2022年5月1日(日)

「本日2022年5月1日(日)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年5月1日)、EDINETに提出された法定開示書類は合計0冊でした。

「本日2022年5月1日(日)にTDnetで開示された全ての適時開示」

本日(すなわち、2022年5月1日)、TDnetで開示された適時開示は合計1本でした。

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1233日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜2022年3月31日(木))

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

各コメントの要約付きの過去のリンク その10(2022年4月1日(金)〜)

http://citizen2.nobody.jp/html/202204/PastLinksWithASummaryOfEachComment10.html

2019年3月12日(火)日本経済新聞

米、自社株買いに規制論 民主、格差拡大と批判 ウォール街と対立深まる

(記事)

2019年3月20日(水)日本経済新

ミッキーに3億円「保険」 オリエンタルランド 地震リスクに備え

(記事)

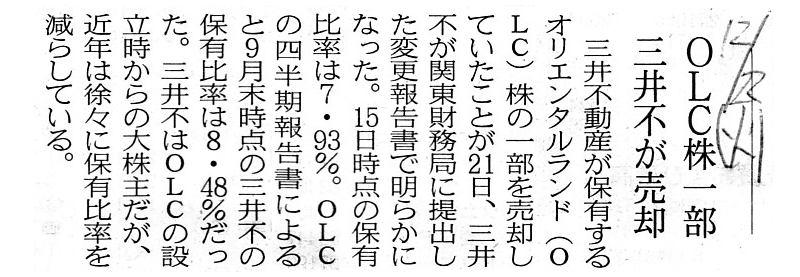

2020年12月22日(火)日本経済新聞

OLC株一部 三井不が売却

(記事)

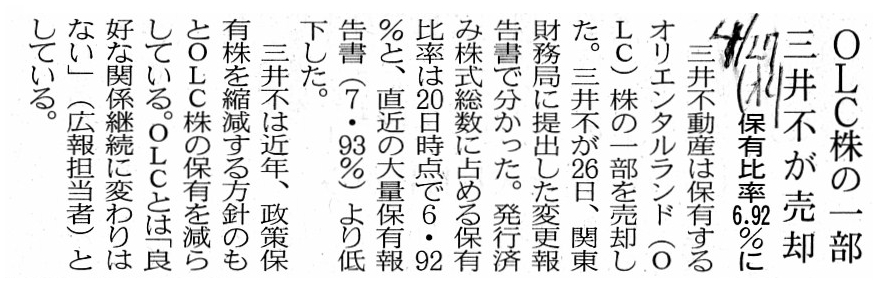

2022年4月27日(水)日本経済新聞

OLC株の一部 三井不が売却 保有比率6.92%に

(記事)

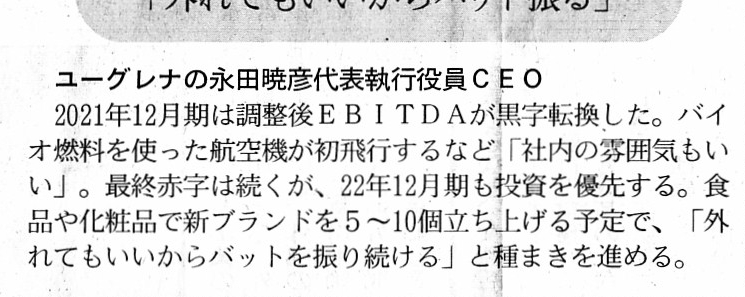

2022年2月17日(木)日本経済新聞

決算トーク

ユーグレナの永田暁彦代表執行役員CEO

「外れてもいいからバット振る」

(記事)

2022年4月20日(水)日本経済新聞

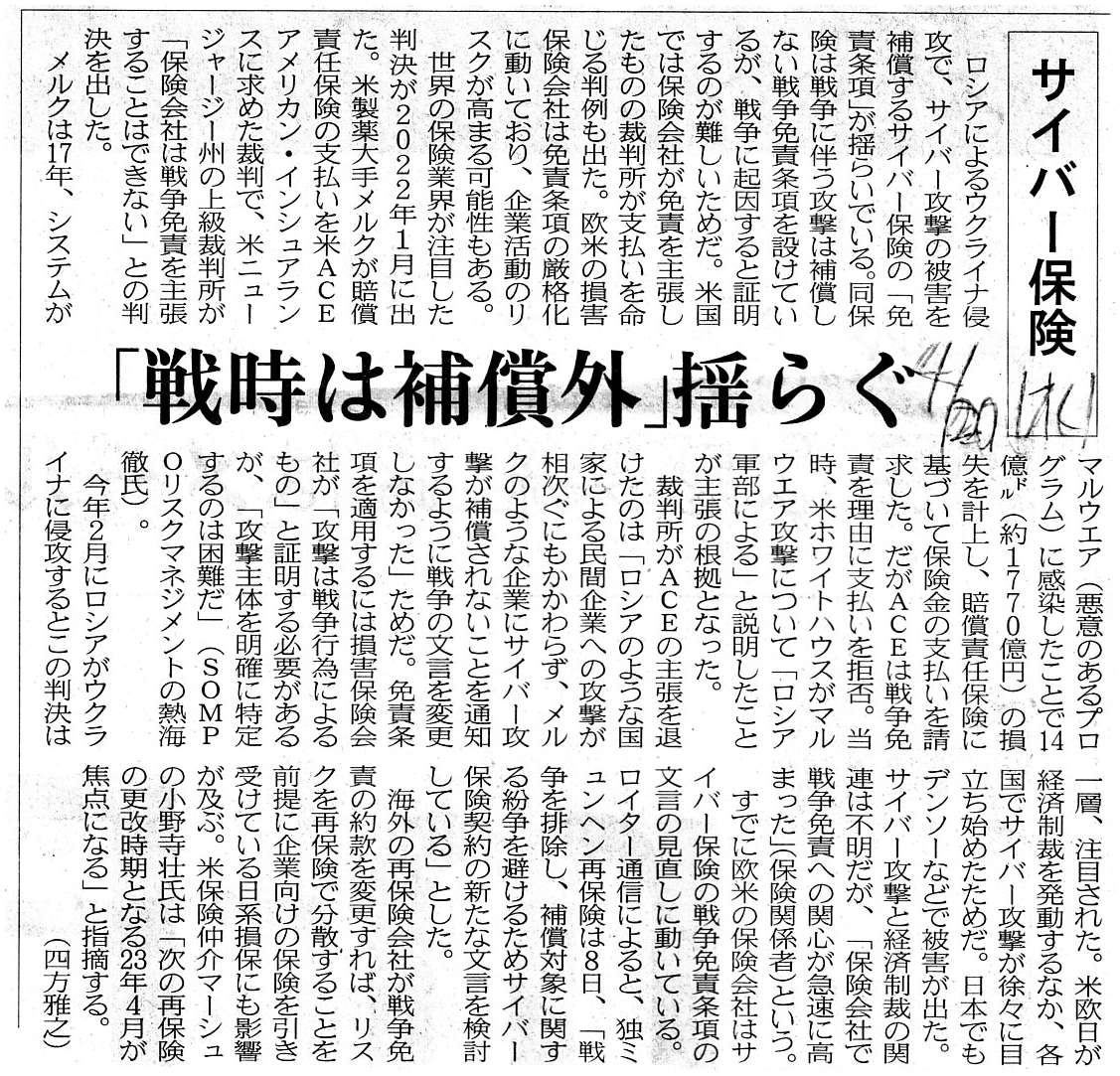

サイバー保険 「戦時は補償外」揺らぐ

(記事)

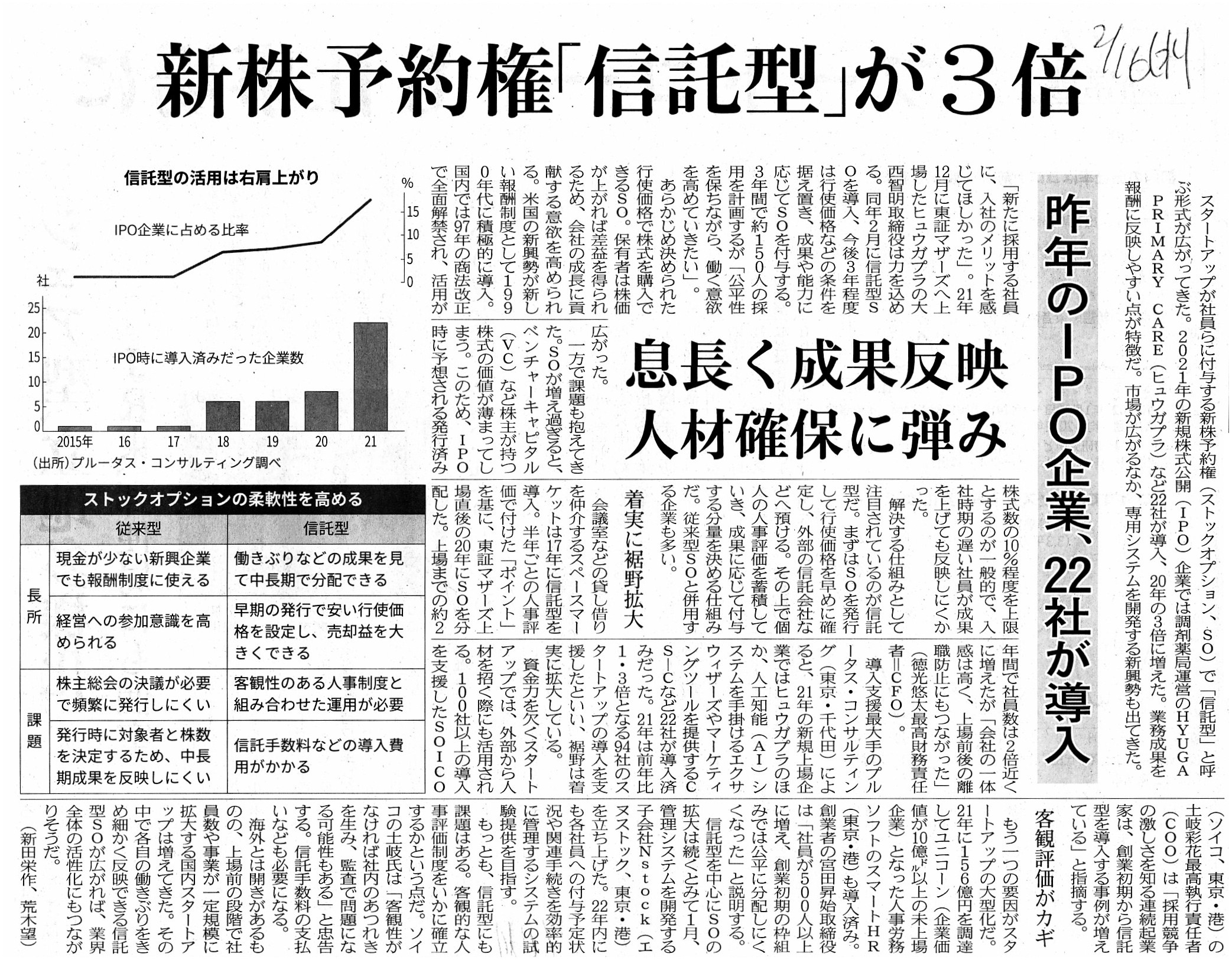

2022年2月16日(水)日本経済新聞

新株予約権「信託型」が3倍 昨年のIPO企業、22社が導入 息長く成果反映

人材確保に弾み

(記事)

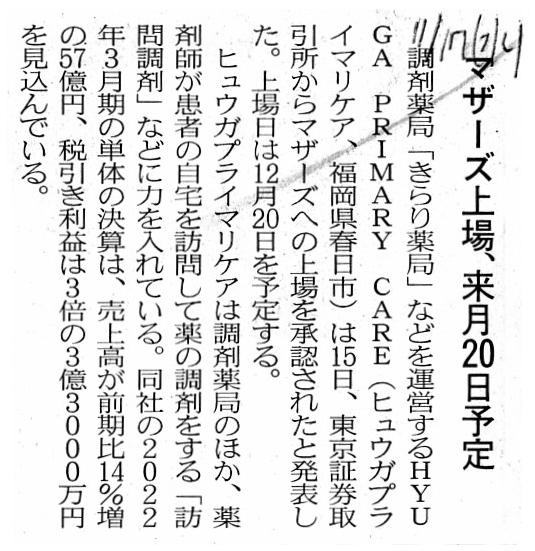

2021年11月17日(水)日本経済新聞

マザーズ上場、来月20日予定

(記事)

【コメント】

約3年前の記事になりますが米国における自社株買いに対する規制論(現米国大統領はこの当時は上院議員をしていたのでしょう)の記事と

東京ディズニーリゾートに関連する記事3本と論点としては以上の記事と関連すると私が考えた記事4本を紹介しています。

「株主に還元されたお金は高成長が見込める事業に再投資される。」というのがまさに「分配と成長の好循環」なのだと私は思います。

それから、OLCの貸出銀行は割り当てられた新株予約権の行使と引き換えに貸出金については債権放棄する、ということなのでしょう。

A "CAT Bond," colloquially-termed, derives from the fact that the 1st issuer

of that bond in Japan was Oriental Land Co., Ltd.

For Mickey Mouse, an image

character of Disney, is a "mouse."

口語表現でいうところの「CAT債」の語源はその債券の日本で最初の発行者がオリエンタルランド株式会社であったことです。

というのは、ディズニーのイメージ・キャラクターであるミッキー・マウスは「ねずみ」だからです。

A "Share Option" in this scene is a "Securing Object."

In order to secure

Redeeming Cash, that "Share Option" is issued.

Otherwise, the Tokyo Disney

Resort will become a "Total Debts Redemption."

That is to say, a lending bank

will attempt to Redeem its lending to the TDR (i.e. Debts of the TDR)

not by

means of going on a date with a lot of families and friends (i.e. "Guests") to

the TDR

but by means of liquidating the TDR itself as a juridical person

(i.e. as a Totality).

この場面における「新株予約権」は「支払いを保証するための目的物」なのです。

弁済金を手に入れるために、その「新株予約権」は発行されるのです。

さもないと、東京ディズニーリゾートは「会社全体の力を出して負債を弁済する」ことになってしまうでしょう。

すなわち、貸出銀行は東京ディズニーリゾートに対する貸出金(すなわち、東京ディズニーリゾートの負債)を、

大勢のご家族やご友人達(すなわち、「お客様」)に東京ディズニーリゾートでデートをしてもらうことによってではなく、

法人としての東京ディズニーリゾートそのものを(すなわち、全体として)清算することによって、弁済してもらおうとすることでしょう。

An "adjusted EBITDA" is able to be explained peacefully,

whereas an

"advocacy of a peace" is not able to be carried out inevitably by civilians.

「調整後EBITDA」は平穏に説明することができますが、

「平和の唱道」を遂行することは民間人には必然的にできないことなのです。

A "bat" which a company swings when it provides new goods and new services is

a "Boosting-an-Accuracy Trial,"

whereas, a "bat" which a company swings as a

measure against climates and earthquakes is a "Blindly-Aimed Target."

That is

to say, you are able to see faces of customers but you are never able to see

causes of natural disasters.

A pharmaceutical dispensing chemist is able to

know a patient's health conditions by means of visiting the patient's

house,

but, for fear of unknown natural disasters, you are not able to

dispense with an insurance notwithstanding the healing conditions.

新製品や新サービスを提供する時に会社が振る"bat"は"Boosting-an-Accuracy

Trial"(正確さを増すための試行錯誤)なのですが、

気候や地震への対応策として会社が振る"bat"は "Blindly-Aimed

Target"(目隠しをしたまま狙いを付けた対象物)なのです。

すなわち、お客様の顔を見ることはできますが、自然災害の原因を知ることは決してできないのです。

薬剤師は患者さんの自宅を訪問することによって患者さんの健康状態を知ることができますが、

あなたは未知なる自然災害を恐れるあまり原状回復条件とは無関係に保険なしで済ますことはできないでいるのです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}