2022年1月31日(月)

「本日2022年1月31日(月)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2022年1月31日)、EDINETに提出された法定開示書類は合計398冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1139日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜2021年12月31日(金))

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

各コメントの要約付きの過去のリンク その9(2022年1月1日(土)〜)

http://citizen2.nobody.jp/html/202201/PastLinksWithASummaryOfEachComment9.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

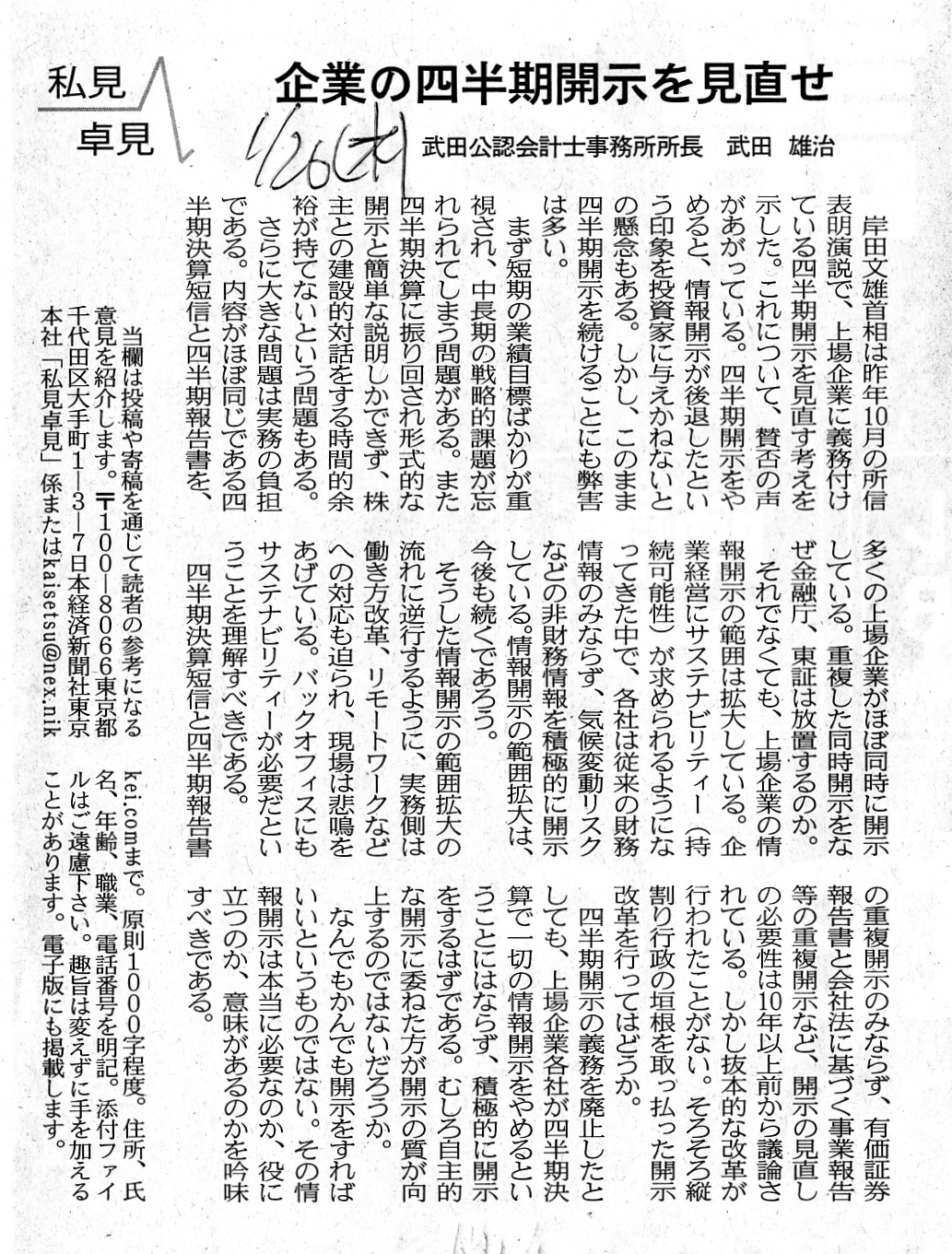

2022年1月26日(水)日本経済新聞

武田公認会計士事務所所長 武田 雄治

企業の四半期開示を見直せ

(記事)

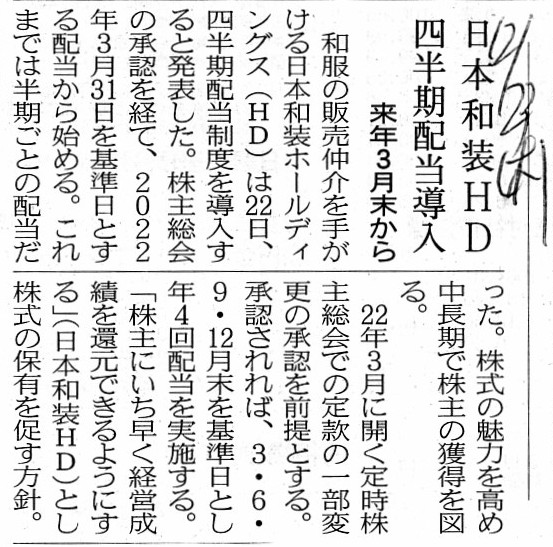

2021年12月23日(木)日本経済新聞

日本和装HD 四半期配当導入 来年3月末から

(記事)

2021年12月22日

日本和装ホールディングス株式会社

四半期配当制度の導入及び定款の一部変更のお知らせ

ttps://ssl4.eir-parts.net/doc/2499/tdnet/2062517/00.pdf

(ウェブサイト上と同じPDFファイル)

(ウェブサイト上と同じPDFファイル)

2022年1月7日

日本和装ホールディングス株式会社

鈴木保奈美さん出演の日本和装の新CM、1月8日よりオンエア!

ttps://ssl4.eir-parts.net/doc/2499/tdnet/2067748/00.pdf

(ウェブサイト上と同じPDFファイル)

「キャプチャー画像」

四半期配当を自社に新たに導入することを意思決定する会社は今でも実際にあるわけです。

実質的に全ての場合において、四半期配当の基準日は実務上は各四半期末日に設定されています。

実務上、例外的な企業は極めて稀です。

それで、それはどういうことを意味するのかと言えば、四半期配当を支払う会社は会社法に基づいて

四半期計算書類を法律上作成しなければならないということです。

より正確に言いますと、会社法上は、配当を支払う会社は、配当を支払う度毎に、配当の基準日時点の計算書類を

作成しなければならないのですが、会社が四半期末日を基準日とする配当―口語表現を用いて言えば「四半期配当」―

を支払うという場合には、いわゆる「四半期財務諸表」がそのまま(すなわち、設えるために追加的に何かを作成する

ことは一切なしに)四半期配当の基準日時点の計算書類としても使えるということになります。

もちろんその会社が四半期毎に定期的に四半期財務諸表を作成してきているのならば、ですが。

総じて言えば、四半期開示制度は、株式市場の投資家が行う投資判断の根拠として役に立つだけではなく、

四半期配当の導入といった会社が行う資本政策の変更にも役立ち、簡単に言えば、四半期開示制度は一挙両得なのです。

ところで、これはまさにちょうど31年前の話になりますが、鈴木保奈美氏は有名なテレビドラマで"Rika

Akana"(赤名リカ)

として出演しましたが、会社は常に「十分な利益剰余金」に基づいて配当を支払わなければならないのです。

ちなみに、このドラマの中で私が最も好きな台詞は、

「もう他の誰かじゃやだよ(あなたの代わりの人を好きになりたいとは思いません)。」です。

あっ、過去のプレスリリースを読んでいておかしな記述があることに今気が付いたのですが、

今まで中間配当を支払ってきているという事実から判断すると、

日本和装ホールディングス株式会社は今以上に定款を変更する必要はありません。

もちろん日本和装ホールディングス株式会社は今まで中間期間毎に適法に中間配当を支払ってきているのならば、ですが。

{kind=link}

{kind=link}