2019年8月19日(月)

「本日2019年8月19日(月)にEDINETに提出された全ての法定開示書類」

注:

本日2019年8月19日(月)にEDINETに提出された全ての法定開示書類は、202冊でした。

2019年8月20日(火)の0時20分頃にEDINETの画面をキャプチャーしたのですが、0時で日付が変わるようでして、

提出期間を「当日」にして検索すると、0件になってしまいました。

提出期間を「過去3日」にして検索すると、昨日・一昨日と土曜日・日曜日がありましたので、

結果的に本日2019年8月19日(月)1日の提出書類が検索結果として表示されました。

Today (i.e. August 19th, 2019), 202 legal disclosure documents have been submitted to EDINET in total.

本日(すなわち、2019年8月19日)、EDINETに提出された法定開示書類は合計202冊でした。

「ゼミナール 金融商品取引法」 大崎貞和 宍戸善一 著 (日本経済新聞出版社)

第13章 証券市場のインフラストラクチャー

1. 金融商品取引所

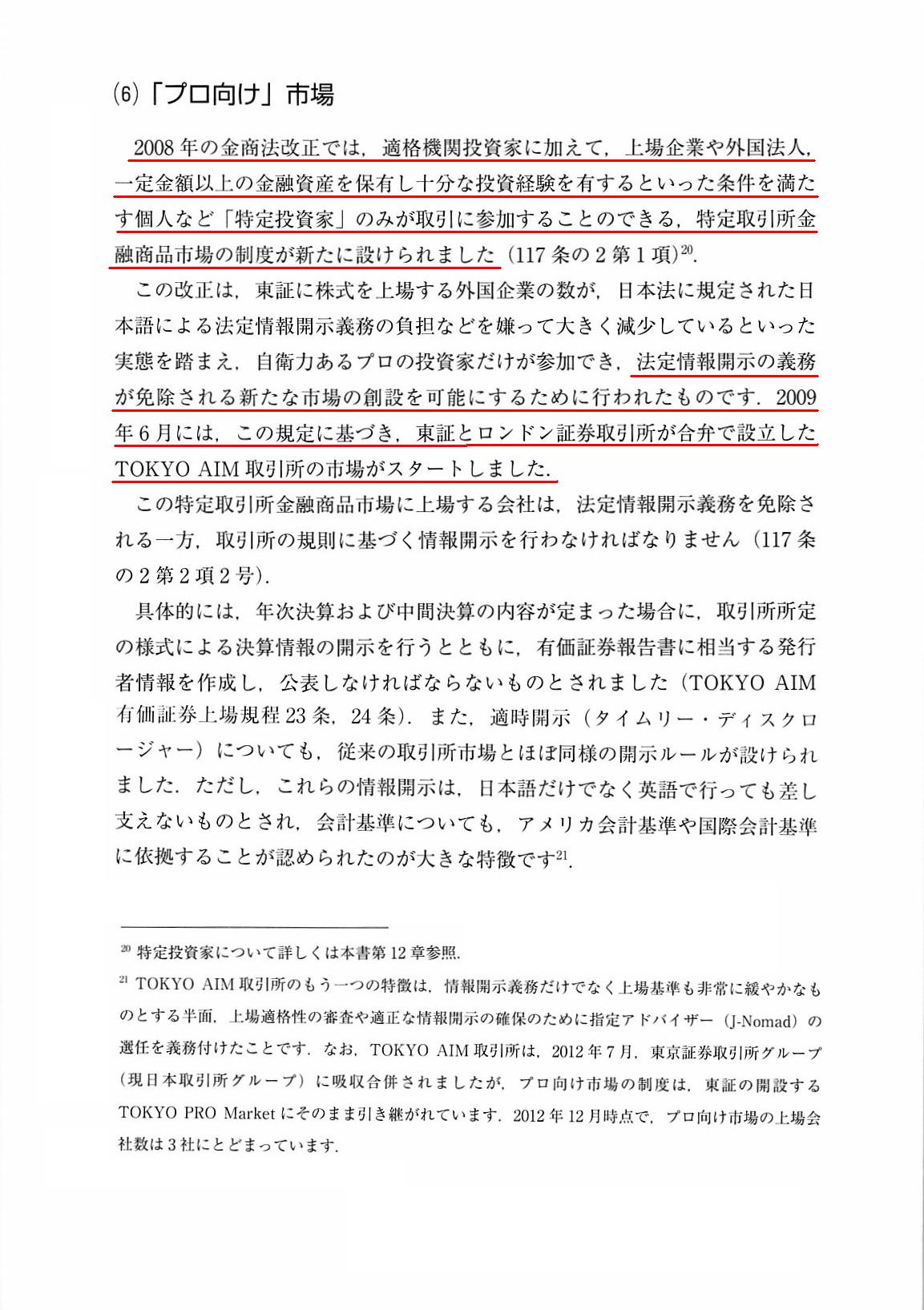

(6) 「プロ向け市場

「347〜348ページ」

注:

また、AIM(Alternative Investment

Market)については、2019年8月12日(月)のコメントでスキャンして紹介した教科書に

【上場基準を設けない取引所市場】というコラム(61ページ)が、さらに、

「プロ向け市場」に関する簡単な脚注(58ページ)が載っていますので参考にして下さい。

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計244日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜2019年4月30日(火))

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

各コメントの要約付きの過去のリンク その2(2019年5月1日(水)〜)

http://citizen2.nobody.jp/html/201905/PastLinksWithASummaryOfEachComment2.html

The traditional securities system before October, 1999 used to be purely for

amateurs, actually.

For they didn't have to make even an investment

judgement.

To be frank, they didn't have to read any legal disclosure

documents at all

because a share price in the market used to be always

invariable.

The traditional securities system before October, 1999 used to

presuppose

that "an intrinsic value of a share is invariable."

In theory,

the traditional securities system before October, 1999 didn't used to require

legal discolusure documents.

The current securities system attempts to

protect interests of investors purely by means of a

"disclosure,"

whereas the traditional securities system before October, 1999

used to attempt to

protect interests of investors by means of something other

than a "disclosure."

The current Securities and Exchange Act after October,

1999 is purely a "law of a disclosure,"

whereas the former Securities and

Exchange Act before October, 1999 used to be a law of a securities

exchange,

not a "law of a disclosure."

Extremely speaking, on the

traditional securities system before October, 1999,

interests of investors

used to be protected from the beginning in a sense.

Extremely speaking, on

the traditional securities system before October, 1999,

all that investors in

the market in those days must do used to be trade a share (i.e. just place an

order).

Here, I would like to compare a share investment on the traditional

securities system before October, 1999

to a "package tour" (a share price in

the market had already been pre-set and every listed share used to be virtually

risk-free.).

If you participate in a "package tour" in U.S., you don't have

to speak English and you can experience a safe tour.

Leaving the question "Is

it good or bad?" out of today's discussion,

the traditional securities system

before October, 1999 didn't used to have

the concept "to protect interests of

investors by means of a 'disclosure'" in it from the beginning.

1999年10月以前の伝統的な証券制度は、実は純粋に素人向けだったのです。

彼らは投資判断すら行う必要はなかったのですから。

率直に言って、彼らは法定開示書類を読む必要は一切なかったのです。

なぜならば、市場の株価は常に一定不変であったからです。

「株式の本源的価値は一定不変である。」ということを1999年10月以前の伝統的な証券制度は前提としていたのです。

理論的には、1999年10月以前の伝統的な証券制度は法定開示書類を求めないものであったのです。

現行の証券制度は純粋に「ディスクロージャー」によって投資家の利益を保護しようとしているのですが、

1999年10月以前の伝統的な証券制度は「ディスクロージャー」以外の何かによって投資家の利益を保護しようとしていたのです。

1999年10月以降の現行の証券取引法は、純粋に「ディスクロージャーの法」なのですが、

1999年10月以前のかつての証券取引法は、「ディスクロージャーの法」ではなく、証券取引の法であったのです。

極端に言えば、1999年10月以前の伝統的な証券制度では、投資家の利益はある意味始めから保護されていたのです。

極端に言えば、1999年10月以前の伝統的な証券制度では、当時の市場の投資家がしなければならなかったことは、

株式の取引を行うことだけ(すなわち、ただ注文を出すことだけ)だったのです。

ここで私は、1999年10月以前の伝統的な証券制度における株式投資を「パックツアー」

(市場の株価は既に予め設定されていましたし全ての上場株式は実質的に無リスクでした)にたとえたいと思います。

米国で「パックツアー」に参加すれば、英語を話せる必要はありませんし安全な旅行を経験できます。

今日の議論ではいい悪いは別にしますが、1999年10月以前の伝統的な証券制度には、

「『ディスクロージャー』によって投資家の利益を保護する」という概念は始めからなかったのです。

,202LegalDisclosureDocumentsHaveBeenSubmittedToEDINETInTotal.JPG){kind=link}

{kind=link}