2021年12月10日(金)

「本日2021年12月10日(金)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2021年12月10日)、EDINETに提出された法定開示書類は合計411冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1087日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜)

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

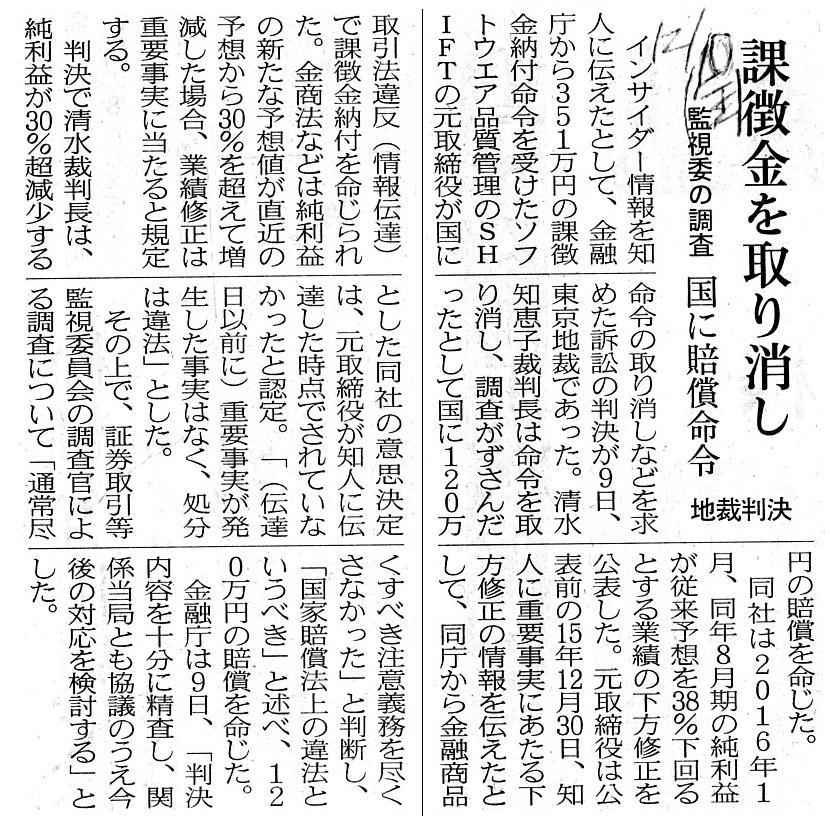

2021年12月10日(金)日本経済新聞

課徴金を取り消し 監視委の調査 国に賠償命令 地裁判決

(記事)

「会計学辞典 第五版」 森田哲彌、宮本匡章 編著 (中央経済社)

「法人実在説、法人擬制説」("Existential Juridical Person Perspective"、"Ficititious Juridical Person Perspective")

"Essential perspective on a juridical person."(「法人の本質観」)

「PDFファイル」

「キャプチャー画像」【コメント】

会社の取締役が公表前に知人に重要事実を伝えたことは金融商品取引法違反(情報伝達)に該当するか否かについて争われた裁判

(課徴金納付命令の取り消しを求めた訴訟)に関する記事を紹介していますが、まず重要な部分を引用したいと思います。

>判決で清水裁判長は、純利益が30%超減少するとした同社の意思決定は、元取締役が知人に伝達した時点でされていなかった

>と認定。「(伝達日以前に)重要事実が発生した事実はなく、処分は違法」とした。

私は記事を一読してすぐに、「取締役による情報伝達と会社の意思決定が何の関係があるんだ?」と思いました。

取締役個人が知人に情報を伝達したわけなのだから、会社や会社の意思決定(取締役会決議のことでしょう)は全く関係ないはずだ

と思ったわけなのですが、同時に私の頭の中には「取締役は会社の連帯債務者である。」というかつての規定が思い浮かびました。

「ひょっとしたら、この考え方は正しいのかもしれない。」と思い始め、頭の中であれこれ考えてみたのですが、

極端に思えるかもしれませんが、ある1つの結論に辿り付きました。

それは、観念的な言い方になりますが、「純粋に理論上の(最初期の商法の)法人には自然人はいない。」という考え方です。

「業務執行に関連して取締役個人が何かをするという考え方自体がない。」という解釈にならないだろうかと思ったわけです。

「業務執行に関して取締役が行うのは会社の意思決定(取締役会決議)で決まったことのみである。」という考え方に基づくならば、

会社の意思決定がなされていないならばその業務執行もない(この事例に即して言えば、会社に重要事実が発生した事実はない)、

という解釈になるなと私は思ったわけです。

当時取締役が知人に伝達した内容は嘘やデタラメや全く未確定の情報に過ぎない、という捉え方になるように思いました。

「会社にあるのは会社の意思決定と会社による業務執行だけである。」、これが純粋な理論上の法人だと私は思いました。

それで、「そう言えば、『法人の定義』のような話が何かあったな。」と思い出し、関連する資料として、会計学辞典から

「法人実在説」と「法人擬制説」についての説明をスキャンして紹介していますので、参考にして下さい。

また、これらの説明を叩き台にして、自分なりに「法人の本質観」についてまとめてみましたので、参考にして下さい。

端的に言えば、現行の会社法における株式会社は「法人実在説」と「法人擬制説」の折衷的な法人なのです。

There did not at all used to exist a notion "natural person" in a juridical

person.

That is to say, at least in theory and in prescriptions of the most

original Commercial Code, notionally speaking,

a person that exectutes

operations of a company is not a natural person (i.e. a director) but still a

juridical person.

Therefore, the most original Commercial Code used to be

based on the "existential juridical person perspective."

Soon after that, the

Commercial Code was amended completely in a sense

so that a juridical person

was based on the "ficititious juridical person perspective."

That is to say,

it was amended so that a director assumed joint and several obligations with a

juridical person.

The current Companies Act is based on a mix of namely an

eclectic perspctive of

the "existential juridical person perspective" and the

"ficititious juridical person perspective."

かつては法人には「自然人」という概念は一切ありませんでした。

すなわち、少なくとも理論上はそして最初期の商法の条文では、概念的に言えば、

会社の業務を執行する人は自然人(すなわち、取締役)ではなくやはり法人なのです。

したがって、最初期の商法は「法人実在説」に立脚していたのです。

その後すぐに、法人は「法人擬制説」に立脚するというふうに商法はある意味完全に改正されました。

すなわち、取締役は法人の連帯債務者であるというふうに商法は改正されました。

現行の会社法は、「法人実在説」と「法人擬制説」を混合した説すなわち折衷した説に立脚しているのです。

If a juridical person is "existential," then a director is legally

totally not liable.

If a juridical person is "fictitious," then a direcor is

legally totally liable.

And, this is merely my personal opinion, but, as the

related argument with the above, concerning the securities system,

if a

juridical person is "existential," then an Annual Securities Report is stated

totally on a juridical person itself.

If a juridical person is "fictitious,"

then an Annual Securities Report is stated

basically only on directors of a

juridical person (and, perhaps, in practice, partly on contents

of that

juridical person such as, for example, financial statements).

To put it

simply, in the former perspective, a juridical person is a juridical

person

and in the latter perspective, a juridical person is a director.

法人が「実在法人」なのであれば、取締役は法律上損害賠償責任を一切負いません。

法人が「擬制法人」なのであれば、取締役は法律上損害賠償責任を全面的に負います。

それから、これは私個人の考えに過ぎませんが、上記の議論と関連する議論としてですが、証券制度に関して言いますと、

法人が「実在法人」なのであれば、有価証券報告書は全面的に法人そのものに関して記載されます。

法人が「擬制法人」なのであれば、有価証券報告書は基本的には法人の取締役に関してのみ記載されます

(そして、おそらく実務上はその法人の内容―例えば財務諸表―に関しても一部は記載されるでしょう)。

簡単に言えば、「法人実在説」では法人とは法人であり、「法人擬制説」では法人とは取締役なのです。

SHIFT Inc, is a professional group of a software test, but,

a

juridical person in the "ficititious juridical person perspective" is an

assembly of directors.

株式会社SHIFTはソフトウェアテストのプロ集団ですが、「法人擬制説」における法人は取締役の集合体なのです。

{kind=link}