2021年12月3日(金)

「本日2021年12月3日(金)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2021年12月3日)、EDINETに提出された法定開示書類は合計274冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1080日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜)

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

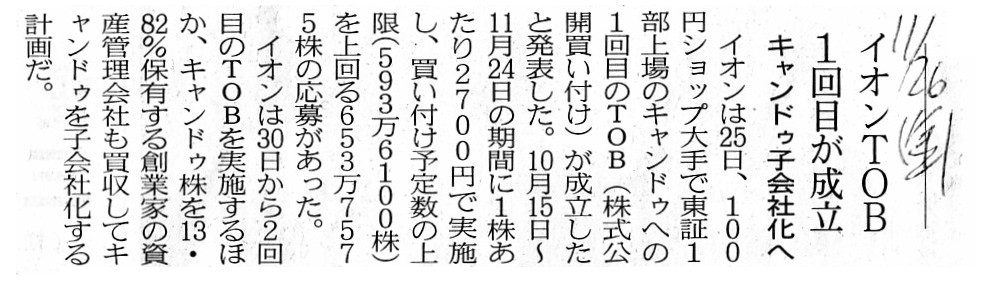

イオンは11月25日、100円ショップ大手のキャンドゥへの1回目の株式公開買い付け(TOB)が成立したと発表した。

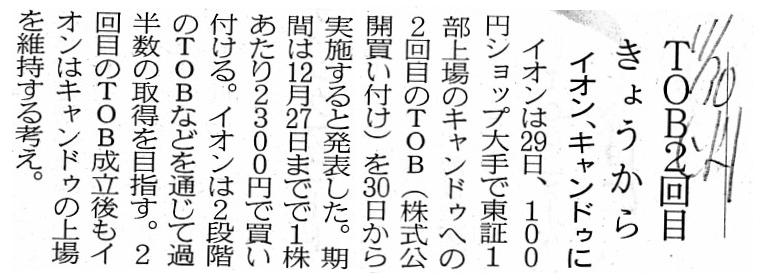

イオンは2回のTOBを通じて、キャンドゥを子会社化する予定だ。

10月15日から11月24日まで1株当たり2700円でTOBを実施、買い付け予定数の上限を上回る653万株余りの応募があった。

これにより、イオンの株式所有割合は37.18%となる。

第2回のTOBは11月30日から12月27日に実施、買い付け価格は2300円とする。2回のTOB終了後、イオンはキャンドゥ創業家の

資産管理会社の株式を買い取り、間接保有を含めて51%以上の株式を取得する。キャンドゥは上場を維持する方針だ。

(ダイヤモンド・リテイル・メディア 2021/11/26

10:07)

ttps://diamond-rm.net/management/99684/

イオン/キャンドゥ株式の第一回公開買付け成立

(流通ニュース 2021年11月25日)

ttps://www.ryutsuu.biz/strategy/n112542.html

「PDF印刷・出力したファイル」

2021年11月26日(金)日本経済新聞

キャンドゥ子会社化へ イオンTOB 1回目が成立

(記事)

2021年11月30日(火)日本経済新聞

イオン、キャンドゥに TOB2回目 きょうから

(記事)

2021年11月30日(火)日本経済新聞 公告

公開買付開始公告についてのお知らせ

イオン株式会社

(記事)

R3.10.29 11:00

イオン株式会社

訂正公開買付届出書 対象: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.11.24 11:48

株式会社キャンドゥ

訂正意見表明報告書 対象: イオン株式会社

(EDINET上と同じPDFファイル)

R3.11.25 16:00

イオン株式会社

公開買付報告書 対象: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.11.30 10:01

イオン株式会社

大量保有報告書 発行: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.12.01 15:16

城戸 一弥

変更報告書 発行: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.12.02 16:02

城戸 一弥

訂正報告書(大量保有報告書・変更報告書) 発行: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.12.01 15:27

城戸 恵子

変更報告書(短期大量譲渡) 発行: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.11.30

イオン株式会社

公開買付開始公告

(EDINET上と同じhtmlファイル)

R3.11.30 10:00

イオン株式会社

公開買付届出書 対象: 株式会社キャンドゥ

(EDINET上と同じPDFファイル)

R3.11.30 10:12

株式会社キャンドゥ

意見表明報告書 対象: イオン株式会社

(EDINET上と同じPDFファイル)

2021年11月25日

イオン株式会社

株式会社キャンドゥ株式(証券コード

2698)に対する公開買付け(第一回)の結果に関するお知らせ

ttps://ssl4.eir-parts.net/doc/8267/tdnet/2053077/00.pdf

(ウェブサイト上と同じPDFファイル)

2021年11月29日

イオン株式会社

株式会社キャンドゥ株式(証券コード

2698)に対する公開買付け(第二回)の開始に関するお知らせ

ttps://ssl4.eir-parts.net/doc/8267/tdnet/2054091/00.pdf

(ウェブサイト上と同じPDFファイル)

2021年11月25日

株式会社キャンドゥ

イオン株式会社による当社株券に対する公開買付け(第一回)の結果

並びに主要株主である筆頭株主、主要株主及びその他の関係会社の異動に関するお知らせ

ttps://www.cando-web.co.jp/corporate/ir/20211125-2.pdf

(ウェブサイト上と同じPDFファイル)

2021年11月29日

株式会社キャンドゥ

イオン株式会社による当社株券に対する公開買付け(第二回)に関する意見表明のお知らせ

ttps://www.cando-web.co.jp/corporate/ir/20211129.pdf

(ウェブサイト上と同じPDFファイル)

「株式会社キャンドゥの過去3ヶ月間の値動き」

「株式会社キャンドゥの過去1ヶ月間の値動き」 「株式会社キャンドゥの過去10日間の値動き」

イオン株式会社が株式会社キャンドゥを連結子会社化することを目的に公開買付を実施するという事例についてのコメント↓。

2021年10月15日(金)

http://citizen2.nobody.jp/html/202110/20211015.html

1999年9月30日以前の伝統的な証券制度においては、上場株式は株式市場内で循環する株式でした。

他の言い方をすれば、投資家は、しばらくしてから同一の株式市場でその株式を売却するということを前提に

株式市場で上場株式を購入していたのです。

その意味において、株式市場の投資家の立場からすると、所有している上場株式を売却する機会は

上場株式を購入する機会よりもはるかに重要だったのです。

当時は、投資家が株式市場で上場株式を取引するためには、所有している上場株式を売却する機会が経常的にもしくは循環して

もしくは周期的にもしくは安定的に維持されていることが絶対的に必要だったのです。

簡単に言いますと、投資家が上場株式を購入した後に所有している上場株式を何とかして売却することができるということが

投資活動の維持に必要な前提だったのです。

万が一上場株式を売却する機会が途切れたとしますと、株式市場における取引そのものも途切れてしまっていたことでしょう。

一方で、1999年10月1日以降の現行の証券制度においては、上場株式は当時とはまた違ったように見なされています。

1つの上場銘柄に関して、株式のいくらかは以前と全く同じように多くの投資家の間で株式市場で循環しており、

株式のいくらかはグループ経営戦略上親会社によって所有されており、

株式のいくらかは将来より高い価格で株式を売却することを目的としている物言う株主によって所有されており、

株式のいくらかは報酬の1つとして発行者の取締役らによって所有されており、

株式のいくらかは資本政策に基づいて発行者自身によって所有されており、

そして株式のいくらかは満了日に発行者が清算されるまで所有するつもりである投資家によって所有されているのです。

上場株式に関するこれらの根本的変遷を鑑みますと、以前の証券制度とは異なり、

上場株式を購入する機会は今では上場株式を売却する機会と同じくらい重要になっているのです。

{kind=link}

{kind=link}

{kind=link}