2020年8月1日(土)

「本日2020年8月1日(土)にEDINETに提出された全ての法定開示書類」

Today

(i.e. August 1st, 2020), 0 legal disclosure document has been submitted to

EDINET in total.

本日(すなわち、2020年8月1日)、EDINETに提出された法定開示書類は合計0冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計592日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜)

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

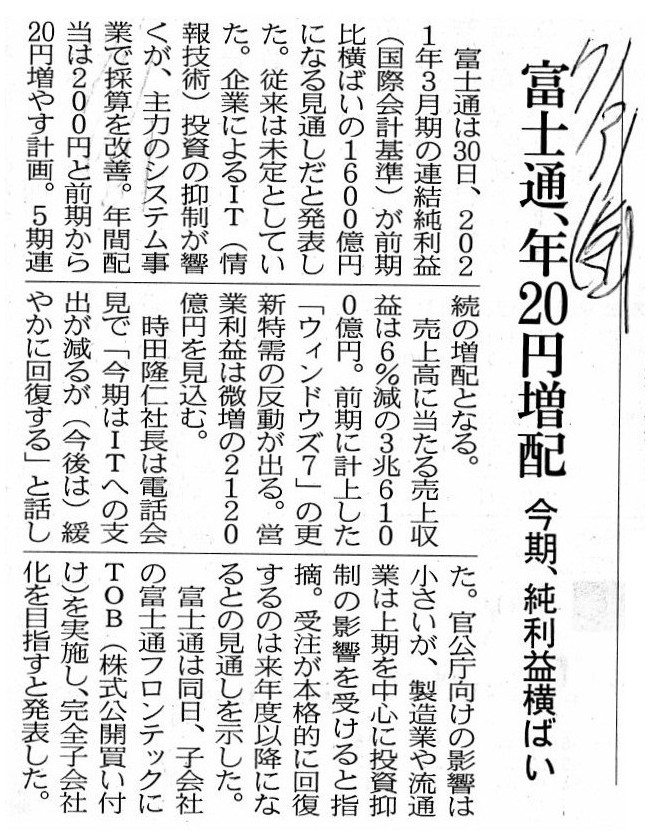

2020年7月31日(金)日本経済新聞

富士通、年20年増配 今期、純利益横ばい

(記事)

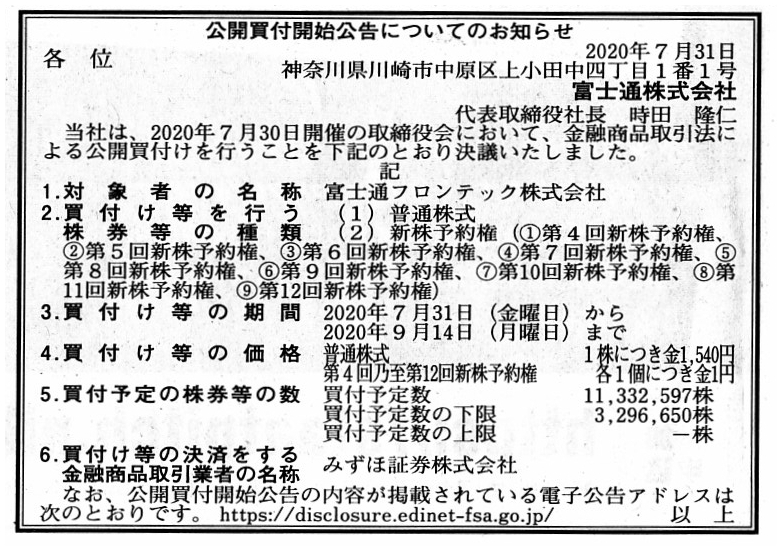

2020年7月31日(金)日本経済新聞 公告

公開買付開始公告についてのお知らせ

富士通株式会社

(記事)

R2.07.31

富士通株式会社

公開買付開始公告

(EDINET上と同じhtmlファイル)

R2.07.31 10:16

富士通株式会社

公開買付届出書 対象: 富士通フロンテック株式会社

(EDINET上と同じPDFファイル)

R2.07.31 15:44

富士通フロンテック株式会社

意見表明報告書 対象: 富士通株式会社

(EDINET上と同じPDFファイル)

2020年7月30日

富士通フロンテック株式会社

支配株主である富士通株式会社による当社株券等に対する公開買付けに関する意見表明及び応募推奨のお知らせ

ttps://www.fujitsu.com/jp/group/frontech/documents/about/resources/news/press-releases/2020/prs20200730-2.pdf

(ウェブサイト上と同じPDFファイル)

このたびの公開買付とは直接的な関係はありませんが、「上場子会社」の位置付けについて考えさせられる論点になりますが、

富士通フロンテック株式会社のウェブサイトには次のようなプレスリリースがありました↓。

2020年5月13日

富士通フロンテック株式会社

取締役人事に関するお知らせ

ttps://www.fujitsu.com/jp/group/frontech/documents/about/resources/news/press-releases/2020/prs20200513-2.pdf

(ウェブサイト上と同じPDFファイル)

2020年6月29日

富士通フロンテック株式会社

支配株主等に関する事項について

ttps://www.fujitsu.com/jp/group/frontech/documents/about/resources/news/press-releases/2020/prs20200629.pdf

(ウェブサイト上と同じPDFファイル)

What if a retired director from Fujitsu Frontec goes back to

Fujitsu?

Investors in a stock market may suspect that a parent company pulls

strings behind the scenes.

That is to say, in case an executive of a parent

company takes office as a director at a subsidiary company,

he should cut all

his connections with the parent company.

One idea is that, in case an

executive of a parent company takes office as a director

at a subsidiary

company, he should receive a retirement allowance from the parent

company,

and he should swear to investors at a stock exchange, etc., "I will

never go back to the parent company."

A concurrent service as a director both

at a parant company and at a subsidiary company is completely out of the

question.

Admitting that a parent company takes control over a

decision-making organ of a subsidiary company on a basis of

their group

management strategy and that they form a united front against competitors inside

and outside the industry,

at least a director of a subsidiary company must be

independent of a parent company

not as a member of their corporate group but

as one natural person for the sake of investors in a stock market.

At least

when a director of a subsidiary company is confronted with a stock market,

he

should be more a fiduciary for investors in a stock market than a fiduciary for

a parent company.

It is true that a parent company directs their group

management strategy to a subsidiary company

in a clear voice (via an

operation order), but a director of a subsidiary company must orient the

subsidiary company

exclusively toward the subsidiary company's own interests

for the sake of all shareholders of the subsidiary company.

All directors of

Fujitsu Frontec must say to their former higher-ups in their old Fujitsu time,

"Who are you, too?"

富士通フロンテックを退職した取締役が富士通に戻るとしたらどうでしょうか。

株式市場の投資家は、親会社が陰で糸を引いているのではないかと疑うかもしれません。

すなわち、親会社の幹部が子会社に取締役として就任する場合は、親会社との縁を全て切るべきなのです。

1つの案は、親会社の幹部が子会社に取締役として就任する場合は、親会社から退職金をもらい、

そして証券取引所等で投資家に対し「私は親会社に戻ることは決していたしません。」と宣誓をするべきなのです。

親会社と子会社両方において取締役として兼任をすることは、完全に論外なのです。

親会社は子会社の意思決定機関をグループ経営戦略に基づいて支配しており業界内外の競争相手に対して統一戦線を張っている

というのは認めますが、少なくとも子会社の取締役は株式市場の投資家のために企業グループの一員としてではなく

1人の自然人として親会社から独立していなければならないのです。

少なくとも株式市場と向かい合っている時は、子会社の取締役は親会社の受託者というよりは

株式市場の投資家の受託者であるべきなのです。

確かに、親会社は子会社に対してグループ経営戦略をはっきりとした声で(業務指図書によって)指示するわけですが、

子会社の取締役は子会社の全ての株主のために子会社を専ら子会社自身の利益に適うよう方向付けなければならないのです。

富士通フロンテックの取締役は皆、かつての富士通時代の元上司に「あなたも誰でしたっけ?」と言わなければならないのです。

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}