2021年3月31日(水)

「本日2021年3月31日(水)にEDINETに提出された全ての法定開示書類」

Today

(i.e. March 31st, 2021), 750 legal disclosure documents have been submitted to

EDINET in total.

本日(すなわち、2021年3月31日)、EDINETに提出された法定開示書類は合計750冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計833日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜)

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

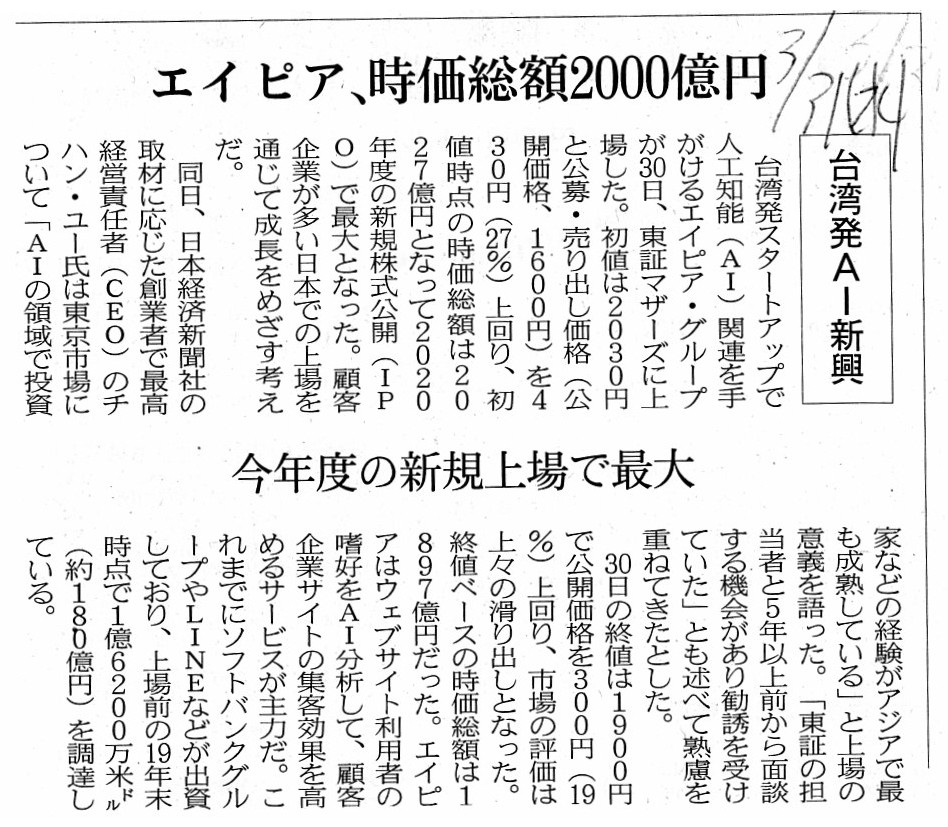

2021年3月31日(水)日本経済新聞

エイピア、時価総額2000億円 台湾発AI新興 今年度の新規上場で最大

(記事)

【コメント】

記事は直接的には関係ないのですが、現行の証券制度における「公開価格」の決定方法について一言だけ書きたいと思います。

2021年3月28日(日)のコメントで、「ブック・ビルディング」の手続きに関連して、私は次のように書きました。

>「主幹事証券会社が決定する公開価格」は「どちらの株式市場に上場するか?」次第で異なることになるのです。

この論点に関してなのですが、私は今でも上記の結論が正しいと思っています。

今では主幹事証券会社は事務手続き上公開価格を決定はしますが株式の本源的価値を算定したりはしないのです。

今日は何年も前のことを思い出したのですが、「ブック・ビルディング」の手続きが分かっている人がほとんどいない

というのが実態なのかもしれないなと思いました(このことは私にとってはSF映画のような驚くべきことなのです)。

「ブック・ビルディング」の手続きに関して、今日は次のような図を描いてみましたので参考・理解のヒントにして下さい↓。

"Imagine that each stock market has a single investor inside

it."

(「各株式市場にはただ1人の投資家しかいないという状況を頭に思い浮かべてみて下さい。」)

Abstractly speaking, formerly a leading securities company for an

underwriting used to calculate and determine,

whereas now investors inside a

stock market form and a leading securities company for an underwriting

determines.

In other word, now a leading securities company for an

underwriting is not able to direct an intrinsic value

of a share on a

theoretical presupposition of the current securities system after October 1st,

1999.

To put it simply, an opening price used to be a result of a

calculation, whereas it is now a consequence of a hearing.

抽象的に言えば、かつては主幹事証券会社が算定をし決定をしていたのですが、

今では株式市場の投資家が形成をし主幹事証券会社が決定をするのです。

他の言い方をすれば、1999年10月1日以降の現行の証券制度における理論的前提を踏まえれば

今では主幹事証券会社が株式の本源的価値を指図することはできないのです。

簡単に言えば、公開価格は、かつては算定の結果だったのですが今ではヒアリングの結果なのです。

1999年9月30日以前の伝統的な証券制度における公開価格は、

排他的に(すなわち、株式市場内の投資家からの需要とは全く無関係に)主幹事証券会社が決定していました。

しかるに、1999年10月1日以降の現行の証券制度における公開価格は、

放出された供給と関連を持たせつつ株式市場内の投資家からの返答と反応を通じて決定されるのです。

In a "Book-building" procedure, a person in charge asks each investor,

"At

what price do you want to buy this share?"

「ブック・ビルディング」の手続きにおいて、

担当者は各投資家に「あなたはこの株式をいくらで買いたいですか?」と尋ねるのです。

Fishes are the well-known product in Okinawa,

but the origin of the

well-known video game "DARIUS" is not an acronym of the sentence

above.

Please let me be audacious, but it seems to me that

those who are

well acquainted with the traditional secrities system before September 30th,

1999

are like a fish out of water when they deal with the current securities

system after October 1st, 1999.

Notwithstanding the fact that an investor

answers, "I want to buy at 710 yen,"

if a leading securities company for an

underwriting determines an opening price as "700 yen,"

the investor will ask

the securities company, "Do you have a health-insurance certificate?"

And,

quite contrary to the traditional secrities system before September 30th,

1999,

on the current securities system after October 1st, 1999, a supply of a

share (i.e. the number of a share

to be sold by the existing shareholders and

to be issued by an issuer itself) can also be said to be

one of the important

factors when an opening price is formed among investors inside a stock market.

魚は沖縄の名産品なのですが、

有名なテレビゲームである「ダライアス(DARIUS)」の語源は上記の文章の頭文字を取ったものではありません。

僭越ではありますが、1999年9月30日以前の伝統的な証券制度に精通している人たちは

1999年10月1日以降の現行の証券制度を取り扱うとなると陸に上がった魚のようだと私には思えます。

投資家が「私は710円で買いたいと思います。」と返答しているにも関わらず主幹事証券会社が公開価格を「700円」

と決定するならば、その投資家はその主幹事証券会社に「保険証持ってる?」と尋ねることでしょう。

それから、1999年9月30日以前の伝統的な証券制度とは正反対に、1999年10月1日以降の現行の証券制度においては、

株式の供給(すなわち、既存株主によって売却される株式数と発行者自身によって発行される株式数)もまた

株式市場の投資家の間で公開価格が形成されるに際して重要な要素要因の1つだと言うことができるのです。

,750LegalDisclosureDocumentsHaveBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}