2021年3月7日(日)

「本日2021年3月7日(日)にEDINETに提出された全ての法定開示書類」

Today

(i.e. March 7th, 2021), 0 legal disclosure document has been submitted to EDINET

in total.

本日(すなわち、2021年3月7日)、EDINETに提出された法定開示書類は合計0冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計809日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜)

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

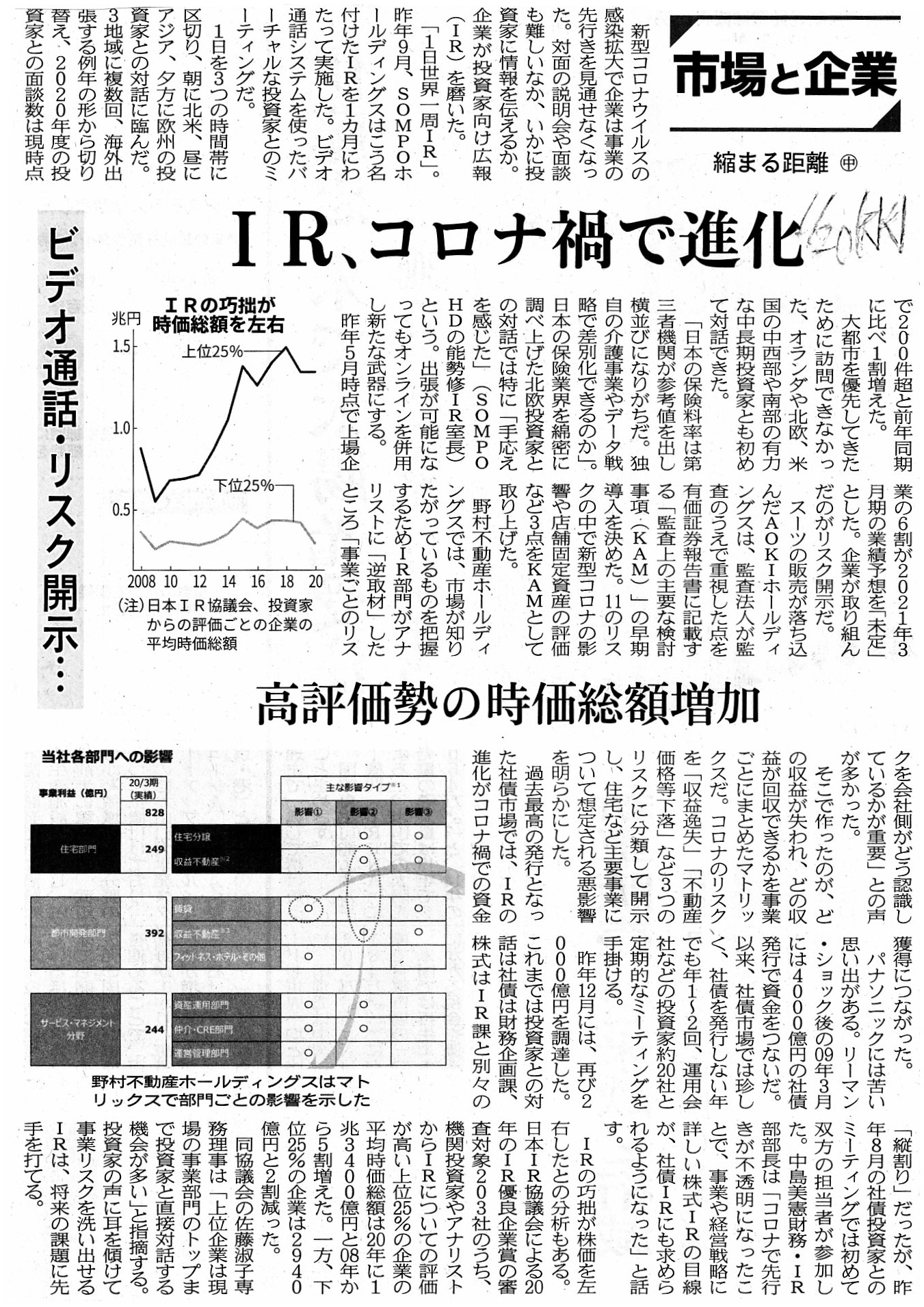

2021年1月20日(水)日本経済新聞

市場と企業 縮まる距離 中

IR、コロナ禍で進化 高評価勢の時価総額増加 ビデオ通話・リスク開示・・・

(記事)

2021年1月21日(木)日本経済新聞

市場と企業 縮まる距離 下

ESG

4年越しの成果 主要指数がリコーに好評価 情報開示「物足りぬ」の声も

(記事)

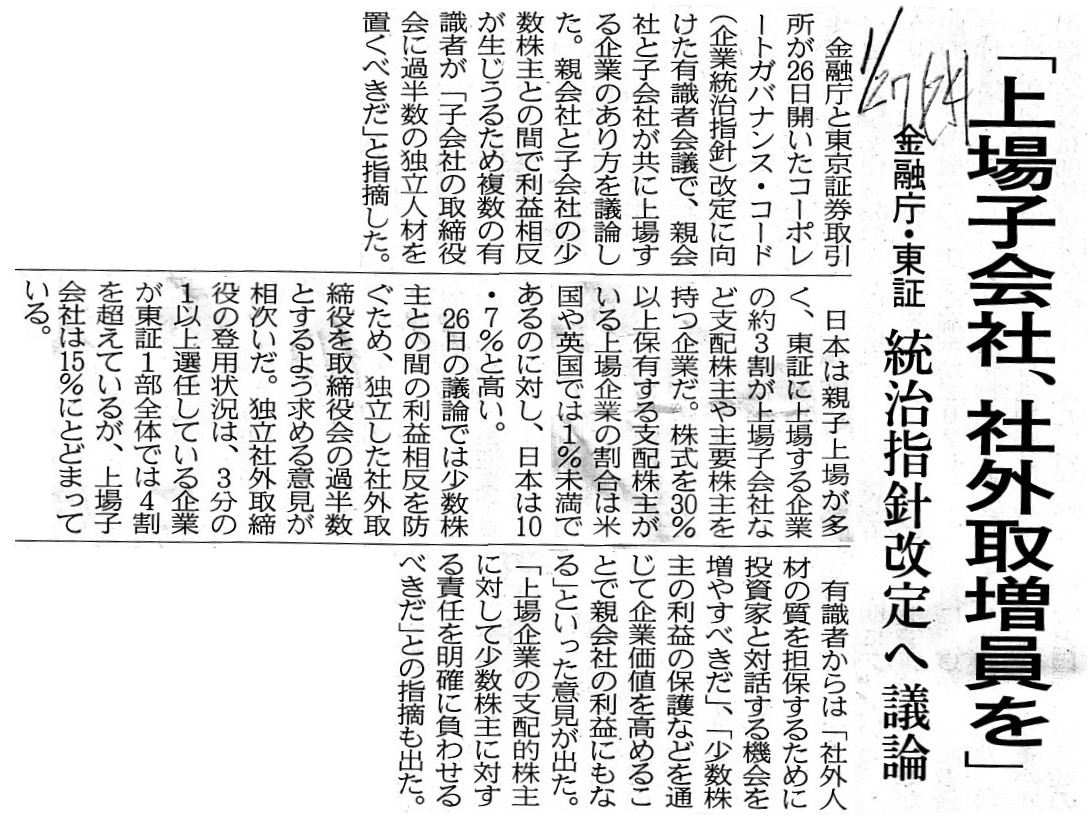

2021年1月27日(水)日本経済新聞

「上場子会社、社外取増員を」 金融庁・東証 統治指針改定へ議論

(記事)

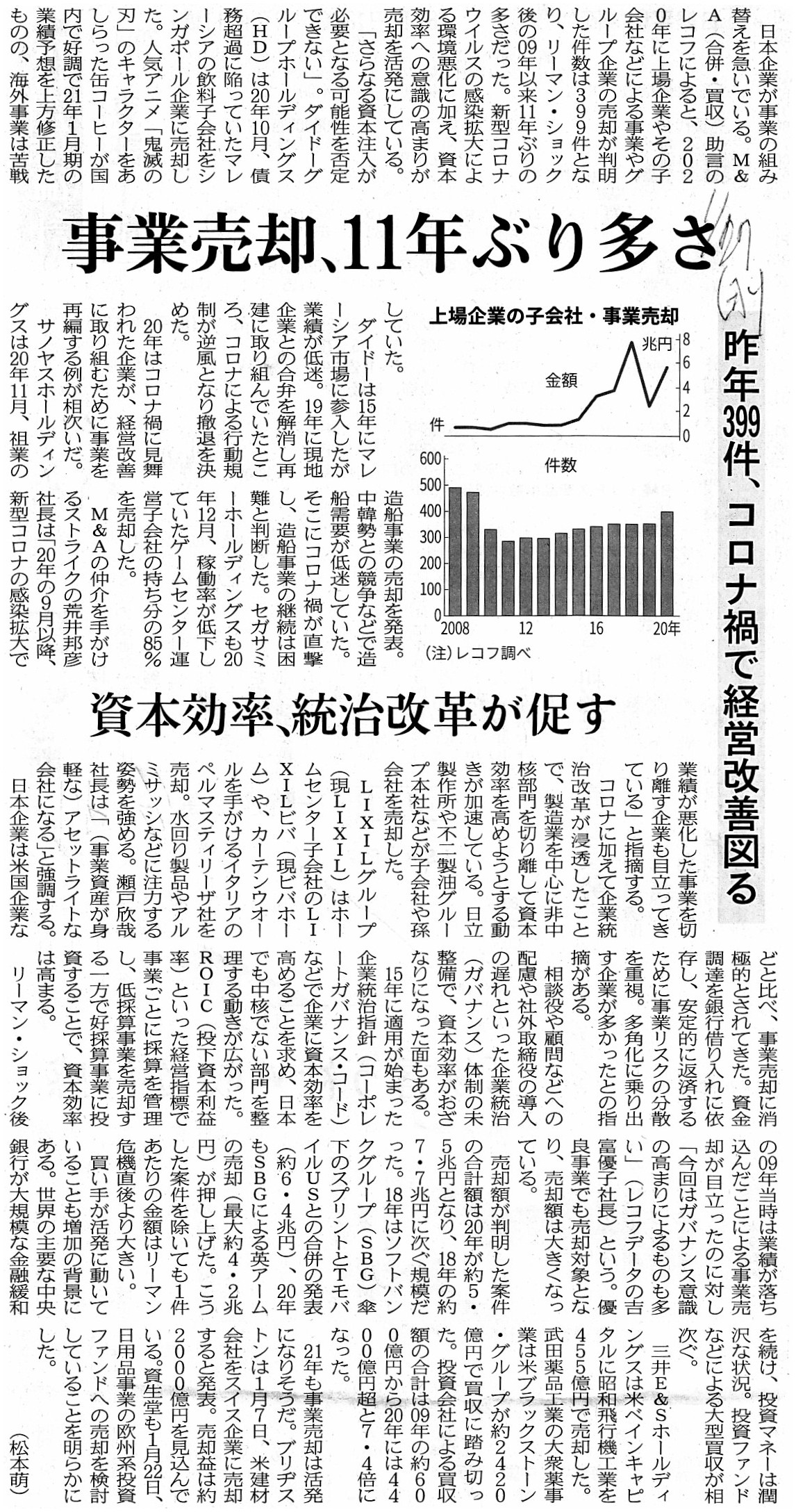

2021年1月27日(水)日本経済新聞

事業売却、11年ぶり多さ 昨年399件、コロナ禍で経営改善図る 資本効率、統治改革が促す

(記事)

2020年9月26日(土)日本経済新聞

減損倍増、最大の4.2兆円 前期 車や鉄鋼が巨額計上 今期も相次ぐ懸念

(記事)

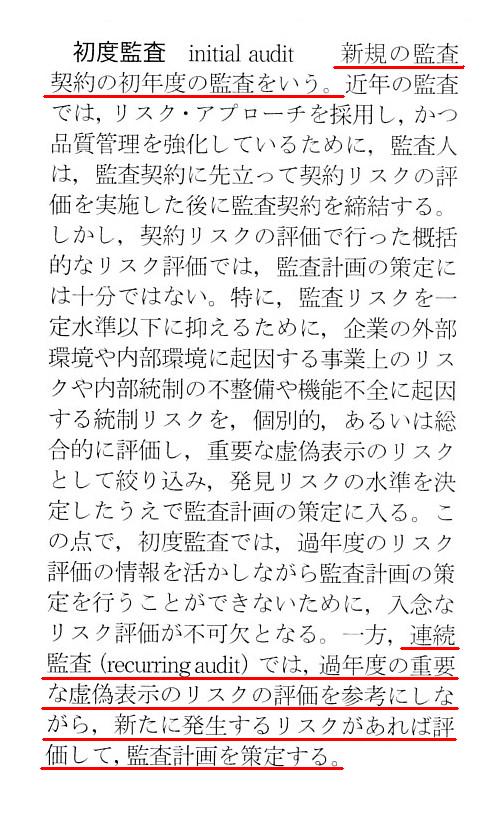

「初度監査」("Initial

Audit")

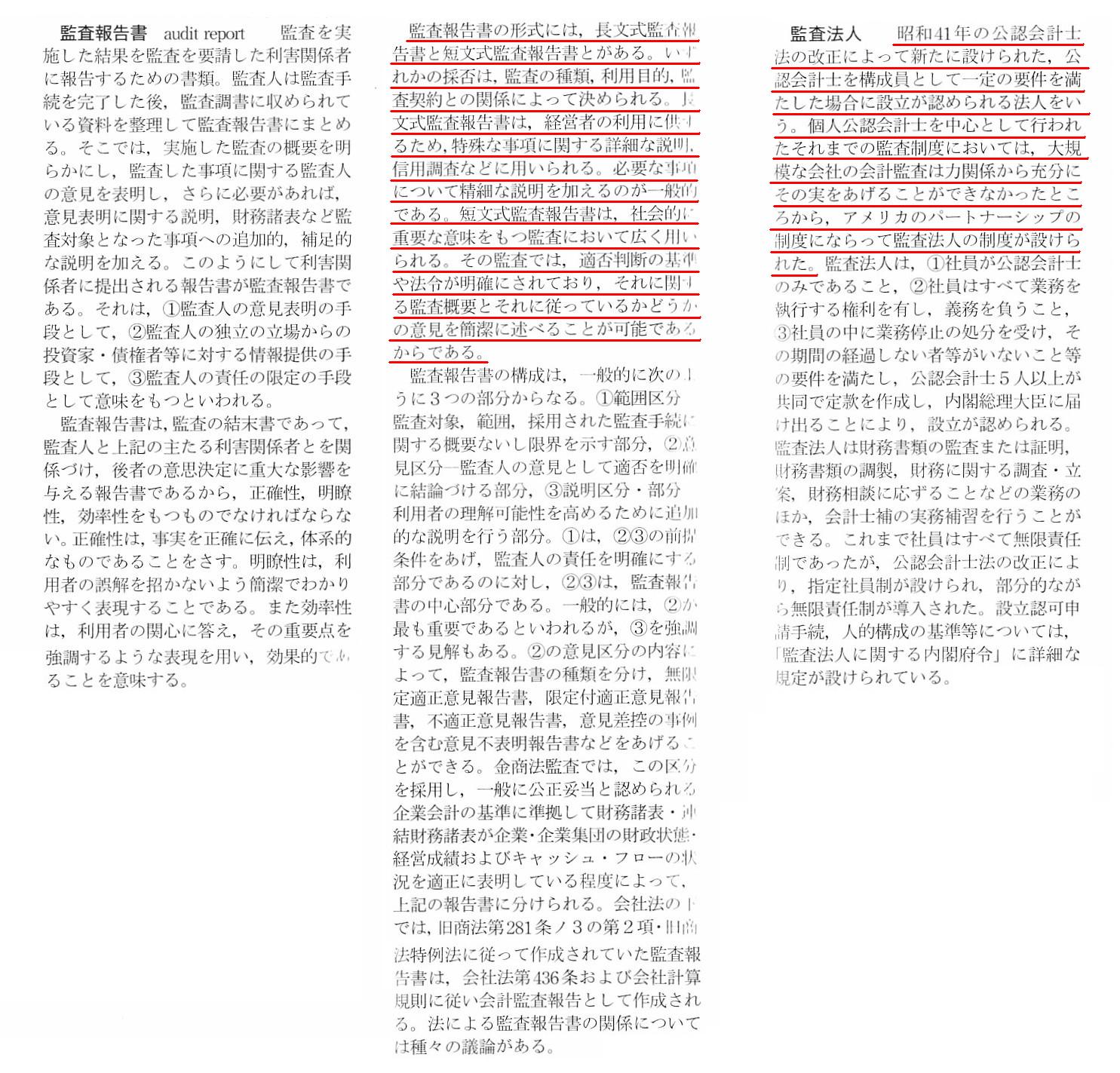

「監査報告書、監査法人」("Audit

Report"、"Audit Firm")

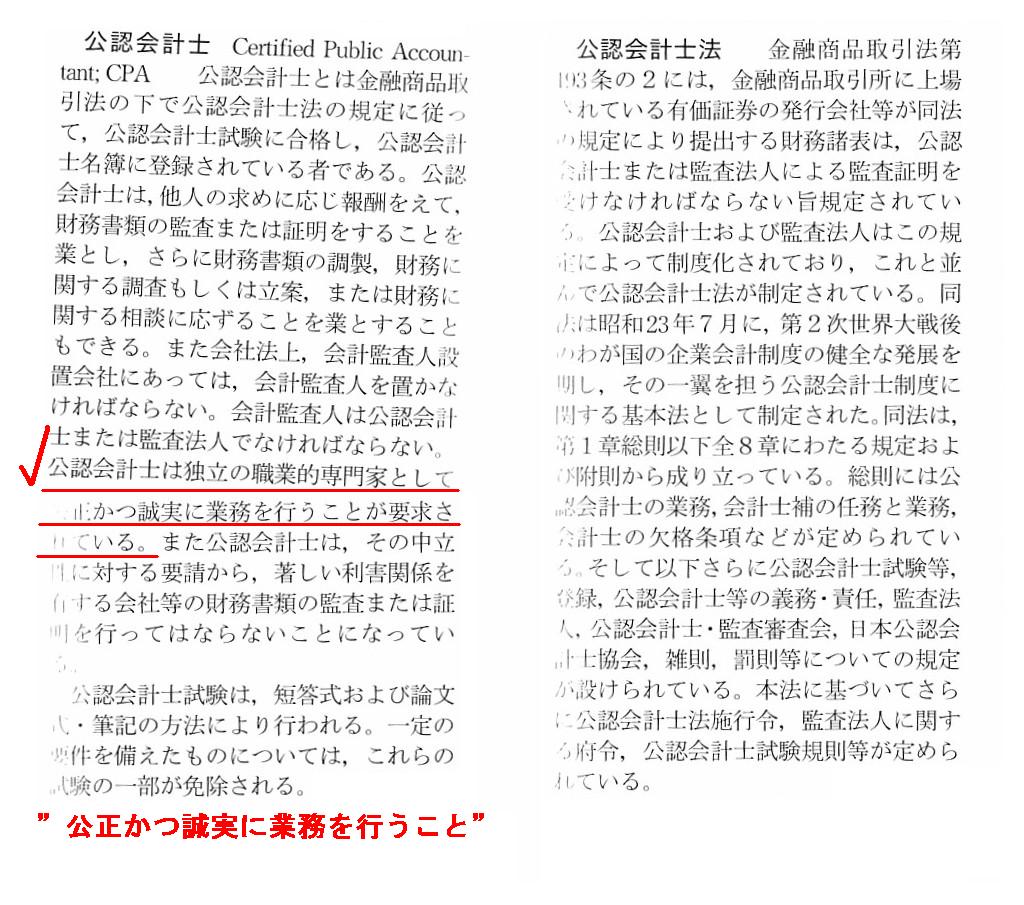

「公認会計士、公認会計士法」("Certified

Public Accountant"、"Certified Public Accountants Act")

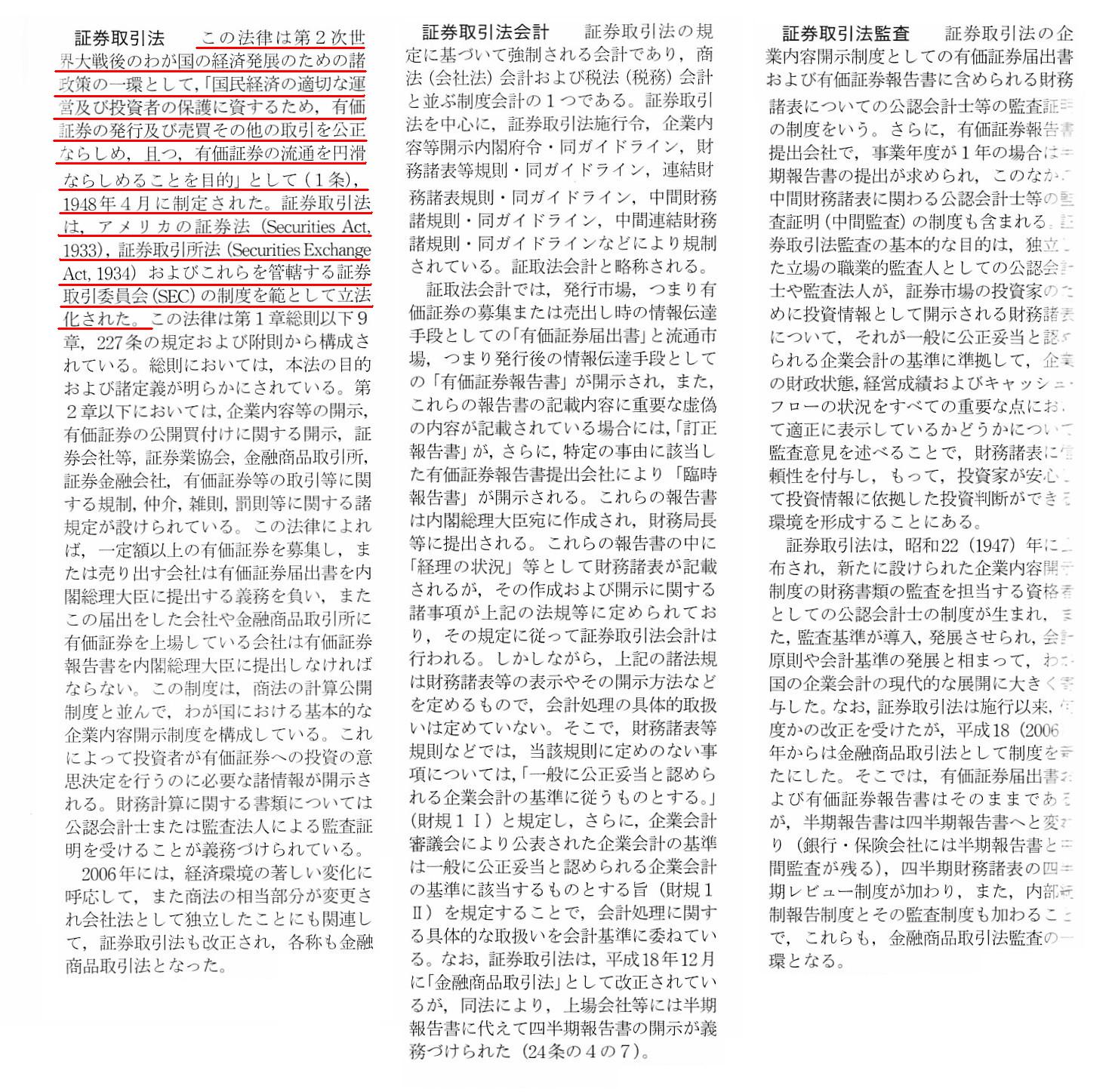

「証券取引法、証券取引法会計、証券取引法監査」("Securities

and Exchange Act"

"Accounting on the Securities and Exchange Act"、"Audit on

the Securities and Exchange Act")

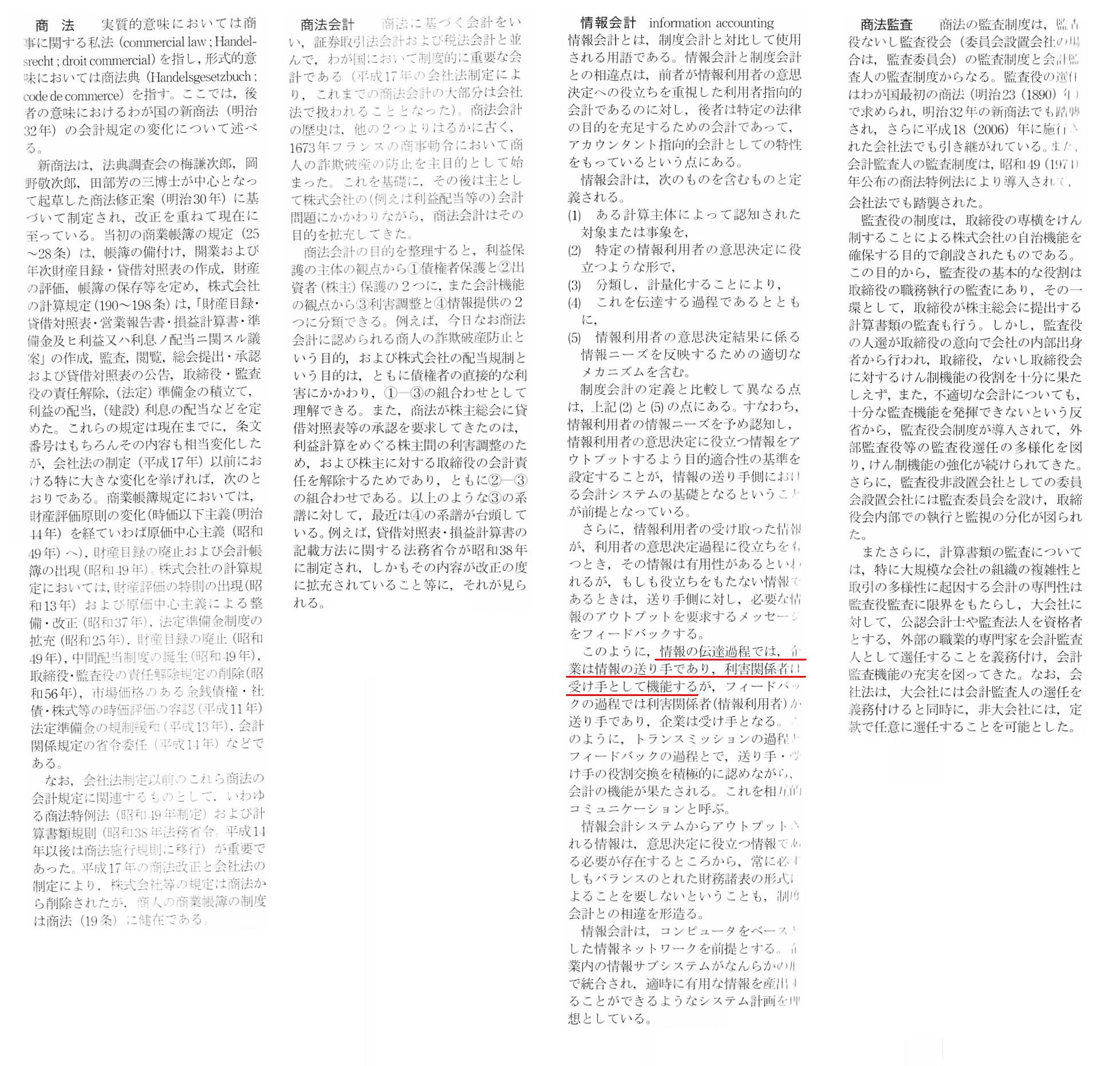

「商法、商法会計、情報会計、商法監査」("Commercial

Code"、"Accounting on the Commercial Code"、

"Information Accounting"、"Audit on

the Commercial Code")

【コメント】

Both a term "Initial Audit" and a term "Recurring Audit"

presuppose

that an acounting audit itself is commenced from halfway.

In

theory, a Certified Public Accountant never alters or never rotates.

A term

"Continuous Auditing Term" itself presupposes that an acounting audit is

commenced from halfway, actually.

In theory, a person who is engaged in an

accounting audit of a company never alters

from a foundation of the company

through a listing of a share of the company to a dissolution of the

company.

In theory, the Securities and Exchange Act has a concept "Audit" as

its basis in it,

whereas the Commercial Code doesn't have a concept "Audit"

from the beginning in it.

The Securities and Exchange Act puts the greatest

essential on disclosing contents and details of an issuer,

whereas the

Commercial Code puts the greatest essential on reporting a result of an

execution of operations.

The former makes a presentation of "what an issuer

contains inside it" and "cuts up into small pieces

(i.e. into each accounting

title)," whereas the latter merely lets shareholders of a company know

a

"result of an operation of the company" from the beginning to the end.

I

can't make a sweeping generalization about it at all, but, in my personal

opinion,

the former regards a "Balance Sheet" as comparatively vital, whereas

the latter a "Profit and Loss Statement."

「初度監査」という用語も「連続監査」という用語も、

どちらも会計監査それ自体を途中から開始することを前提としているのです。

理論上は、公認会計士が交代をするすなわちローテーションをするということは決してないのです。

「継続監査期間」という用語それ自体が、実は会計監査を途中から開始することを前提としているのです。

理論上は、会社の会計監査に従事をする人物は、その会社の設立からその会社の株式の上場を経てその会社の解散の時まで、

決して交代しないのです。

理論上は、証券取引法にはその土台として「監査」という概念があるのですが、商法には始めから「監査」という概念はないのです。

証券取引法は発行者の内容と詳細を開示することに最重点を置いているのに対し、

商法は業務の執行の結果を報告することに最重点を置いています。

証券取引法は「発行者の社内に含まれている物」を表示し「1つ1つにまで(すなわち、各勘定科目にまで)細かく切る」

ということをする一方、商法は単に会社の株主に対しその「会社の営業の結果」を告げることだけに終始します。

一概に言えることでは全くないのですが、私個人の意見になりますが、

証券取引法は「貸借対照表」を相対的に重視しているのに対し、商法は「損益計算書」を相対的に重視しているのです。

Concerning a sale of a business unit, from a viewpoint in the remote

past,

a person who is engaged in the accounting-related duties probably wants

to say,

"I can't tell whether a book value of each asset transferred from a

seller company is correct or not."

事業部門の売却に関して言いますと、大昔の観点から言えば、会計関連の職務に従事している人はきっとこう言いたいでしょう。

「売り手企業から譲渡される各資産の帳簿価額が正しいのかどうか私にはわかりません。」と。

In a word, an Accounting Auditor must traditionally not become a

transmitter of information.

一言で言いますと、伝統的に会計監査人は情報の送り手になってはならないのです。

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}