2021年9月22日(水)

「本日2021年9月22日(水)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2021年9月22日)、EDINETに提出された法定開示書類は合計219冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1008日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)~2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)~2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)~2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)~2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)~2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)~2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)~2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)~)

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2021年9月20日(月)日本経済新聞

買収提案「比較できない」 関西スーパー株主、開示ルール曖昧

(記事)

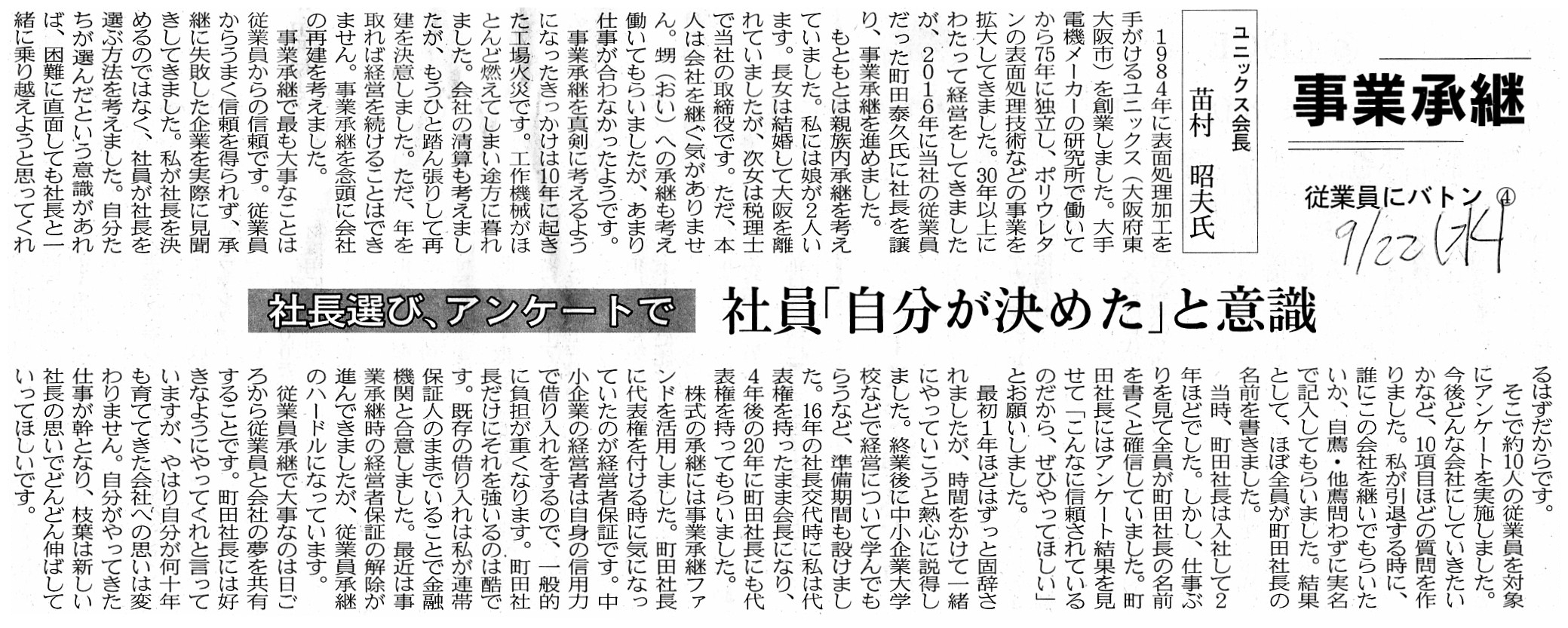

2021年9月22日(水)日本経済新聞

オーケー社長 株主に賛同呼びかけ 関西スーパー買収で

(記事)

2021年9月22日(水)日本経済新聞

事業承継 従業員にバトン ④

ユニックス会長 苗村

昭夫氏

社長選び、アンケートで 社員「自分が決めた」と意識

(記事)

2021年9月21日

オーケー株式会社

昨日の一部報道について

ttps://ok-corporation.jp/media/001/202109/

%E4%B8%80%E9%83%A8%E5%A0%B1%E9%81%93%E3%81%AB%E3%81%A4%E3%81%84%E3%81%A6_20210921.pdf

(ウェブサイト上と同じPDFファイル)

注:

エイチ・ツー・オー

リテイリング株式会社からも株式会社関西スーパーマーケットからも、

関連するプレスリリースは特に発表されていないようです。

【コメント】

It is not a party who intends to actually acquire a share such as a

potential parent company or a potential controlling

shareholder but a party

who does not intend to acquire the share such as an investment fund who fights

for a proxy.

In other words, most typically, a strategic buyer doesn't fight

for a proxy.

In this case, OK Corporation is clearly a strategic buyer.

Therefore, it is not proxies of Kansai Super Market Ltd., etc. but

professional shoppers who are quite a connoisseur

of super markets and who

are always checking a lot of fliers that OK Corporation must fight for.

I

understand that shareholders, who should fundamentally be the supremet

decision-maker of an M&A,

of Kansai Super Market Ltd. are currently not

able to compare the H2O Retailing plan and the OK plan.

Then, how about an

idea that the 3 parties in question leave shoppers of Kansai Super Markt Ltd. to

decide

which company ought to acquire Kansai Super Market Ltd. instead of the

sharaholders.

What is the most important thing concerning a business

succession is a trust from employees,

but, what is the most important thing

concerning an M&A of retailers is a post-merger inducement to shop for

shoppers.

A change of a parent company of a super market can sometimes impede

the current shoppers from going shopping.

For some shoppers believe that the

Postal Savings have been misappropriated to the war expenditures

such as a

purchase of tanks and a subscription of wartime government bonds.

By the way,

if the well-known vogue concerning a decision-making of these days is

given,

what you call a "third party committee" or a "special committee" ought

to consist

not of Outside Directors but of independent learned persons.

A

reason for it is that, all things considered, Outside Directors are one of the

company organs.

A Finanicial Auditor on a basis of the Companies Act, which

is one of the company organs, accompanies directors,

whereas an Outside

Director on a basis of the Companies Act, which is the same as the

above,

ultimately threatens to accommodate directors' wishes, saying

"Consider it done."

委任状を争奪するのは、将来の親会社や将来の支配株主といった実際に株式を取得することを目論む当事者ではなく、

投資ファンドといった株式を取得することは目論んではいない当事者なのです。

他の言い方をすれば、最も典型的なことを言えば、ストラテジック・バイヤーは委任状を争奪しないのです。

この事例では、オーケー株式会社は明らかにストラテジック・バイヤーです。

したがって、オーケー株式会社が争奪しなければならないのは、株式会社関西スーパーマーケットの委任状などではなく、

スーパーマーケットに対する目が肥えておりいつも数多くのチラシをチェックしているプロの買い物客達なのです。

株式会社関西スーパーマーケットの株主は―株主は本来M&Aの最高の意思決定者であるべきなのですが―現在、

H2Oリテイリング案とオーケー案を比較することができないでいると聞いています。

それならば、件の3社は株式会社関西スーパーマーケットをどちらの会社が取得するべきか株主の代わりに

株式会社関西スーパーマーケットの買い物客に決めてもらうという案はどうでしょうか。

事業承継で最も大事なことは従業員からの信頼ですが、

小売店のM&Aで最も大事なことは統合後に買い物客に買い物をしようという気を起こさせる誘引なのです。

スーパーマーケットの親会社が変わると、従来からの買い物客が買い物に行く足が遠のくことがあるのです。

郵便貯金は戦車の購入や戦時国債の購入のような軍事費に転用されていると信じる買い物客もいるのですから。

ところで、意思決定に関するあの有名な最近の流行を所与のこととしますと、

いわゆる「第三者委員会」や「特別委員会」は、社外取締役ではなく、独立した有識者で構成されているべきなのです。

その理由は、結局のところ、社外取締役というのは会社機関の1つだからです。

会社法上の会計監査人は―会計監査人は会社機関の1つなのですが―取締役と一緒に伴走をするのですが、

会社法上の社外取締役は―同上―結局「かしこまりました。」と言って取締役らの願いを聞き入れる恐れがあるのです。

{kind=link}

{kind=link}

{kind=link}