2020年9月11日(金)

「本日2020年9月11日(金)にEDINETに提出された全ての法定開示書類」

Today

(i.e. September 11th, 2020), 321 legal disclosure documents have been submitted

to EDINET in total.

本日(すなわち、2020年9月11日)、EDINETに提出された法定開示書類は合計321冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計633日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜2020年8月31日(月))

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

各コメントの要約付きの過去のリンク その6(2020年9月1日(火)〜)

http://citizen2.nobody.jp/html/202009/PastLinksWithASummaryOfEachComment6.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

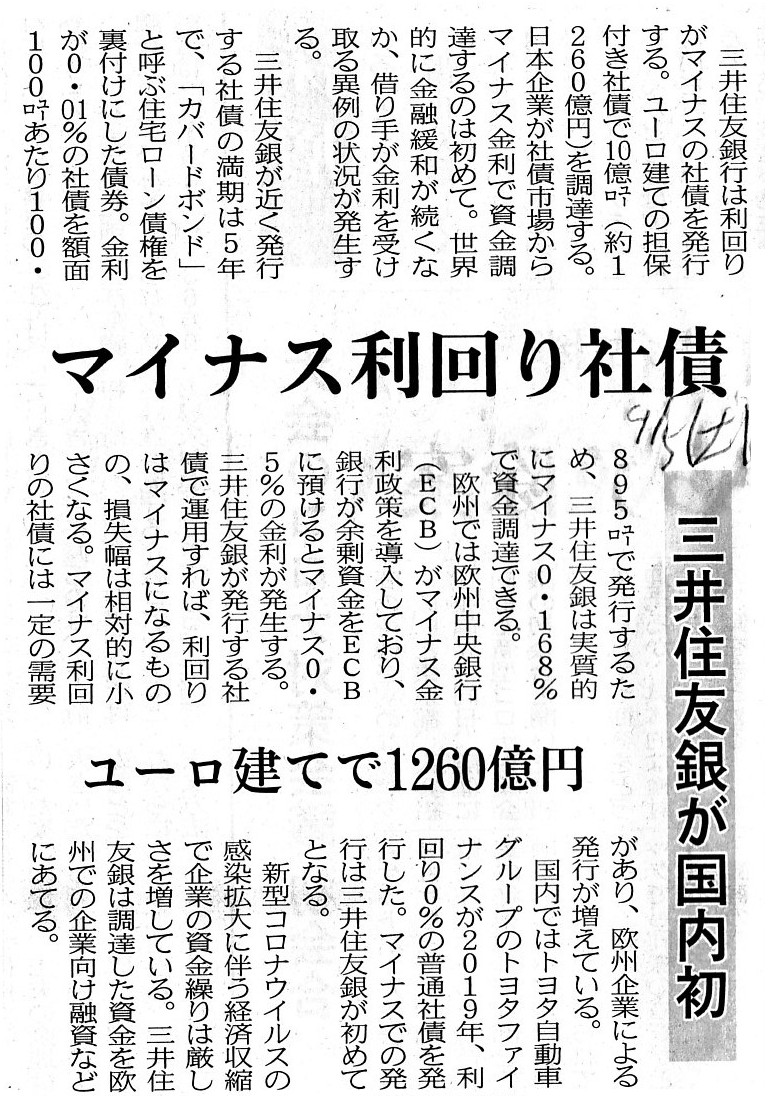

2020年9月5日(土)日本経済新聞

マイナス利回り社債 三井住友銀が国内初 ユーロ建てで1260億円

(記事)

2020年9月11日

富国生命保険相互会社

東京都住宅供給公社が発行する「ソーシャルボンド」の購入について

ttps://www.fukoku-life.co.jp/about/news/download/20200911.pdf

(ウェブサイト上と同じPDFファイル)

A negative interest rate bond can be used as one of the types of what you

call ESG investment.

But, generally, a corporation which issues a negative

interest rate bond as ESG investment securities

is not a financial service

but a business-operating organization.

For a corporation contributory to ESG

activities is not a financial service but a business-operating

organization.

That's why a financial service very seldom issues a negative

interest rate bond in practice.

All things considered, a corporation which

issues a negative interest rate bond as ESG investment securities is

only

that which is able to make a drastic "diversification"

because ESG activities

themselves are "utterly new operations" for the corporation, actually.

For

example, a Real Estate Investment Trust is not able to issue a negative interest

rate bond as ESG investment

securities in practice because it may legally not

be engaged in business activities other than asset investment.

マイナス金利の債券はいわゆるESG投資の一類型として活用することができます。

ただ、通常は、ESG投資証券としてマイナス金利の債券を発行する法人というのは、

金融機関ではなく事業を営む団体なのです。

というのは、ESG活動に関与する力がある法人は金融機関ではなく事業を営む団体だからです。

そういうわけで、実務上は金融機関がマイナス金利の債券を発行することはほとんどないのです。

あれこれ考えてみますと、実際のところESG活動それ自体がその法人にとって「全く新しい業務」であるわけなのですから、

ESG投資証券としてマイナス金利の債券を発行する法人というのは思い切った「多角化」を行うことができる法人だけなのです。

例えば、不動産投資信託は、法律上資産の運用以外の行為を営業としてすることができませんので、

実務上はESG投資証券としてマイナス金利の債券を発行することができないのです。

,321LegalDisclosureDocumentsHaveBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}