧市場と新市場とで株価の連続性は本当にあるると言えるだろうかとふと思いました。

象印の12〜2月、純利益27億円 高価格帯炊飯器が好調

(日本経済新聞 2022年4月1日 23:00

[有料会員限定])

ttps://www.nikkei.com/article/DGXZQOUF019AK0R00C22A4000000/

「キャプチャー画像」

「キャプチャー画像」

注:2

象印マホービン株式会社が新サービスの実証実験を行っているという記事を紹介します↓。

象印マホービン株式会社は飲食店に注文管理などのシステムを提供することで手数料を得る、というビジネスモデルとのことです。

マイボトル、飲食店に預けて利用 象印が新サービス

(日本経済新聞 2022年3月28日 2:00

[有料会員限定])

ttps://www.nikkei.com/article/DGXZQOUF079SY0X00C22A3000000/

「キャプチャー画像」

注:3

ギャランツジャパン株式会社のウェブサイトを紹介します↓。

家電を製造販売している会社というより投資会社という印象を受けました。

ギャランツジャパン株式会社

ttps://www.galanz.co.jp/

「キャプチャー画像」

【コメント】

紹介している記事とプレスリリース等を題材にして、一言だけコメントを書きたいと思います。

2022年2月17日に開催された象印マホービン株式会社の定時株主総会では中国の家電メーカーであるギャランツ社が

取締役の選任を求める株主提案を提出していたのですが株主提案は否決された、とのことです。

上の方にギャランツジャパン株式会社のウェブサイトを紹介していますが、家電を製造販売しているというより、

まさに投資業を本業としているようだと私は思いました。

最近の電気製品の取扱説明書は内蔵している機能の割りに薄いような気がしますが、

ギャランツ社が作成したプレゼンテーション資料は力がこもっており株主に強く訴えかける内容だと思いました。

最近の会社は顧客のことではなく投資家のことを第一に考えているのだろうかと思いました。

顧客のことを第一に考えてこそ、会社は投資家と向き合うことができるはずだと思いました。

それにしましても、ギャランツ社側が提案していた取締役候補者は象印マホービン株式会社の事業ともギャランツ社の事業とも

関係がない人物であるように私は思いました(グローバルな視点が本当に候補者にあったのでしょうか)。

それから、提案する候補者を前回から変更しますと、最善の候補者を挙げていないかのような印象を一般株主に与えてしまうと思います。

A purpose of a vacuum bottle is maintaining a temperature of a drink inside

it, but, traditinoally,

a purpose of a stock market is maintaining a kinetic

energy namely a liquidity of a share inside it.

On the traditional securities

system before September 30th, 1999,

a purpose of tradings of a listed share

used to lie exactly in energizing those tradings themselves.

Such a situation

meant not that tradings of a listed share had become thier own goal

but that,

when all is said and done, thermos, sorry, circulating a listed share among

investors

had been exactly an essence at the least on the securities system

in those days.

In other words, in those days, a trading of a listed share

used to have nothing to do with management of a company,

nor with gaining an

investment profit.

魔法瓶の目的は内部の飲み物の温度を保持することですが、

伝統的には株式市場の目的は市場内の株式の運動エネルギーをすなわち流動性を保持することなのです。

1999年9月30日以前の伝統的な証券制度では、上場株式の取引の目的はまさにそれら取引そのものを活性化させることにあったのです。

そのような状況というのは、上場株式の取引は自己目的化していたというわけではなく、

要するに、サーモス、失礼しました、上場株式を投資家達の間で循環させるということが少なくとも当時の証券制度における

まさに根本的要素だった、ということなのです。

他の言い方をすれば、当時は、上場株式の取引は会社の経営とは全く関係がなかった、ということです。

そして、投資利益を得ることとも。

Originally, a word "thermos" used to be a registered trademark, but, it has

now become virtually a common noun.

By the way, does a titleholder of an

intellectual property have to pay a registration fee at the Japan Patent

Office?

And, is a listing fee necessary?

For example, the Shanghai Stock

Exchange is a non-profit organization

directly administered by the China

Securities Regulatory Commission (CSRC).

元々は「サーモス」という言葉は登録商標だったのですが、今では事実上普通名詞化しています。

ところで、知的財産権の権利者は特許庁で登録手数料を支払う必要があるのでしょうか。

そして、上場料金というのは必要なのでしょうか。

例えば、上海証券取引所は中国証券規制委員会が直接運営をしている非営利組織です。

Vacuum bottles of the Zojirushi Corporation may be able to keep a temperature

of a drink inside them,

but, stock exchanges are not always able to keep a

listing fee with which listed companies are burdened.

That is to say, when

stock exchanges update their services such as a commencement of a new stock

price index,

they can't help raising a listing fee because of additional

clerical work and an equipment renewal investment, etc.

For example, a

re-arrangement of stock markets made in this April has cost the Tokyo Stock

Exchange a lot.

The Tokyo Stock Exchange surely attempts to shift the

re-arrangement-related costs to a listing fee.

Pupils use vacuum bottles of

the Zojirushi Corporation on a school excursion day and a school sports meeting

day,

but, there doesn't exist such a thing as a free lunch.

This is true

of everything, but, when another service is provided, another price is burdened

with.

If the Tokyo Stock Exchange raises a listing fee, then an intrinsic

value itself of a share of each listed company decreases,

and consequently, a

share price in a stock market of each listed company drops inevitably.

That

decrease in an intrinsic value of a share causes a discontinuity of a share

price in a stock market.

Concretely speaking, a share price in a stock market

on April 1st, 2022 and that on April 4th, 2022 are not continuous,

if a

listing fee is raised according to a re-arrangement of this time

though.

Purely in theory in corporate finance, listed companies are not

burdened with any costs of a listing at all.

Generally speaking, what you

call a "contract" (i.e. what you call an "obligation") costs,

whereas what

you call an "official duty" does not cost.

I would never like to assert that

stock markets today which are privately-operated are "sham battles of

investments" nor

"white elephants," but, if citizens want only business

profits in a narrow sense to be reflected into a share price

in a stock

market to the utmost, stock markets in the world ought to be

publicly-established and publicly-operated,

either in a capitalist state or

in a democratic state or in a non-electoral state.

象印マホービン株式会社の魔法瓶は内部の飲み物の温度を維持できるかもしれませんが、

証券取引所は上場会社が負担する上場料金を維持できるとは限らないのです。

すなわち、証券取引所が新しい株価指標の開始のようなサービスをアップデートするという時、

追加的な事務作業や設備更新投資等のために上場料金を上げざるを得ないわけです。

例えば、この4月に行われた株式市場の見直しは東京証券取引所にとって多額の費用がかかっているわけです。

東京証券取引所は再編関連費用を上場料金に転嫁しようとすることでしょう。

児童達は遠足の日や運動会の日に象印マホービン株式会社の魔法瓶を使っていますが、フリーランチのようなものはないのです。

何事でもそうですが、別のサービスが提供されるならば別の代金を負担するものです。

東京証券取引所が上場料金を値上げするならば、各上場会社の株式の本源的価値そのものが減少することになりますし、

その結果、各上場会社の株式市場における株価は必然的に下落します。

株式の本源的価値の減少は株式市場における株価の不連続性をもたらします。

具体的に言えば、2022年4月1日の株式市場における株価と2022年4月4日の株式市場における株価とは連続していないのです。

このたびの見直しに併せて上場料金を値上げするのならばですが。

コーポレート・ファイナンスにおける純粋な理論上は、上場会社は上場のためのコストを一切負担しません。

一般的なことを言えば、いわゆる「契約」(すなわち、いわゆる「債権債務関係」)には費用がかかりますが、

いわゆる「公務」には費用はかからないのです。

私的に運営されている今日の株式市場は「証券投資の見せかけの戦闘」だと言いたいわけでもありませんし「用済みのもの」である

と言いたいわけでもありませんが、仮に国民が狭い意味での事業利益のみを株式市場における株価へと最大限反映させたいのならば、

世の株式市場は公設・公営であるべきなのです。

資本主義国家においても民主議国家においてもそして非選挙国家においても、です。

{kind=link}

{kind=link}

{kind=link}