2020年8月8日(土)

「本日2020年8月8日(土)にEDINETに提出された全ての法定開示書類」

Today

(i.e. August 8th, 2020), 0 legal disclosure document has been submitted to

EDINET in total.

本日(すなわち、2020年8月7日)、EDINETに提出された法定開示書類は合計0冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計599日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜2020年4月30日(木))

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

各コメントの要約付きの過去のリンク その5(2020年5月1日(金)〜)

http://citizen2.nobody.jp/html/202005/PastLinksWithASummaryOfEachComment5.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

「ゼミナール 金融商品取引法」 大崎貞和 宍戸善一 著 (日本経済新聞出版社)

第6章 敵対的企業買収と防衛策

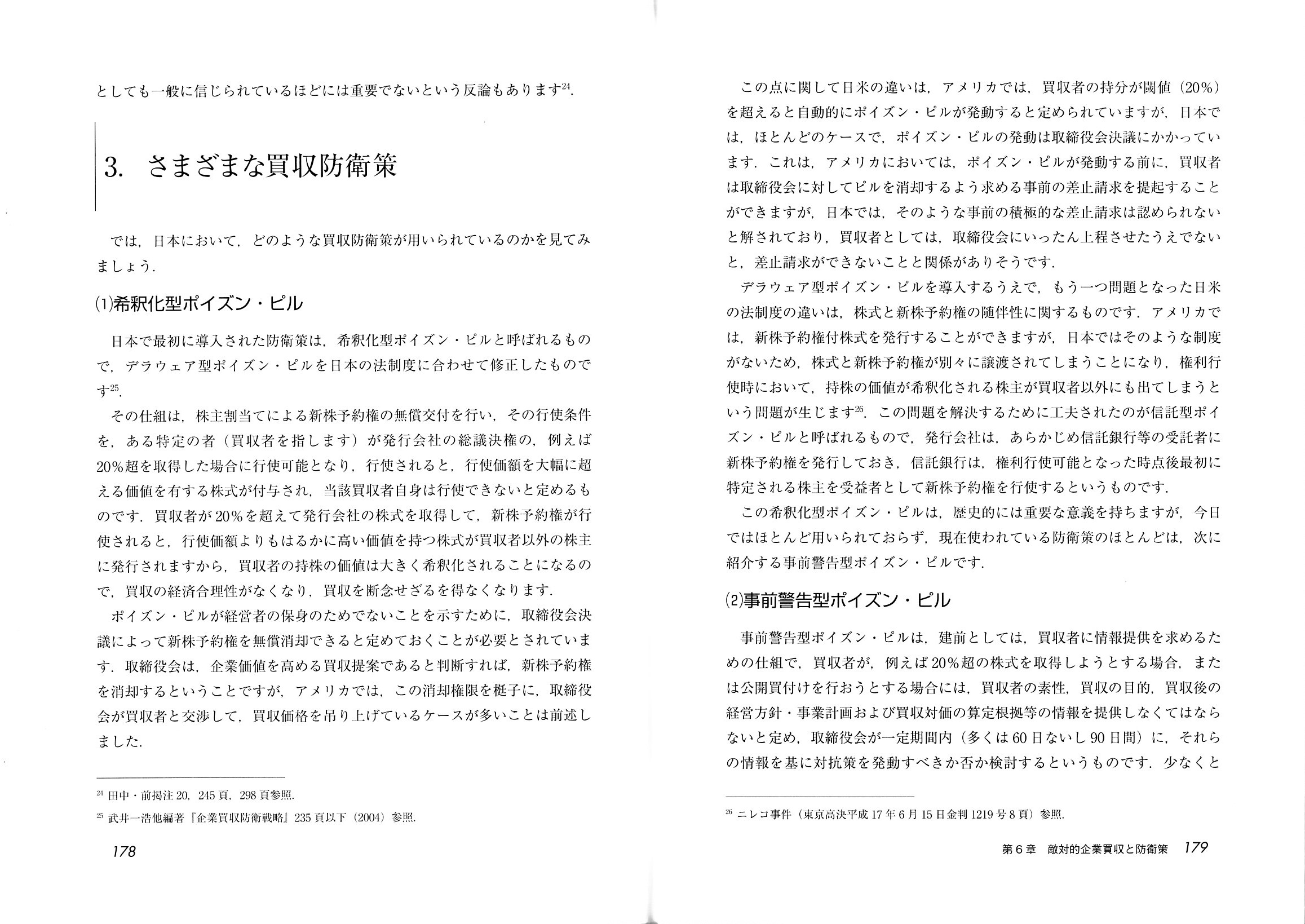

3. さまざまな買収防衛策

(1) 希釈化型ポイズン・ピル

(2)

事前警告型ポイズン・ピル

(3) 拒否権型ポイズン・ピル

「178〜179ページ」

「180〜181ページ」

【コメント】

米国企業が買収防衛策を相次いで導入しているとのことですが、記事から重要な部分を引用したいと思います。

>新型コロナの影響で株価が低迷する米国企業が敵対的買収に備える防衛策を相次ぎ導入している。

>エネルギー企業などがコロナ禍の「安値」買収への緊急避難と位置付ける。

>2020年1〜6月に52社が敵対的買収を防ぐポイズンピル(毒薬条項)を導入した。

>19年通年では16社にとどまり、わずか半年で19年の3倍超に急増した。

>企業活動が停滞して株価が極端に下がったところで買収されれば、資産を切り売りされるとの見方が広がった。

日米の会社法制度(買収防衛策導入のための根拠)の違いについては私には詳しくは分からないのですが、

「ポイズン・ピル」についての説明を金融商品取引法の教科書からスキャンして紹介しています。

教科書の説明が正しいのかどうかについても十分には分からないなと私は思いました。

今年に入り米国企業で新たに導入されている買収防衛策が特徴的なのは、従来の買収防衛策とは異なり、

「有効期限は1年間のみ」といった条件で導入されていることです。

この理由についてですが、「天変地異の影響による株価下落は一時的なものに過ぎない。」という将来見通しの他に、

「経営者の保身のために買収防衛策を導入するわけではない。」ということをアピールする狙いもあるのだろうと思いました。

買収防衛策については様々な見方があるのだろうとは思いますが、買収防衛策を導入・発動することは、

せっかく申し出があるにも関わらず「投資家から株式売却の機会を奪うことになる。」という問題点があると私は思います。

株主の立場からすると、「買収防衛策というのは形を変えた『譲渡制限』ではないのか。」、という見方もできると思います。

「株価が極端に下がっている現在、誰かに少しでも高い価格で株式を買い取ってもらった方がまだました。」、

株式市場の投資家としてはそう言いたくなる場面もあるのではないだろうかと思いました。

An anti-M&A policy itself can be against interests of investors in a

stock market.

That is to say, investors in a stock market themselves can hope

that an anti-M&A policy will not be invoked.

Investors in a stock market

have their own investment purposes in them.

It is exclusively investors in a

stock market that ought to discern

whether an offer of a M&A is a good

one or a bad one.

Now that investors in a stock market are all professional,

it is not proper and is logically not able

for a company itself to discern a

good from a bad concerning an offer of a M&A.

From a standpoint of

investors in a stock market, an offer of a M&A

in the midest of a

convulsion of nature of this time may be a chance in a million.

An

inappropriate invocation of an anti-M&A policy can amount to

the fact

that a company deprives investors in a stock market of a divest

opportunity.

In a scene of a rapid and chronic decrease in a share price in a

stock market,

investors in a stock market are inclined to seek for an

opportunity to put away their own shares.

Otherwise, "one existing

shareholder himself" probably begins to purchase a share additionally for a

purpose of

gaining "another investment profit" (for examle, selling a company

in pieces or a liquidation of a company).

For an existing shareholder, a

means of a disinvestment is not always "selling his own share only,"

actually.

No person can discern a hostile acquirer from a disinterested

acquirer from the beginning.

買収防衛策自体が株式市場の投資家の利益に反するということがあるのです。

すなわち、株式市場の投資家自身が買収防衛策が発動されないことを望むということがあるのです。

株式市場の投資家にはそれぞれの投資目的があります。

買収の申し出が良い申し出なのか悪い申し出なのかを見分けるべきなのは、専ら株式市場の投資家なのです。

今や株式市場の投資家は皆プロフェッショナルなのですから、会社自身が買収の申し出に関して良い悪いを識別するというのは、

ふさわしくはないことですし論理的には不可能なことなのです。

株式市場の投資家の立場からすると、今般の天変地異の最中における買収の申し出は、千載一遇のチャンスかもしれないわけです。

買収防衛策の場違いな発動は、結局のところ会社が株式市場の投資家から売却機会を奪うことにつながり得るのです。

株式市場における株価が急激にかつ慢性的に下落している場面では、

株式市場の投資家は所有株式を手仕舞う機会を探し求める傾向にあるのです。

さもなくば、「既存のある株主自身」が「異なる投資利益」を得るために

(例えば、会社を切り売りするためにまたは会社を清算をするために)きっと株式を買い増し始めることでしょう。

既存株主にとって、投資を引き上げる手段は実は「所有株式を売却することだけだ」とは限らないのです。

敵対的な買収者と公平無私な買収者とを識別することは始めから誰にもできないのです。

Generally, a listed subsidiary company doesn't introduce an anti-M&A

policy into it

because it has already had its controlling shareholder (i.e.

its parent company), but,

what if a listed subsidiary company prohibits its

parent company from selling shares of it

by means of an anti-M&A policy

or something (Doesn't it mean a "Share with a Restriction on a Transfer"?)?

一般に、既に支配株主(すなわち、親会社)がいるため上場子会社には買収防衛策が導入されていませんが、

買収防衛策か何かを用いて上場子会社が親会社が自社株式を売却することを禁止するとしたらどうでしょうか

(それは「譲渡制限株式」を意味しないでしょうか?)?

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}