2020年3月8日(日)

「本日2020年3月8日(日)にEDINETに提出された全ての法定開示書類」

Today (i.e. March 8th, 2020), 0 legal disclosure document has been

submitted to EDINET in total.

本日(すなわち、2020年3月8日)、EDINETに提出された法定開示書類は合計0冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計446日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)〜2019年12月31日(火))

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

各コメントの要約付きの過去のリンク その4(2020年1月1日(水)〜)

http://citizen2.nobody.jp/html/202001/PastLinksWithASummaryOfEachComment4.html

ユニゾホールディングス株式会社の被雇用者が行う「エンプロイー・バイアウト("Employee Buyout")」に関連するコメント

http://citizen2.nobody.jp/html/202001/CommentsWithRelationToAn'EmployeeBuyout'.html

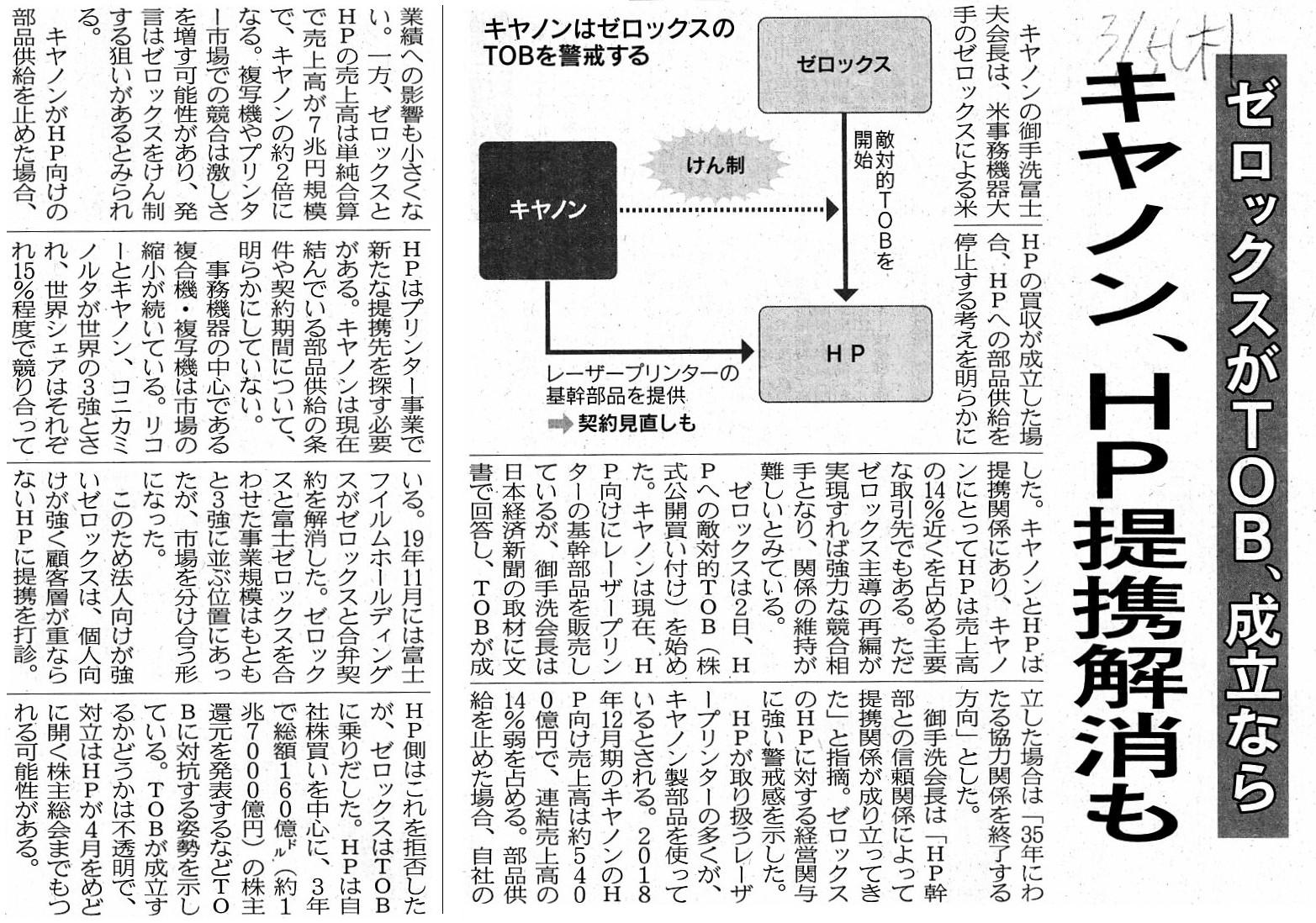

2020年3月5日(木)日本経済新聞

キャノン、HP提携解消も ゼロックスがTOB、成立なら

(記事)

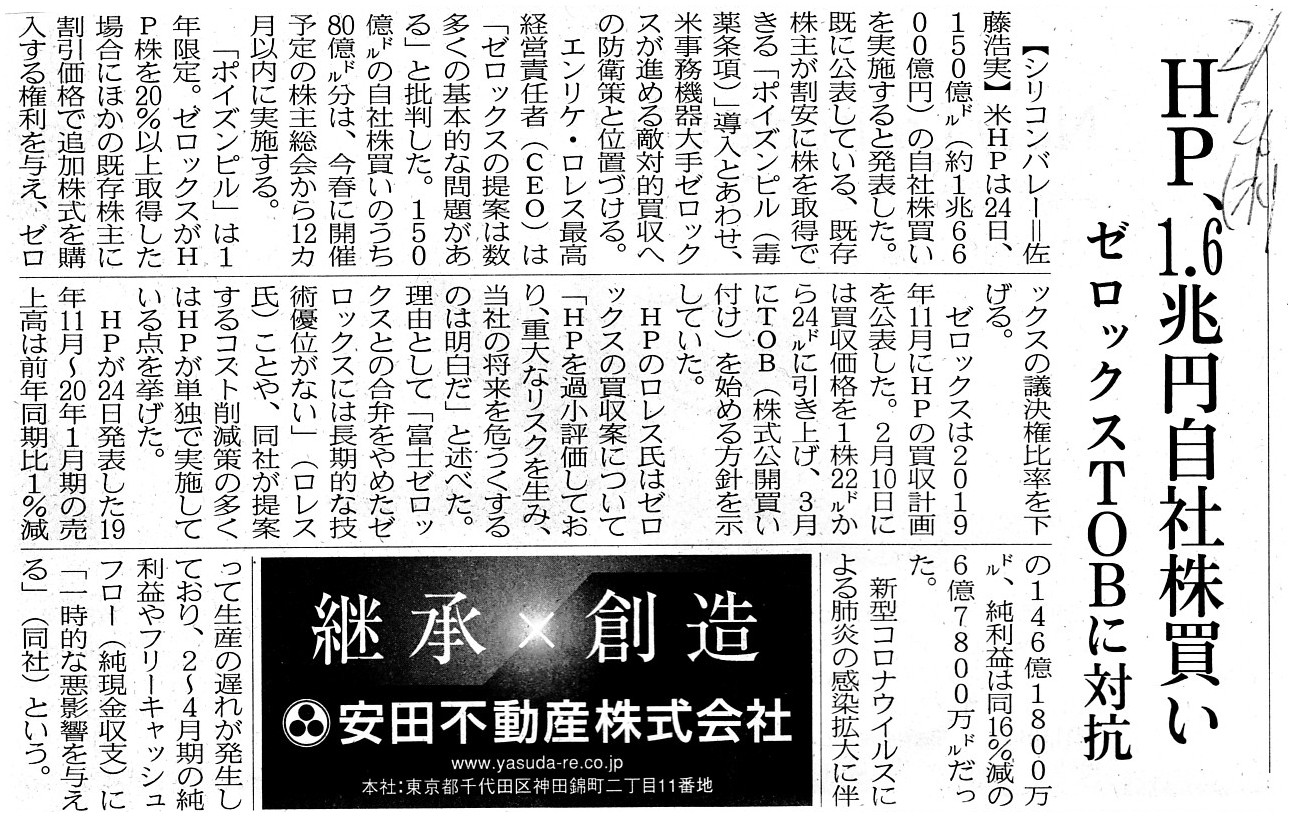

2020年2月26日(水)日本経済新聞

HP、1.6兆円自社株買い ゼロックスTOBに対抗

(記事)

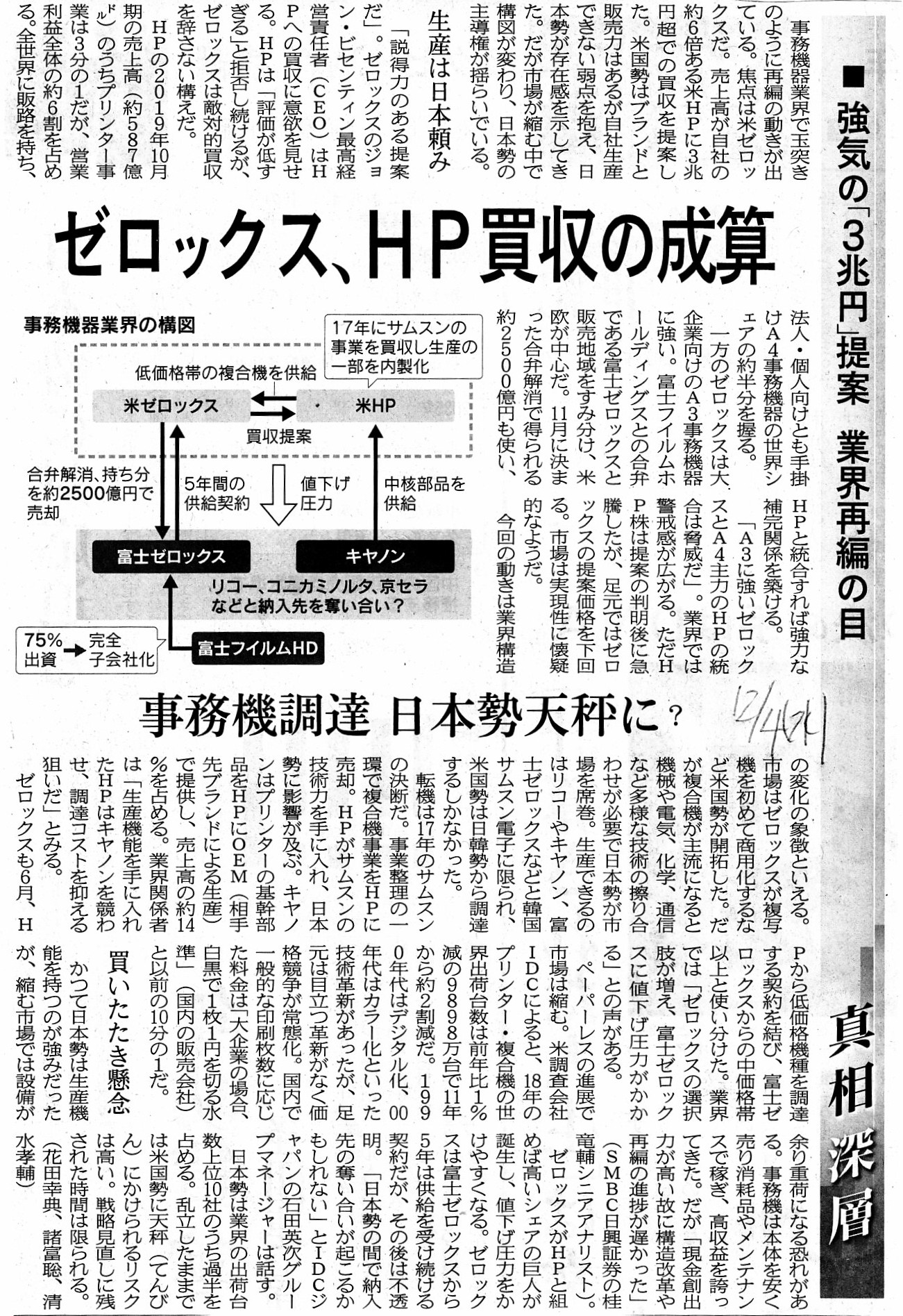

2019年12月4日(水)日本経済新聞

■強気の「3兆円」提案 業界再編の目 ゼロックス、HP買収の成算 事務機調達 日本勢天秤に?

(記事)

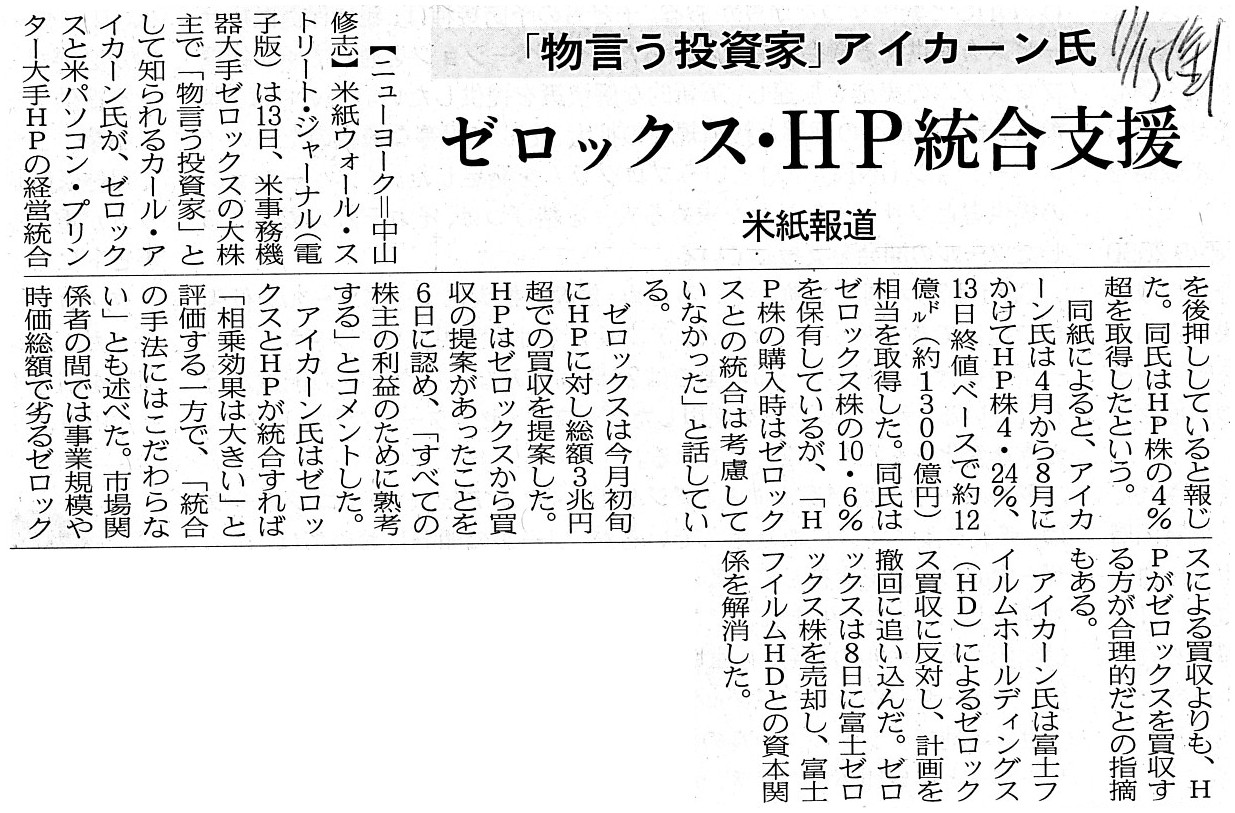

2019年11月15日(金)日本経済新聞

「物言う投資家」アイカーン氏 ゼロックス・HP統合支援 米紙報道

(記事)

2019年11月8日(金)日本経済新聞

米ゼロックス、規模に活路 HPに買収提案 3兆円規模 縮む市場

戸惑う投資家

日本勢、戦略変更も キャノン、HPに長年供給

(記事)

Please note that a discussion (concerning a term "buyout") below presupposes

a "listed company" and a "securities system."

What you call a "hostile

buyout" is on an extended line of a usual share investment in the

market,

whereas what you call a "friendly buyout" is an utterly different

transaction from a share investment in the market.

A person who makes what

you call a "hostile buyout" is one of the investors in the market,

whereas a

person who makes what you call a "friendly buyout" is never a mere investor in

the market

but purely a potential manager who has "already had a thorough

knowledge" of a subject company more or less.

A person who makes what you

call a "hostile buyout" will buy a share of a subject company purely as a listed

share,

whereas a person who makes what you call a "friendly buyout" will buy

a share of a subject company

as if the share were a unlisted share of course

though the share is actually a listed share.

To put it abstractly, what you

call a "hostile buyout" is one of the listed share investments in the

market,

whereas, contrary to what you might think, what you call a "friendly

buyout" is

one of the securities investments in general.

A person who

invests in a listed share never asks to a potential investee, "How is your

company?"

On the other hand, a person who invests in an unlisted share,

including a person who makes what you call

a "friendly buyout" in today's

discussion, absolutely asks to a potential investee,

"Please let me be quite

at home with your company beforehand because we are to form one family."

I

would like to arrive at a conclusion on a basis of the discussion above.

The

conslusion is "in case of what you call a 'friendly buyout,' quite contrary to a

listed share investment in general,

directors of a subject company are not

liable for damages to a buyer in relation to an acquisition."

Quite contrary

to what you might think, though people in general are probably imagining

so,

an investment in a listed share is extremely exceptional among securities

investments in the whole world, actually.

An investment in a listed share is

made only on a ground of a document.

以下の議論(「買収」という用語に関して)は「上場企業」や「証券制度」を前提にしていることに注意して下さい。

いわゆる「敵対的買収」というのは市場における通常の株式投資の延長線上にあるものなのですが、

いわゆる「友好的買収」というのは市場における株式投資とは全くもって異なる取引なのです。

いわゆる「敵対的買収」を行う人というのは市場の投資家の1人なのですが、

いわゆる「友好的買収」を行う人というのは、市場の一投資家というわけでは決してなく、

純粋に大なり小なり対象会社のことを「既に熟知している」将来の経営者なのです。

いわゆる「敵対的買収」を行う人は対象会社の株式を純粋に上場株式として買うことになるわけですが、

いわゆる「友好的買収」を行う人は対象会社の株式を、もちろんその株式は実際には上場株式なのですが、

あたかもその株式は非上場株式であるかのように買うことになります。

抽象的に言えば、いわゆる「敵対的買収」というのは市場における上場株式投資の1つなのですが、

意外に思うかもしれませんが、いわゆる「友好的買収」というのは証券投資全般の1つなのです。

上場株式に投資をする人は、投資をする可能性がある会社に対し「御社はどんな会社ですか?」とは決して尋ねません。

一方、非上場株式に投資をする人―今日の議論ではいわゆる「友好的買収」を行う人を含むわけですが―は、

「1つの家族になるのですから御社について前もって熟知させて下さい。」と必ず投資をする可能性がある会社に対し依頼をします。

上記の議論を踏まえた上で、ある結論に辿り着きたいと思います。

その結論とは、「いわゆる『友好的買収』の場合には、上場株式投資全般とは正反対に、

株式取得に関連し対象会社の取締役は買い手に対し損害賠償の責任を負わない。」というものです。

意外に思うかもしれませんが、世間一般の人々はきっとそういうイメージを持っているのかもしれませんが、

上場株式への投資というのは、実は、世の中全体における証券投資の中では極めて例外的なのです。

上場株式への投資というのは、文書のみを根拠に行われるのです。

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}