2021年9月19日(日)

「システムメンテナンスに伴うサービスの一時停止のお知らせ」

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計1004日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜2021年4月30日(金))

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

各コメントの要約付きの過去のリンク その8(2021年5月1日(土)〜)

http://citizen2.nobody.jp/html/202105/PastLinksWithASummaryOfEachComment8.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

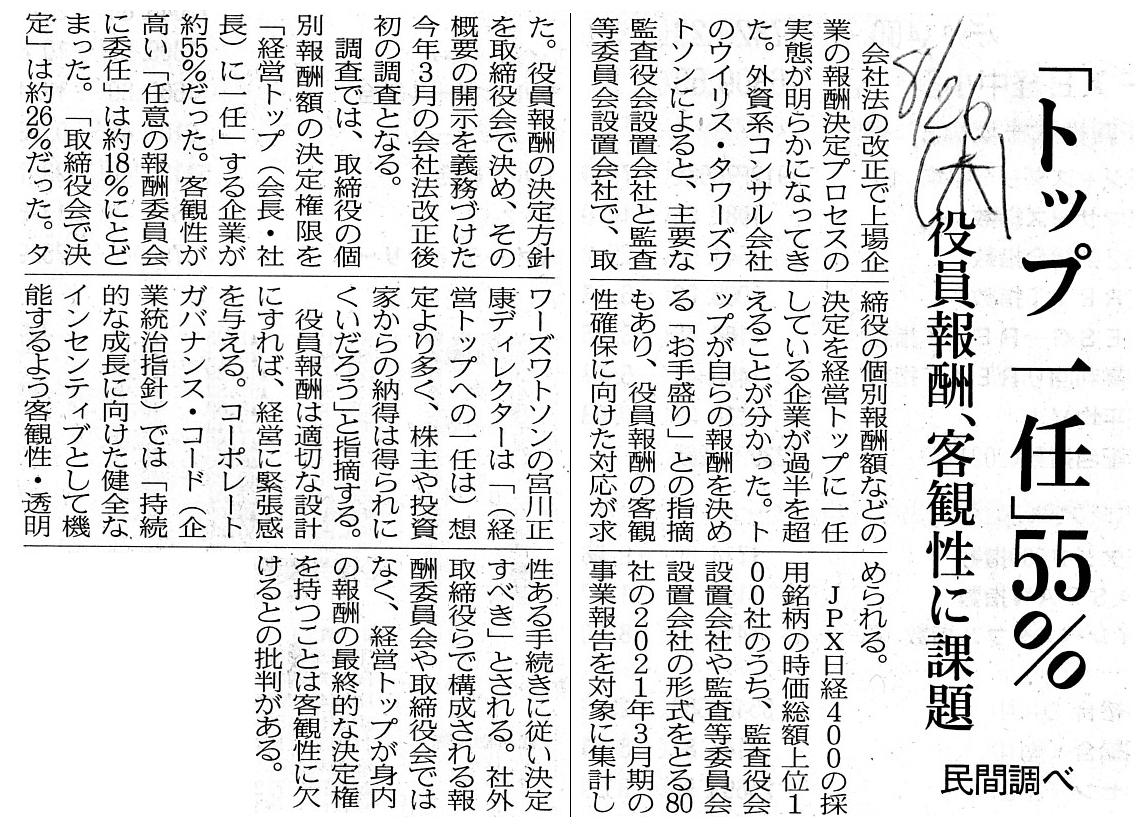

2021年8月26日(木)日本経済新聞

「トップ一任」55% 役員報酬、客観性に課題 民間調べ

(記事)

2020年11月27日

株式会社ユーグレナ

第16期定時株主総会招集ご通知

ttps://www.euglena.jp/ir/meeting/pdf/dai16_syoushu_euglena.pdf

(ウェブサイト上と同じPDFファイル)

注:

主要上場企業80社の2021年3月期の事業報告を対象に集計したところ、取締役の個別報酬額の決定権限を

「経営トップ(会長・社長)に一任」する企業が約55%だった、とのことです。

しかし、日本では、特に大企業では社長の役割はむしろ監査と指名と報酬であるように思いました。

松下幸之助の言葉「任せて任せず。」とはそういう意味なのではないだろうかと思いました。

社外の人材が決めさえすれば株主や投資家は納得をするというものでは決してないと思いました。

それから、一般に会社法に基づく監査と金融商品取引法に基づく監査とは実質的に区分できないと言われています。

しかし、理論的には次のようなことが言えます。

○会社法に基づく計算書類の作成者⇒取締役(会社内部の人物)

○金融商品取引法に基づく財務諸表の作成者⇒独立者(会社外部の人物)

このような見方をしますと、会社法に基づく監査と金融商品取引法に基づく監査とはむしろ業務内容として本質的に全く異なる

という言い方ができると私は考えます。

抽象的に表現するならば、会社法に基づく監査は「一緒に作る」、すなわち、"accompany"(伴走する、もしくは、伴奏する)、

金融商品取引法に基づく監査は「完成品を評する」、すなわち、"acknowledge"(承認する)、

という本質的違いが理論的にはあると私は考えます。

日本では、最高経営責任者("CEO")の職域は伝統的に監査と指名と報酬であるように私には思えます。

仮に私のこの理解が正しいならば、この文脈における「CEO」は、"Chief

Executive Officer"(最高経営責任者)ではなく、

どちらかと言えば"Chief Encouraging

Officer"(最高激励責任者)ということになります。

そして、日本で誰が次期総理になるのかは私には分かりませんが、この文脈における「トップ」は

"Totally

Organizing Presenter" (会社全体を編制して表現をする者)であり、

その意味は概ね"Solely Ruling

Officer"(単独支配責任者)という意味です。

この文脈における「トップ」は、「競技者」(すなわち、業務執行者)ではなく、「表現者」(すなわち、監督者)なのです。

この文脈における「トップ」は、社内の誰に対しても「俺がルールブックだ。」と言えなければならないのです。

そして、さらに言えば、会社に万一のことが起こった時は、この文脈における「トップ」は、

「弊社に『さようなら』と言うのは私自身が最後の人物になります。」と自ら進んで高らかに宣言できなければならないのです。

The fact that shareholders are satisfied and the fact that investors are

safisfied are different from each other.

Shareholders peruse a "Business

Report" on a basis of the Companies Act never on a presupposition that

they

trade shares, whereas investors peruse an "Annual Securities Report" on a basis

of the Financial Instruments

and Exchange Act exclusively on a presupposition

that they trade shares.

In theory, even a "Financial Auditor" on a basis

of the Companies Act is an inside company organ, actually.

Whether both

shareholders and investors are satisfied with the amount of a remuneration to

each director or not

depends not on who determines or on in accordance with

which procedure but exactly on that amount itself.

Stakeholders regard any

pay by a company as a pay made to suit the company as long as a company organ

determines it.

Stakeholders don't know whether management and "Outside

So-and-sos" go to a "golf club" together on the weekend

or go through an

argument inside and outside a board of directors like the "Fight Club"

every day of a week.

株主が納得をすることと投資家が納得をすることは違うのです。

株主は会社法に基づく「事業報告」を株式の取引を行うことは全く前提とはしないで閲覧するのですが、

投資家は金融商品取引法に基づく「有価証券報告書」を株式の取引を行うことのみを前提として閲覧するのです。

理論的には、会社に基づく「会計監査人」でさえ実は社内の会社機関なのです。

株主と投資家が取締役の個別報酬額に納得をするか否かは、誰が決定したのかやどの手続きに従ったのかではなく、

まさにその報酬額そのものによって決まるのです。

利害関係者は、会社によるいかなる支払いも、それを会社機関が決定している限り、お手盛りの支払いであると見なすのです。

利害関係者は、経営陣らと「社外何々」らとが、週末に一緒に「ゴルフクラブ」に行っているのか、それとも、

毎日欠かさず取締役会の内外で「ファイト・クラブ」のように議論を行っているのか、どちらなのかを知らないのです。

{kind=link}