2022年5月4日(水)

「本日2022年5月4日(水)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年5月4日)、EDINETに提出された法定開示書類は合計0冊でした。

「本日2022年5月4日(水)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年5月4日)、TDnetで開示された適時開示は合計1本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1236日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜)

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

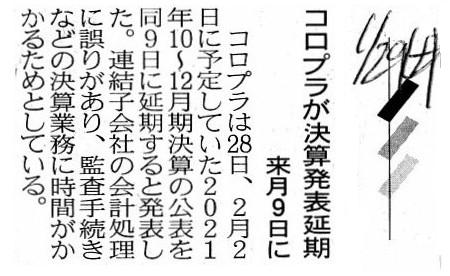

2022年1月29日(土)日本経済新聞

コロプラが決算発表延期 来月9日に

(記事)

2022年1月28日

株式会社コロプラ

2022年9月期第1四半期決算発表日の変更に関するお知らせ

ttps://ssl4.eir-parts.net/doc/3668/tdnet/2073619/00.pdf

(ウェブサイト上と同じPDFファイル)

「PDF印刷・出力したファイル」

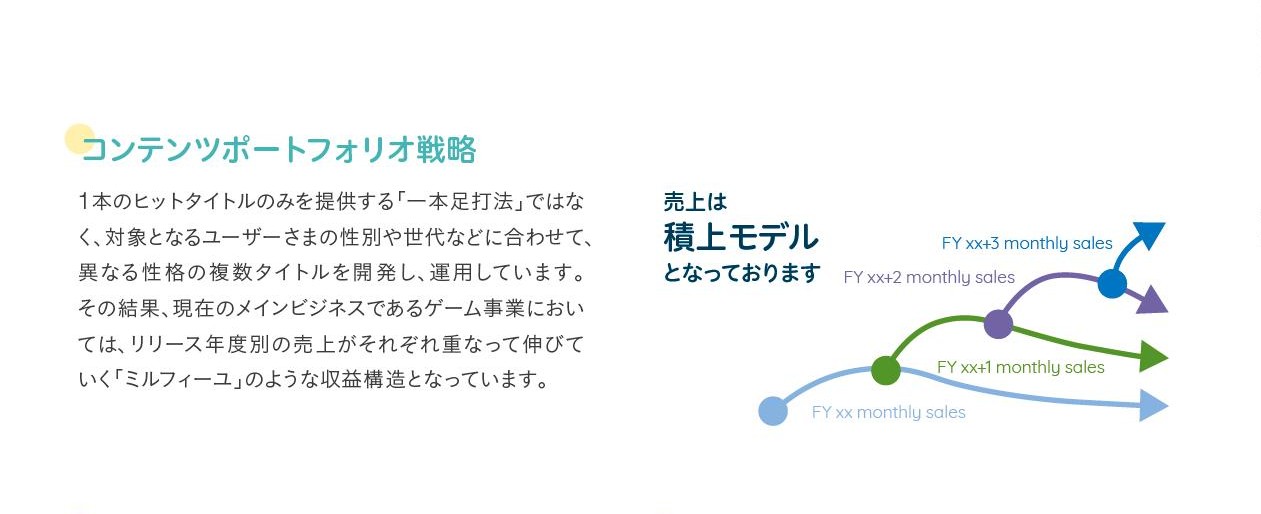

COLOPL Report 2021(ウェブサイト上と同じPDFファイル その1)

(ウェブサイト上と同じPDFファイル その2)コロプラのユニークポイント

(7/52ページ)

株式会社コロプラは「企業のパラスポーツ支援」の一環としてパラアスリートの採用に積極的に取り組んでいるようです↓。

パラスポーツ、企業が支援 アスリート雇用や長期協賛 ESG重視

(日本経済新聞 2021年8月25日 2:00

[有料会員限定])

ttps://www.nikkei.com/article/DGKKZO75096060V20C21A8EA2000/

「キャプチャー画像」

【コメント】

Even if it is a Certified Public Accountant during the

audit-related procedure on a Quarterly Securities Report

that detected errors

in accounting treatments inside consolidated subsidiary companies,

an audit

procedure itself has nothing to do with a "Kessan Tanshin."

A company

prepares a "Kessan Tanshin" "exclusively" namley on a presupposition that a CPA

doesn't see it at all.

In other words, you must regard not that an audit on a

"Kessan Tanshin" has not been completed yet as of a disclosure date

of the

"Kessan Tanshin" but that a "Kessan Tanshin" is not an object of an audit from

the beginning.

Colopl, Inc. merely appropriated a point-out of the errors

which were publicly detected by a Certified Public Accountant

to

privately-prepared financial statements namely a "Kessan Tanshin"

conveniently.

In such a case, generally speaking, I don't know whether a

Certified Public Accountant charges another fee to a company.

And, legally,

whether financial statements are "audited" or "unaudited" depends on a

declaration of an audit opinion.

Even if a company has reflected all of the

point-outs made by a Certified Public Accountant into financial

statements

appearing in a "Kessan Tanshin" totally, those financial

statements nonetheless legally remain "unaudited."

Financial statements

appearing in a "Kessan Tanshin" are legally never able to be changed to

"audited" ones anyhow or other.

たとえ連結子会社内における会計処理の誤りを発見したのが四半期報告書に関する監査関連手続きを行っていた公認会計士であった

のだとしても、監査手続きそれ自体は「決算短信」とは何の関係もありません。

会社は「決算短信」を「排他的に」すなわち公認会計士が「決算短信」を見ることは全くないということを前提に作成するのです。

他の言い方をすれば、「決算短信」に関する監査は「決算短信」の開示日の時点では未了であるというわけではなく、

「決算短信」は始めから監査の対象外なのだと考えなければなりません。

株式会社コロプラは公認会計士が公的に発見をした誤りの指摘を私的に作成する財務諸表にすなわち「決算短信」に流用しただけなのです。

そのような場合、一般的には、公認会計士は会社に対し別料金を請求するのかどうかについては私には分かりませんが。

それから、法律的には、財務諸表が「監査済み」なのか「未監査」なのかは監査意見の表明次第なのです。

たとえ会社は公認会計士が行った指摘の全てを「決算短信」に掲載される財務諸表へ完全に反映しているのだとしても、

その財務諸表はそれでもやはり法律的には「未監査」のままなのです。

「決算短信」に掲載される財務諸表が法律上「監査済み」の財務諸表に変わることはどのようにしても全く不可能なことなのです。

In the most traditional perspective, directors are all "Staffs," and outside

contractors in general such as employees,

business connections, outsourced

workers and licensees of intellectual properties, etc. are all "Lines," I

suppose.

For example, directors of a copany must superintend licensees (of

course, outsiders) of intellectual properties in terms of

whether those

licensees use their rights properly according to a contract between the company

and each licensee.

And, what is more, for example, directors of a company

must superintend purchasers of the company's products in terms of

whether

those purchasers maitain resale prices properly according to a contract between

the company and each purchaser.

Please let me make an unnecessary addition,

but, even an existence of the Labour Standards Law

doesn't change an employee

to an inside person, at least on the principle of a law though.

最も伝統的な見方から言えば、取締役は皆「スタッフ」であり、

被雇用者や取引先や外注労働者や知的財産権の使用許諾者等といった社外の契約者全般は皆「ライン」なのだと思います。

例えば、会社の取締役は、知的財産権の使用許諾者達(もちろん、社外者です)を、それら使用許諾者達は

会社と各使用許諾者との間の契約に従って適正に権利を使用しているのかどうかという観点から監督をしなければならないのです。

そして、さらに言えば、例えば、会社の取締役は、会社の製品の購入者を、それら製品購入者達は

会社と各製品購入者との間の契約に従って適正に再販売価格を維持しているのかどうかという観点から監督をしなければならないのです。

蛇足を言わせて頂きますと、労働基準法があっても被雇用者が社内の人間に変わることはないのです。少なくとも法理上はですが。

{kind=link}

{kind=link}