2019年11月13日(水)

「本日2019年11月13日(水)にEDINETに提出された全ての法定開示書類」

Today (i.e. November 13th, 2019), 1435 legal disclosure documents have been submitted to EDINET in total.

本日(すなわち、2019年11月13日)、EDINETに提出された法定開示書類は合計1435冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計330日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)~2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)~2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)~)

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

「ゼミナール 会社法入門」 岸田雅雄 著 (日本経済新聞出版社)

第4章 コーポレート・ファイナンス

Ⅱ 制度を考える

2 金融商品取引法

発行市場における規制

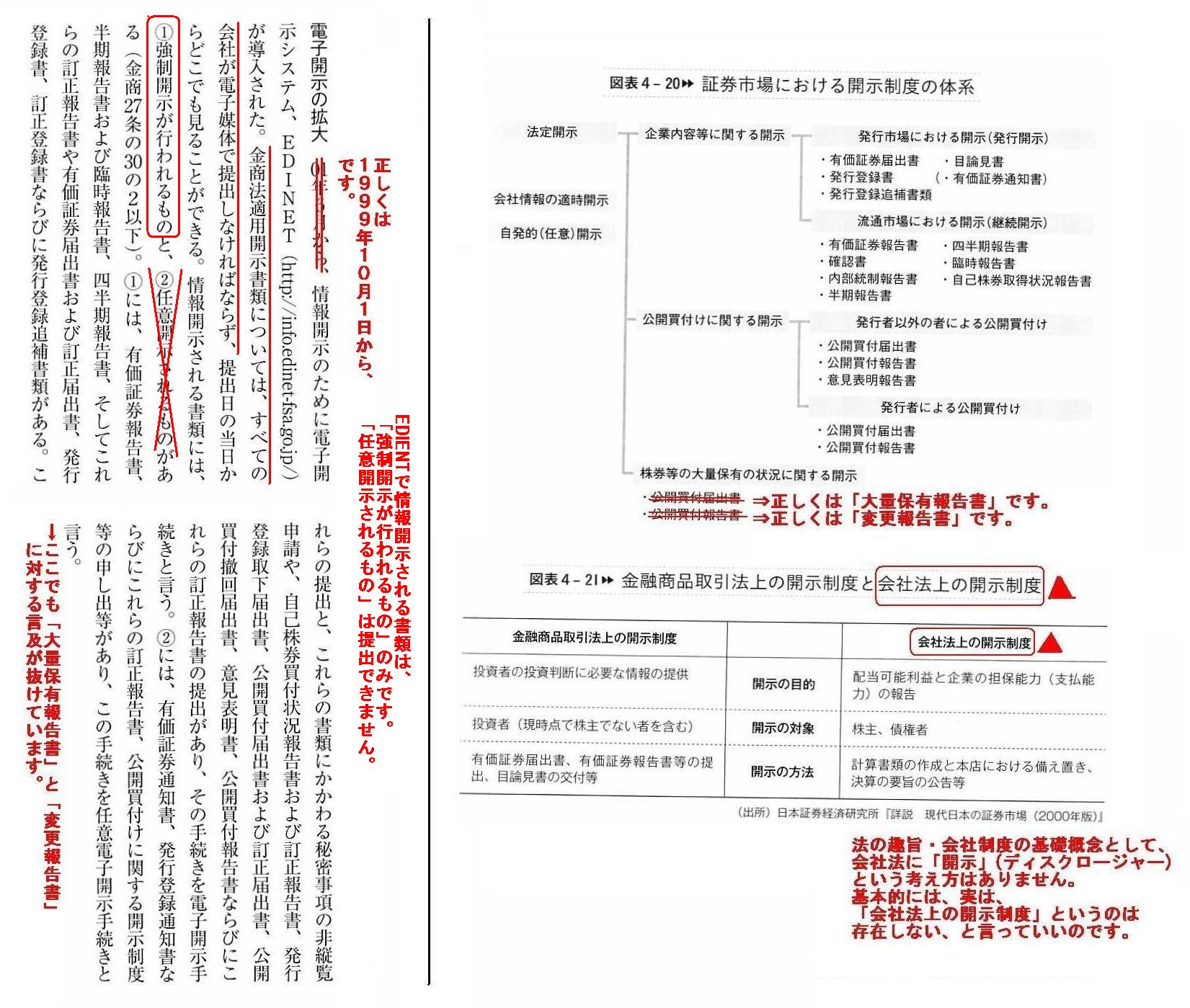

図表4-20▼証券市場における開示制度の体系

図表4-21▼金融商品取引法上の開示制度と会社法上の開示制度

「390~391ページ」

第1章 会社とは何か

Ⅱ 制度を考える

5 会社法の開示制度(ディスクロージャー)

電子公告制度度

「85~86ページ」

情報開示のために電子開示システム、EDINETが導入されたのは、01年6月からではなく「1999年10月1日」からです。

EDIENTで情報開示される書類は、「強制開示が行われるもの」のみです。

「任意開示されるもの」は提出できません。

法の趣旨・会社制度の基礎概念として、会社法に「開示」(ディスクロージャー)という考え方はありません。

基本的には、実は、「会社法上の開示制度」というのは存在しない、と言っていいのです。

→ここでも「大量保有報告書」と「変更報告書」に対する言及が抜けています。

仮に証券制度が投資家はインターネットを利用するということを前提とするのならば、

上場企業もまたインターネットを利用するということを証券制度は前提とするべきなのです。

But, at the same time, investors must be able to retrieve disclosed

information without going wrong.

So, one idea is that a listed company makes

a voluntary disclosure only on the TDnet.

That is to say, even if a listed

company make a voluntary disclosure on a web site of its own,

it is regarded

as not having made the disclosure on a securities system.

しかし、同時に、投資家は開示された情報を迷うことなく入手できなければなりません。

そこで、1つの案は、上場企業はTDnet上でのみ任意開示を行う、というものです。

すなわち、たとえ上場企業が自社ウェブサイト上で任意開示を行っても、

証券制度上はその上場企業はその開示は行っていないものとみなされる、というものです。

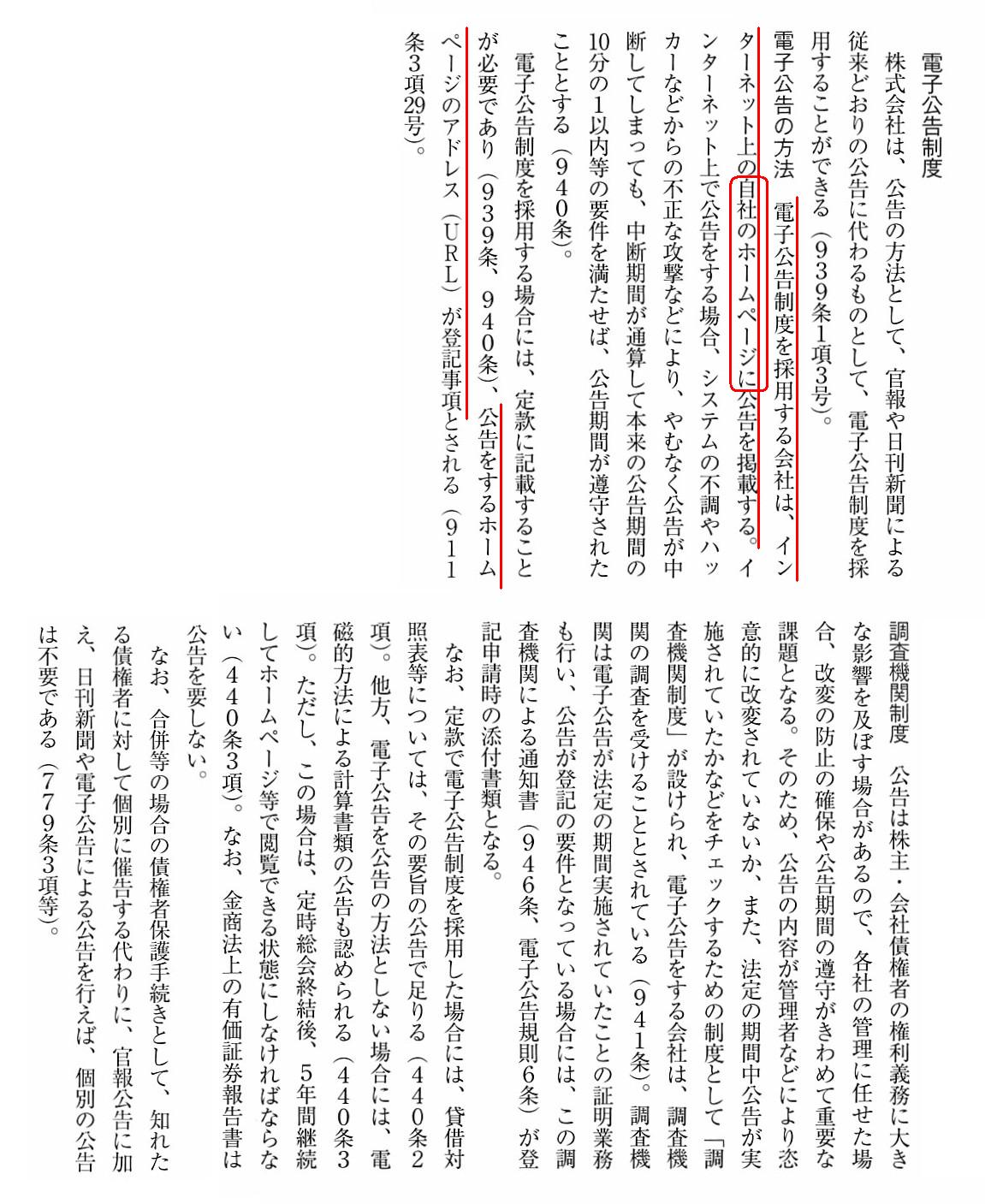

On the Companies Act, concerning an "electronic public notice,"

a

company must make an "electronic public notice" on its own web site.

And,

quite contrary to the Companies Act, on the Financial Instruments and Exchange

Act,

concerning an "electronic public notice," an issuer must make an

"electronic public notice" on the EDINET.

When I reflect on the difference

between them, on the legal system,

the EDINET presupposes that it is

absolutely available (i.e. always (24 hours / 365 days) accessible),

whereas

a web site of an issuer's own presupposes that it is available at a probability

of more than 90 percent.

To coin a phrase, an investor protection in relation

to a disclosure on the Internet requires

the "CIA" meaning

"Communicativeness," "Instantaneousness" and "Accessibleness."

Relatively

speaking, an "electronic public notice" on the Companies Act doesn't

require

the "CIA" meaning "Comparability," "Interactivity" and "Agility,"

which is also a word of my own coining.

会社法上は、「電子公告」に関しては、会社は「電子公告」を自社ウェブサイト上で行わなければなりません。

そして、会社法とは正反対に、金融商品取引法上は、「電子公告」に関しては、

発行者は「電子公告」をEDINET上で行わなければなりません。

両者の違いについて考えてみますと、法制度上は、

EDINETは絶対的に利用可能である(すなわち、常に(24時間365日)アクセスできる)ということを前提としているのに対し、

発行者自身のウェブサイトは90パーセント以上の確率で利用可能であるということを前提としているのです。

私の独創的な言い方をすれば、インターネット上の情報開示に関する投資家保護のためには、

「情報を十分に伝達するものであること」、「提出され次第即時に閲覧できること」そして「常にアクセス可能であること」

を意味する「CIA」が必要となるのです。

どちらかと言えば、会社法上の「電子公告」は、「比較可能性」、「相互作用性」そして「迅速性」を意味する「CIA」

は必要としていないのです(この「CIA」も私の造語ですが)。

,1435LegalDisclosureDocumentsHaveBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}