2019年9月8日(日)

「本日2019年9月8日(日)にEDINETに提出された全ての法定開示書類」

Today (i.e. September 8th, 2019), 0 legal disclosure document has been

submitted to EDINET in total.

本日(すなわち、2019年9月8日)、EDINETに提出された法定開示書類は合計0冊でした。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計264日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)~2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)~2019年8月31日(土))

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

各コメントの要約付きの過去のリンク その3(2019年9月1日(日)~)

http://citizen2.nobody.jp/html/201909/PastLinksWithASummaryOfEachComment3.html

2019年9月7日(土)日本経済新聞

企業業績 予想下げ 19年度 大手証券3社 世界経済減速映す

主要248社19年度

営業減益が拡大 QUICK業績予想

(記事)

2019年9月6日(金)日本経済新聞

社債 きょう1.2兆円超 発行最大、低金利が後押し

(記事)

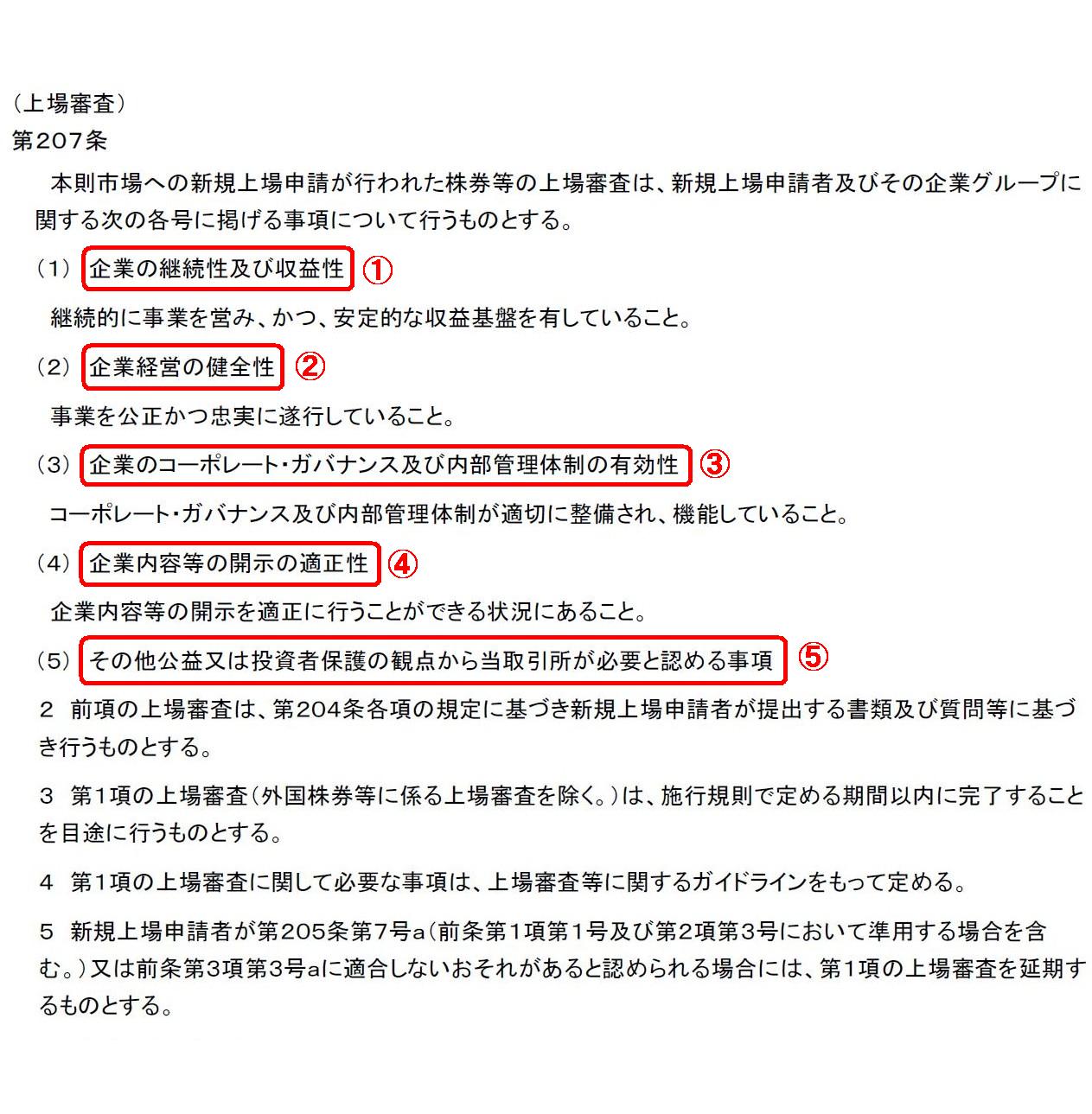

有価証券上場規程(東京証券取引所)(公表日平成30年2月28日、施行日平成30年3月31日)

第207条(上場審査)

「条文のキャプチャー」

Some securities companies have made an expectation of future financial

results

on grounds of insider information of an issuer, actually.

発行者の内部情報を根拠にして将来の業績予想を行ったことがある証券会社が実はあるのです。

第2章 上場制度と発行開示

2. 取引所の上場制度

(1) 上場基準と上場審査

上場審査

「65~66ページ」

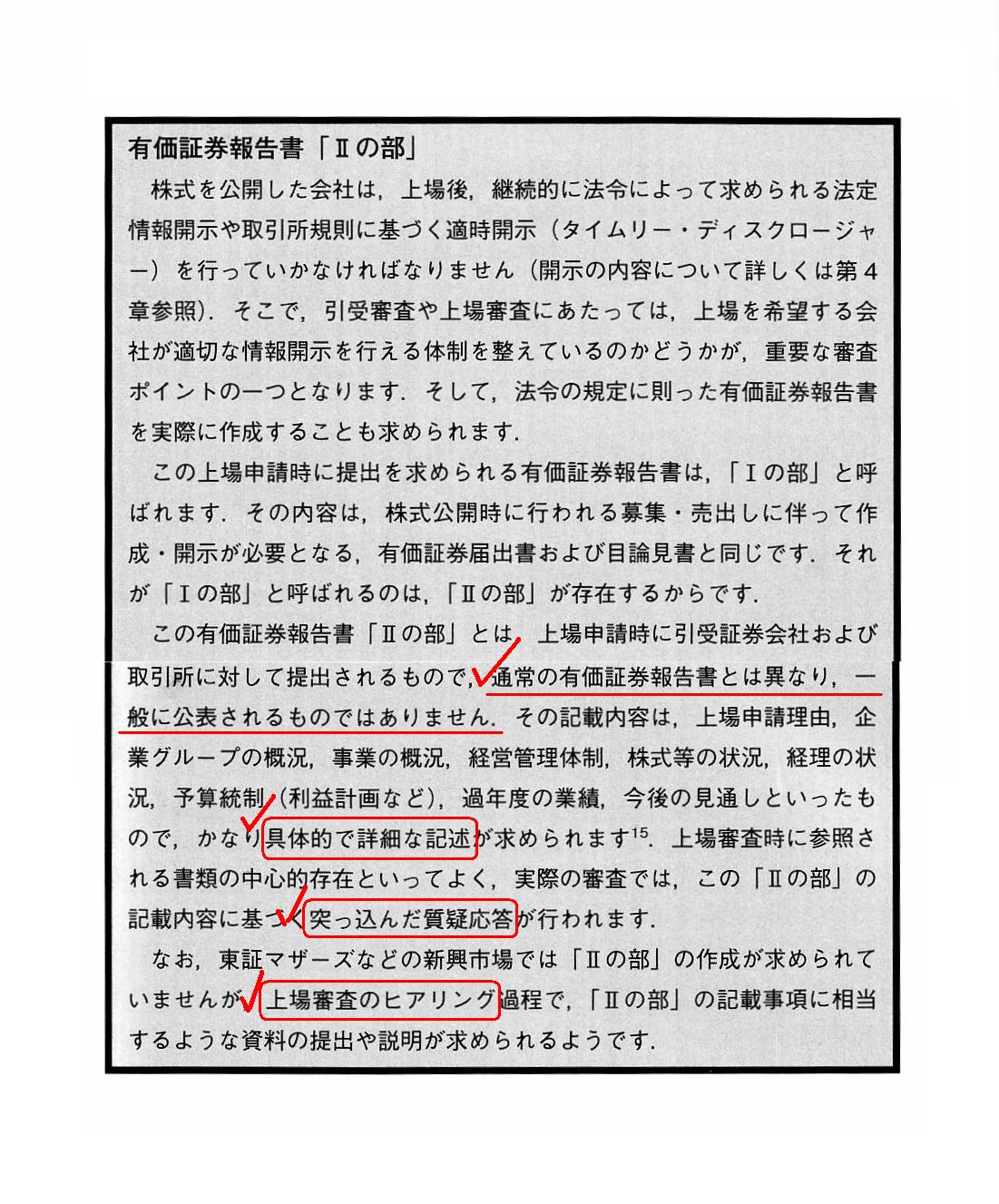

【コラム】有価証券報告書「Ⅱの部」

「66~67ページ」

「各時期の『上場審査』の主体と主目的と特徴について」

「PDFファイル」

「キャプチャー画像」

「(1999年10月以前の伝統的な証券制度において主幹事証券会社が新規上場に際し開示をするべき算定資料の例)」

「PDFファイル」

「キャプチャー画像」

主幹事証券会社が新規上場予定の発行者の株式の本源的価値を算定するためには、

主幹事証券会社は多くのインサイダー情報を知っていなければなりません。

Detailed contents of a "listing examination" are varied on the basis of a securities system of each time.

「上場審査」の具体的内容は、各時代の証券制度に基づいて変わるのです。

Each of the four periods has its own way of making a listing examination.

上場審査のやり方は時代により四者四様なのです。

Each of the four periods is different from the other three in a listing examination.

上場審査はその時代により四者四様である。

The "listing examination" on the traditional securities system before

October, 1999 was

exactly a "calculation of an intrinsic value of a share of

an issuer to be newly listed."

1999年10月以前の伝統的な証券制度における「上場審査」は、

まさに「新規上場予定の発行者の株式の本源的価値を算定すること」だったのです。

Purely in theory, a managing securities company for an underwriting

should

have disclosed its grounds for a calculation of an intrinsic value of a

share.

純粋な理論上のことになりますが、主幹事証券会社は株式の本源的価値の算定根拠を開示するべきだったのです。

A managing securities company for an underwriting used to calculate an

intrinsic value of a share

on grounds of literally insider information itself

of an issuer to be newly listed

on the traditional securities system before

October, 1999.

But, it doesn't so on the current securities system.

1999年10月以前の伝統的な証券制度では、主幹事証券会社は、新規上場予定の発行者の

文字通りインサイダー情報そのものを根拠にして株式の本源的価値を算定していました。

しかし、現行の証券制度では、主幹事証券会社はそうはしていません。

You may really get astounded, but, on the traditional securities system

before October, 1999,

a managing securities company for an underwrting used

to calculate an intrinsic value of a share

not on grounds of financial

statements of an issuer of the past 5 business years

but on grounds of a lot

of insider information of an issuer, actually.

本当にびっくり仰天するかもしれませんが、1999年10月以前の伝統的な証券制度では、主幹事証券会社は、

発行者の過去5ヵ年の財務諸表を根拠に株式の本源的価値を算定していたのではなく、

発行者の数多くの内部情報を根拠に株式の本源的価値を算定していたのです。

The reason why an intrinsic value of a share calculated by a managing

securities company for an underwriting

on the traditional securities system

before October, 1999 was trustworthy not only in theory but also in

practice

is that it calculated an intrinsic value of a share on grounds of a

lot of insider information of an issuer.

1999年10月以前の伝統的な証券制度において、

主幹事証券会社が算定する株式の本源的価値を理論上も実務上も信頼することができた理由は、

主幹事証券会社が発行者の数多くの内部情報を根拠に株式の本源的価値を算定していたからなのです。

The well-known textbook on the securities system in Japan written in 1989 and

written in plain words,

which I have read in 1990, must be revised.

私は1990年に読んだことがあるのですが、1989年に執筆され分かりやすく書かれたあの有名な日本の証券制度に関する教科書を

訂正しなければならないでしょう。

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}