2019年8月31日(土)

「本日2019年8月31日(土)にEDINETに提出された全ての法定開示書類」

Today (i.e. August 31st, 2019), 0 legal disclosure document has been

submitted to EDINET in total.

本日(すなわち、2019年8月31日)、EDINETに提出された法定開示書類は合計0冊でした。

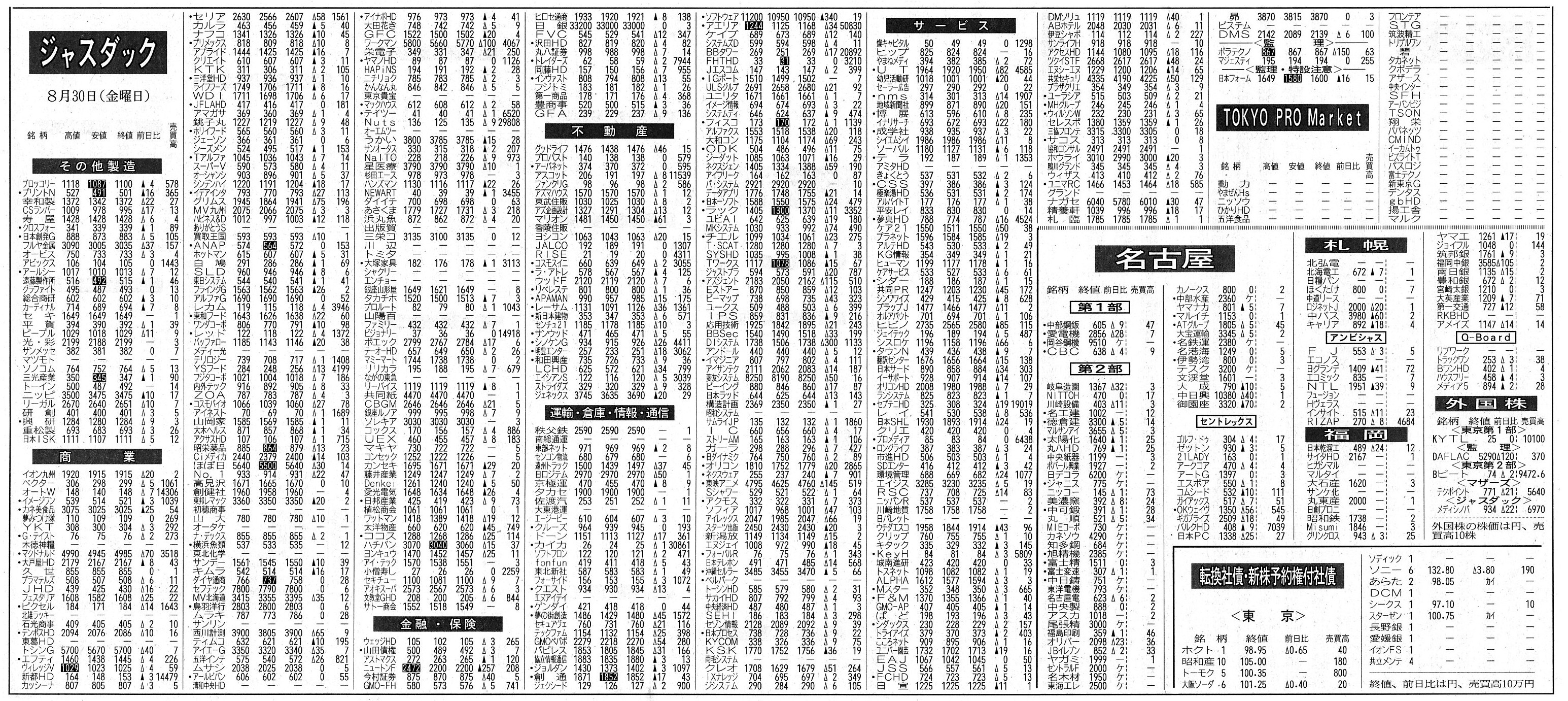

2019年8月30日(金)日本経済新聞

日本株 薄商い 12日連続2兆円割れ 米中・金融施策・・・見極め

(記事)

2019年8月30日(金)日本経済新聞

株式情報

8月29日(木曜日)

(記事)

2019年8月31日(土)日本経済新聞

株式情報

8月30日(金曜日)

(記事)

2019年8月31日(土)日本経済新聞

ソニーと資本提携解消 オリンパスにもファンドの影 財務回復、株主の目意識

(記事)

2019年8月29日

ソニー株式会社

オリンパス株式会社が実施する自己株式の買付けへの応募に関するお知らせ

ttps://www.sony.co.jp/SonyInfo/IR/news/20190829_J.pdf

(ウェブサイト上と同じPDFファイル)

2019年8月30日

ソニー株式会社

オリンパス株式会社による自己株式の買付けへの応募結果に関するお知らせ

ttps://www.sony.co.jp/SonyInfo/IR/news/20190830_J.pdf

(ウェブサイト上と同じPDFファイル)

2019年8月29日

オリンパス株式会社

自己株式取得及び自己株式立会外買付取引(ToSTNeT-3)による自己株式の買付けの決定に関するお知らせ

ttps://www.olympus.co.jp/ir/data/announcement/2019/contents/ir00020.pdf

(ウェブサイト上と同じPDFファイル)

2019年8月30日

オリンパス株式会社

自己株式立会外買付取引(ToSTNeT-3)による自己株式の取得結果

及び自己株式取得終了に関するお知らせ

ttps://www.olympus.co.jp/ir/data/announcement/2019/contents/ir00021.pdf

(ウェブサイト上と同じPDFファイル)

「ゼミナール 金融商品取引法」 大崎貞和 宍戸善一 著 (日本経済新聞出版社)

第13章 証券市場のインフラストラクチャー

1. 金融商品取引所

(3)

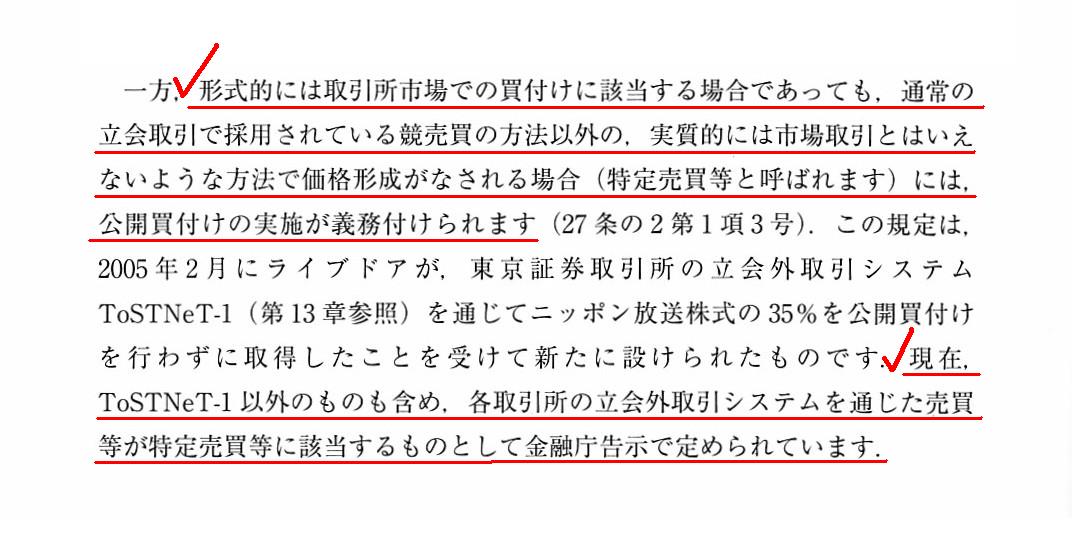

金融商品取引所市場における取引と取引所外取引

立会外取引

「340〜341ページ」

第7章 公開買付け(TOB)をめぐる規制

1.

株式公開買付規制

(2) 公開買付けの実施が強制される範囲

3分の1ルール

「194ページ」

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計256日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜)

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

It is true that this transaction between Sony and Olympus is virtually a

negociation transaction,

but no investors in the market complain about this

transaction between the two.

For this transaction between the two has not

damaged interests of investors in the market at all.

On the other hand, if

this transaction between the two had been made under the traditional securities

system

before October, 1999, it would definitely have damaged interests of

investors in the market.

For this transaction between the two would have

deprived investors in the market

of an opportunity to sell their

shares.

Between the traditional securities system before October, 1999 and

the current securities system,

the concept itself "interests of investors in

the market" is different from each other.

As a means of an "investor

protection,"

the traditional securities system before October, 1999 relied on

purely an "opportunity to sell a share in the market,"

whereas the current

securities system relies on a "disclosure" in the first place and "personal

connections" on occasion.

In short, the traditional securities system before

October, 1999 didn't admit "personal connections" and the like.

On the other

hand, the current securities system admits "personal connections" and the

like

to be one of the "investment abilities" of investors.

確かにソニーとオリンパスの間で行われたこの取引は実質的に相対取引ですが、

2社の間で行われたこの取引について不平を言う市場の投資家は1人もいません。

というのは、2社の間で行われたこの取引は市場の投資家の利益を一切害していないからです。

一方、仮に2社の間で行われたこの取引が1999年10月以前の伝統的な証券制度下において行われたとするならば、

この取引は明らかに市場の投資家の利益を害したことになります。

というのは、2社の間で行われたこの取引は投資家から所有株式を売却する機会を奪ったことになるからです。

1999年10月以前の伝統的な証券制度と現行の証券制度との間では、

「市場の投資家の利益」という概念そのものが互いに異なっているのです。

「投資家保護」の手段としては、

1999年10月以前の伝統的な証券制度は純粋に「市場で株式を売却する機会」に依拠していたのですが、

現行の証券制度は第一に「ディスクロージャー」に依拠していますし時に「人脈」に依拠しているのです。

要するに、1999年10月以前の伝統的な証券制度は「人脈」とその他の同種類のものを認めていなかったのです。

一方、現行の証券制度は、「人脈」その他を投資家の「投資能力」の1つだと認めているのです。

What you call the "principle of a market concentration" in those days was

caused by

the fact that the securities system relied on the opportunity

above.

Investors in the market used to presuppose that they didn't know each

other,

whereas they now presuppose that they can sometimes so.

当時のいわゆる「市場集中原則」は証券制度が上記の売却機会に依拠してからなのです。

市場の投資家はかつては相手方のことを知らないということを前提としていたのですが、

今では相手方のことを知っているということもあるということを前提としているのです。

On the traditional securities system before October, 1999, investors in the

market should have been provided with

an opportunity to sell their shares as

much as possible (and they actually used to).

On the other hand, on the

current securities system, investors in the market don't have to be provided

with

an opportunity to sell their shares at all in theory.

In other words,

on the former securities system, from a standpoint of investors in the

market,

the fact that they were able to "exchange" their shares for cash used

to be by far the most important factor

when they made a securities

investment.

That is to say, from a standpoint of them, an opportunity for

their shares to "expire" didn't used to matter at all.

On the other hand, on

the latter securities system, from a standpoint of investors in the

market,

the fact that their shares are scheduled to "expire" in due course of

time is more important a factor than

the fact that they are able to

"exchange" their shares for cash when they make a securities investment.

That

is to say, from a standpoint of them, even the fact that

shares in general

are not traded in the market frequently doesn't matter at all

1999年10月以前の伝統的な証券制度では、市場の投資家には所有株式を売却する機会が最大限与えられるべきだった

のです(そして、実際に市場の投資家にはその機会が与えられていました)。

一方、現行の証券制度では、市場の投資家に所有株式を売却する機会を与える必要は理論上は全くないのです。

他の言い方をすれば、前者の証券制度では、市場の投資家の立場からすれば、

所有株式を「売却する」ことができるということが証券投資を行う際に圧倒的に重要な要素であったのです。

すなわち、市場の投資家の立場からすれば、所有株式が「満了する」機会は全く重要ではなかったのです。

一方、後者の証券制度では、市場の投資家の立場からすれば、証券投資を行う際には、

所有株式が当然そうするべき時に「満了する」予定となっているということが

所有株式を「売却する」ことができるということよりも重要な要素なのです。

すなわち、市場の投資家の立場からすれば、株式全般が市場で頻繁には取引されていないとしても全く問題ではないのです。

,0LegalDisclosureDocumentHasBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.jpg){kind=link}

{kind=link}