2021年3月1日(月)

「本日2021年3月1日(月)にEDINETに提出された全ての法定開示書類」

本日(すなわち、2021年3月1日)、EDINETに提出された法定開示書類は合計182冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計803日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜2020年12月31日(木))

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

各コメントの要約付きの過去のリンク その7(2021年1月1日(金)〜)

http://citizen2.nobody.jp/html/202101/PastLinksWithASummaryOfEachComment7.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

2021年2月28日(日)日本経済新聞

News Forecast

3月1日 改正会社法施行 役員報酬 決め方透明に

(記事)

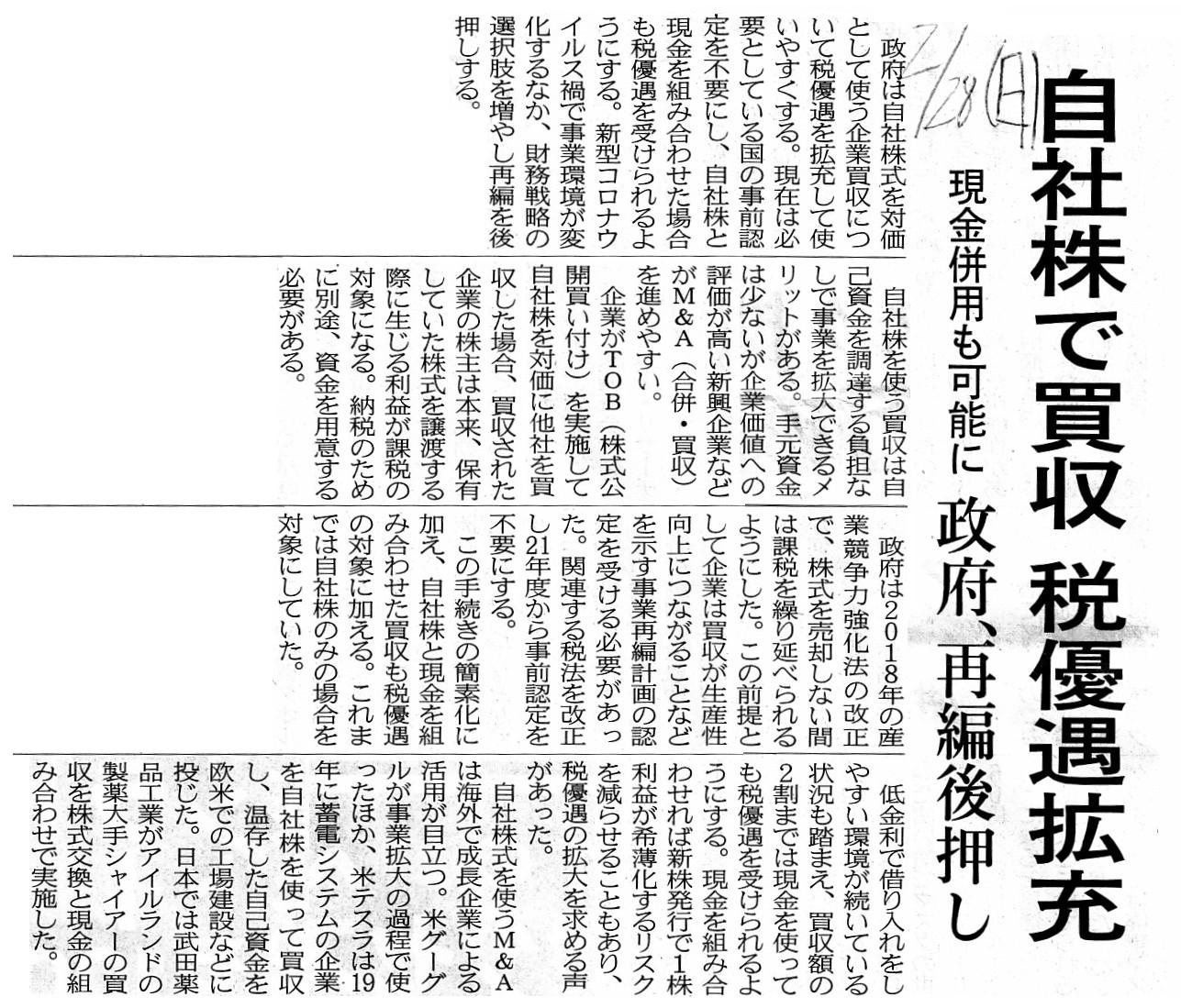

2021年2月28日(日)日本経済新聞

自社株で買収 税優遇拡充 現金併用も可能に 政府、再編後押し

(記事)

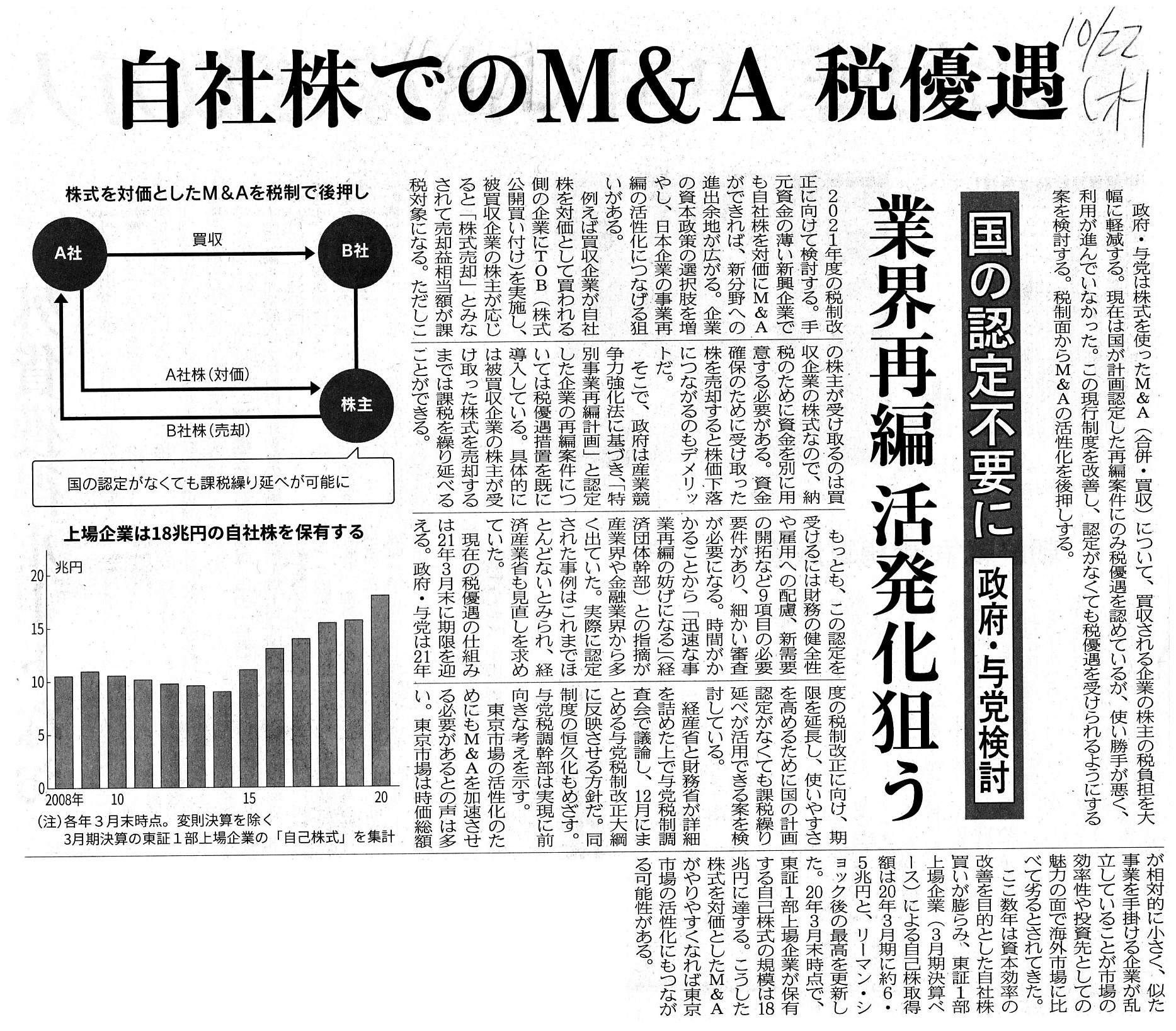

2020年10月22日(木)日本経済新聞

自社株でのM&A 税優遇 国の認定不要に 政府・与党検討 業界再編 活性化狙う

(記事)

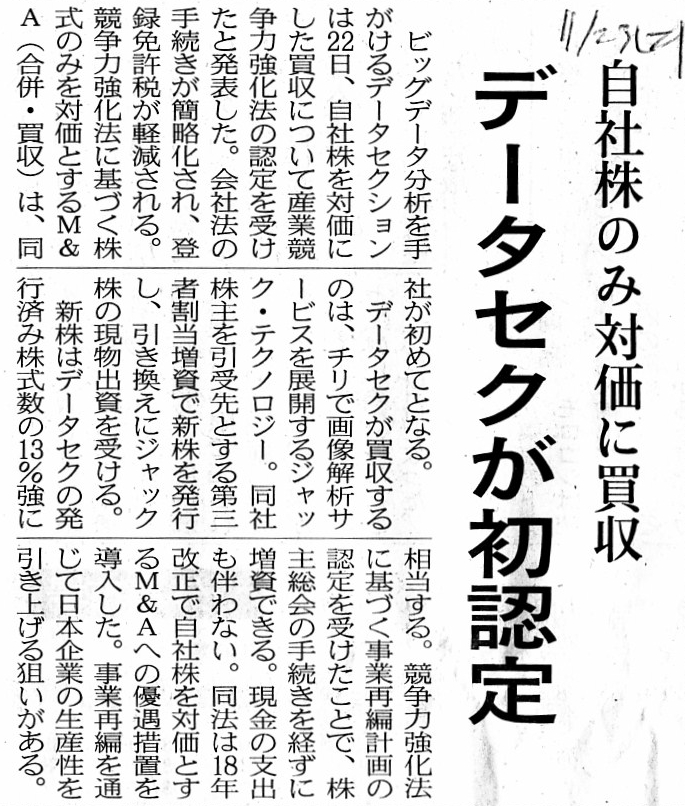

2019年11月23日(土)日本経済新聞

自社株のみ対価に買収 データセクが初認定

(記事)

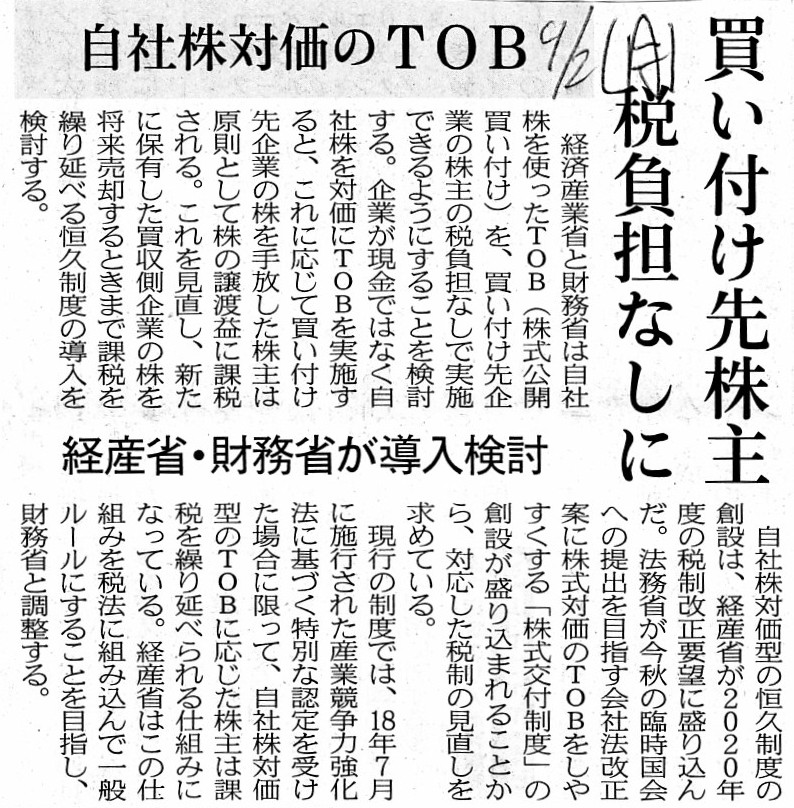

2019年9月2日(月)日本経済新聞

買い付け先株主 税負担なしに 自社株対価のTOB 経産省・財務省が導入検討

(記事)

経済産業省

2021年2月5日

「産業競争力強化法等の一部を改正する等の法律案」が閣議決定されました

ttps://www.meti.go.jp/press/2020/02/20210205001/20210205001.html

「PDF印刷・出力したファイル」

>現在開会中である、第204回通常国会に提出される予定です。

関連資料

法律案概要

ttps://www.meti.go.jp/press/2020/02/20210205001/20210205001-1.pdf

(ウェブサイト上と同じPDFファイル)

法律案要綱(ウェブサイト上と同じPDFファイル)

法律案・理由(ウェブサイト上と同じPDFファイル)

新旧対照条文(ウェブサイト上と同じPDFファイル)

参照条文(ウェブサイト上と同じPDFファイル)

現金と自社株の組み合わせをM&Aの対価として用いることができます。

しかしながら、今の上場株式は昔の上場株式ではなくなっているのです。

具体的に言いますと、1999年9月30日以前の伝統的な証券制度における上場株式というのは

実務上は実質的に「現金同等物」であったのですが、

1999年10月1日以降の現行の証券制度における上場株式は実務上は少しも「現金同等物」ではないのです。

上記の相違の理由の1つは、確かに、前者の証券制度では株式市場における株価は変動しなかった一方

後者の証券制度では株式市場における株価は大幅にかつ毎日変動するからである、というものです。

しかし、上記の相違のもう1つの理由は、別の角度からの見方になりますが、

前者の証券制度における上場株式は実務上短期間のうちに株式市場内で現金化することができた一方

後者の証券制度における上場株式は実務上短期間のうちに株式市場内で現金化することはできないからである、というものです。

それどころか、やや極端な言い方になりますが、後者の証券制度に関する理論は、

上場株式は会社の満了日にすなわち会社の清算日に現金化されるということを前提にしています。

手短に言えば、後者の証券制度における上場株式は短期間のうちに株式市場内で売却をすることができるとは限らないのです。

すなわち、M&Aの対価として自社株式を用いる場合は、対象会社の株式の売り手がM&Aの対価を真の意味で受け取ることが

できるのは会社の満了日になってからになるのです。

簡単に言えば、上記の相違の1つの理由は、株式の本源的価値の不変性ではなく、株式市場内の株式の流動性なのです。

話をまとめますと、1999年9月30日以前の伝統的な証券制度における上場株式はむしろM&Aの対価として適合するのですが、

1999年10月1日以降の現行の証券制度における上場株式は決してM&Aの対価として適合しないのです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}